@z9141706349251 I’m not going to reveal all of my research here, but I’m guess this guys knows more than me or Eisman on this particular topic. $FICO

English

J.T.

674 posts

@Hold_Quality

Actuary | Commodity Investor | High Quality Compounder Holder | Long: SPGI, GOOGL, ASML, FICO, AMZN, META, MA, MCO, TSM, Uranium, FMCC

$FICO CEO: "The regulators are not gonna be comfortable with AI making underwriting decisions when they're not explainable, when it's a black box, when they can't demonstrate that discrimination is not occurring.I mean AI is great in a lot of things. But using it in underwriting, the biggest play is that it's going to get around the rules and regulations of the fair lending laws"

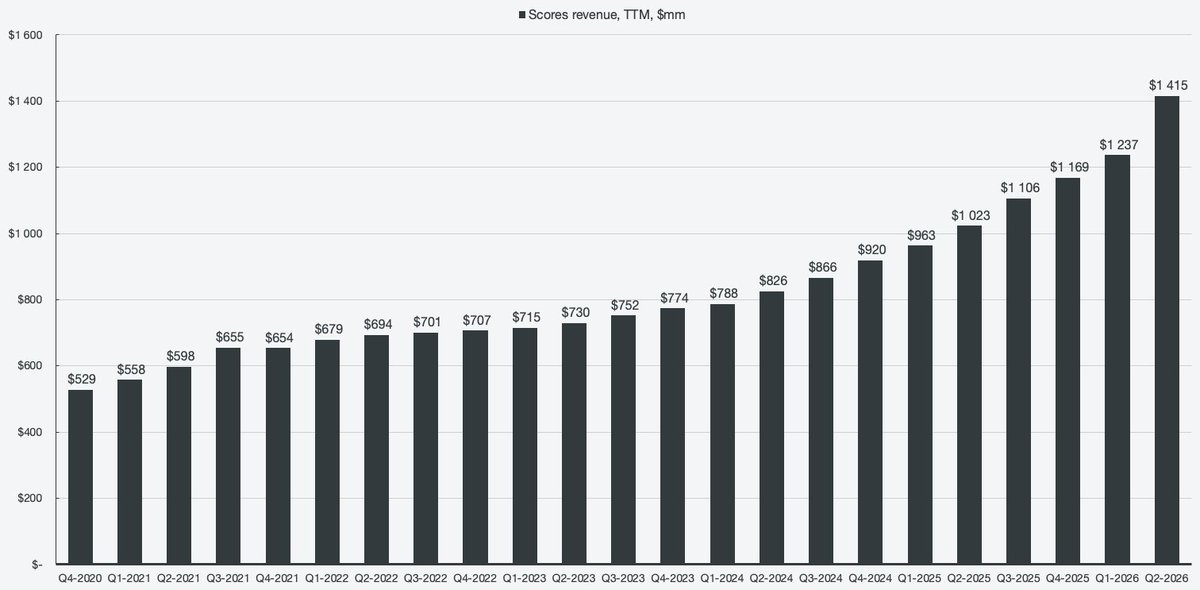

$FICO PUT UP ITS FASTEST GROWING REVENUE QUARTER... EVER?