Shadowban🫸🏻🫷🏼

10.5K posts

Shadowban🫸🏻🫷🏼

@ICinese

il profilo piu bello senza seguaci

Katılım Haziran 2014

1.1K Takip Edilen1K Takipçiler

Die USA haben diesen Krieg absichtlich angefangen. Sie wussten genau, dass der Iran als Reaktion die Straße von Hormus sperren würde. Und genau das wollte die US-Regierung auch!

-Öl soll weltweit knapp werden.

-Lieferketten und Fabriken sollen gestoppt werden.

-Die Preise sollen extrem steigen (Inflation).

-Die Weltwirtschaft soll abstürzen.

Wenn die Wirtschaft abstürzt, müssen die Banken wieder massenhaft neues Geld drucken und die Zinsen senken. Das führt am Ende zu einer riesigen Inflation, bei der das Geld extrem schnell an Wert verliert.

Durch eine hohe Inflation verlieren auch Schulden ihren Wert. Sie schrumpfen quasi von selbst. Und wer hat weltweit die meisten Schulden? Die USA!

Sie stehen mit 39,5 Billionen Dollar in der Kreide. Diesen riesigen Schuldenberg wollen sie so loswerden. Gleichzeitig ist das Chaos die perfekte Ausrede, um ein neues, digitales Zwangsgeld (CBDCs) einzuführen, das der Staat komplett kontrollieren kann.

Auch Deutschland spielt in diesem Plan eine Rolle. Zuerst wurde die Nordstream Pipeline gesprengt, um uns vom billigen russischen Gas abzuschneiden. Jetzt sorgt der Krieg für noch mehr Energieknappheit. Das treibt die Preise für Öl und Gas weiter nach oben.

Und wer verdient daran? Die USA.

Sie haben in den letzten Jahren in Deutschland die neuen Gas-Terminals (in Wilhelmshaven, Lubmin und Brunsbüttel) gebaut. Diese werden jetzt mit amerikanischen Schiffen beliefert.

Die USA schlagen also zwei Fliegen mit einer Klappe: Sie entwerten ihre eigenen Schulden durch Inflation und verdienen sich gleichzeitig dumm und dusselig als neuer Hauptlieferant für teures Öl und Gas.

Wenn du dein Geld in Zeiten von hoher Inflation und geopolitischer Unsicherheit schützen willst, ist die wichtigste Grundregel: Weg von reinen Geldwerten, hin zu echten Sachwerten.

ETFs, Gold, Silber

Deutsch

🇮🇹 Andrea #Pirlo prende quota per la panchina della Nazionale.

Secondo La Gazzetta dello Sport, il nome dell'ex centrocampista campione del mondo 2006 sta guadagnando sempre più consensi come possibile nuovo commissario tecnico dell'Italia. Sarebbe una scelta fortemente sostenuta dal nuovo direttore tecnico Paolo Maldini e dal suo vice Leonardo, che vedono in Pirlo il profilo ideale per aprire un nuovo ciclo in vista del Mondiale 2030.

Pirlo, oggi 47enne, è attualmente impegnato come allenatore negli Emirati Arabi Uniti dopo le esperienze sulle panchine di Juventus, Fatih Karagümrük e Sampdoria. La sua candidatura viene considerata sempre più concreta, mentre l'operazione Guardiola resta molto complessa.

👀 Sareste favorevoli a vedere Andrea Pirlo come nuovo CT della Nazionale italiana? 🇮🇹⬇️

Italiano

@realroseceline Could a new company build the same if it was given 300bln to start from scratch?

English

One of the most underappreciated parts of $NFLX isn’t the content library or even its incredible scale. It’s the balance sheet. I don’t think investors fully appreciate how extraordinary it really is.

Think about what management actually accomplished. If I asked you to build $NFLX from scratch with hundreds of millions of subscribers, global distribution, and one of the largest content libraries ever assembled you’d probably assume the company would need $50–100 billion of debt.

Instead, $NFLX has reached the point where its cash nearly offsets its debt. That’s almost unheard of for a business that spent decades investing billions into content while expanding across the globe. It transformed one of the most capital intensive growth stories into an extraordinary free cash flow machine.

The remarkable part is how they got there. For more than a decade, the market gave $NFLX something almost no company ever receives: time. Investors were willing to sacrifice short term earnings because management consistently proved it could create far more long term value.

The market didn’t finance $NFLX with debt alone. It financed it with trust. Every time management delivered, investors became even more willing to look beyond the next quarter, allowing them to keep investing aggressively.

Most CEOs spend their careers trying to satisfy Wall Street every 90 days. $NFLX was given the rare opportunity to optimize for the next decade instead. That may have been one of its greatest competitive advantages.

The flywheel became almost impossible to stop. More subscribers funded more content and greater scale improved economics. Eventually, the business became so strong that it no longer needed debt to fuel its own growth.

Most people think debt and dilution built $NFLX content library. I think that’s only part of the story. Investor trust was the real asset, and debt and dilution was simply the bridge that allowed management to turn that trust into one of the greatest media businesses ever created.

There’s an important investing lesson here. The greatest businesses aren’t built by maximizing quarterly profits. They’re built by maximizing decades of intelligent capital allocation and earning the trust to execute that vision.

Very few management teams are ever given that opportunity and even fewer earn it. $NFLX didn’t just build one of the world’s greatest businesses, it proved that when exceptional management earns exceptional patience from shareholders, extraordinary outcomes become possible. 🌹

Dimitry Nakhla | Babylon Capital®@DimitryNakhla

A quality valuation analysis on $NFLX 🧘🏽♂️ •NTM P/E Ratio: 22.04x •4-Year Mean: 32.09x •NTM FCF Yield: 3.77% •4-Year Mean: 2.51% As you can see, $NFLX appears to be trading below fair value Going forward, investors can receive ~45% MORE in EPS & ~50% MORE FCF per share 🧠*** Before we get into valuation, let’s take a look at why $NFLX is a great business BALANCE SHEET✅ •Cash & Short-Term Inv: $12.29B •Long-Term Debt: $13.36B $NFLX has a strong balance sheet, an A S&P Credit Rating, & 15x FFO Interest Coverage RETURN ON CAPITAL✅ •2022: 11% •2023: 13% •2024: 19% •2025: 23% •LTM: 26% $NFLX maintains strong and improving returns on capital, highlighting the financial efficiency of the business REVENUES✅ •2022: $31.61B •2026E: $51.38B •CAGR: 12.91% FREE CASH FLOW✅ •2022: $1.62B •2026E: $13.17B •CAGR: 68.85% NORMALIZED EPS✅ •2022: $0.99 •2026E: $3.58 •CAGR: 37.89% SHARE BUYBACKS✅ •2022 Shares Outstanding: 4.51B •LTM Shares Outstanding: 4.32B By reducing its shares outstanding by 4%, $NFLX increased its EPS by 4% (assuming 0 growth) MARGINS✅ •LTM Gross Margins: 49.03% •LTM Operating Margins: 29.72% •LTM Net Income Margins: 28.52% ***NOW TO VALUATION 🧠 As stated above, investors can expect to receive ~45% MORE in EPS & ~50% MORE FCF per share Using Benjamin Graham’s 2G rule of thumb, $NFLX has to grow earnings at an 11.02% CAGR over the next several years to justify its valuation Today, analysts anticipate 2026 - 2028 EPS growth over the next few years to be greater than the (11.02%) required growth rate: 2026E: $3.58 (41% YoY) *FY Dec 2027E: $3.84 (7% YoY) 2028E: $4.60 (20% YoY) $NFLX has an ok record of meeting analyst estimates ~2 years out, but let’s assume $NFLX ends 2028 with $4.60 in EPS & see its CAGR potential assuming different multiples 27x P/E: $124💵 … ~22.7% CAGR 25x P/E: $115💵 … ~18.9% CAGR 23x P/E: $105💵 … ~15.0% CAGR 22x P/E: $101💵 … ~12.9% CAGR 21x P/E: $97💵 … ~10.8% CAGR $NFLX trades near the low end of its historical valuation range, just as advertising is beginning to scale and APAC/LATAM still represent only ~24% of revenue and remain a huge long-term growth driver At a 22x multiple, the case rests primarily on execution rather than multiple expansion. If advertising and international markets deliver, there’s room for some re-rating from today’s lower levels — allowing for the twin-engines to work (EPS growth + multiple expansion) And as FCF margins continue to expand, the company’s economics are becoming increasingly attractive, supporting aggressive share repurchases at current levels Today, at $75💵 $NFLX appears to be a strong consideration for investment ___ 𝐃𝐈𝐒𝐂𝐋𝐎𝐒𝐔𝐑𝐄‼️ 𝐓𝐡𝐢𝐬 𝐜𝐨𝐧𝐭𝐞𝐧𝐭 𝐢𝐬 𝐩𝐫𝐨𝐯𝐢𝐝𝐞𝐝 𝐟𝐨𝐫 𝐢𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐚𝐧𝐝 𝐞𝐝𝐮𝐜𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐩𝐮𝐫𝐩𝐨𝐬𝐞𝐬 𝐨𝐧𝐥𝐲 𝐚𝐧𝐝 𝐝𝐨𝐞𝐬 𝐧𝐨𝐭 𝐜𝐨𝐧𝐬𝐭𝐢𝐭𝐮𝐭𝐞 𝐢𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐚𝐝𝐯𝐢𝐜𝐞, 𝐚𝐧 𝐨𝐟𝐟𝐞𝐫, 𝐨𝐫 𝐚 𝐬𝐨𝐥𝐢𝐜𝐢𝐭𝐚𝐭𝐢𝐨𝐧 𝐭𝐨 𝐛𝐮𝐲 𝐨𝐫 𝐬𝐞𝐥𝐥 𝐚𝐧𝐲 𝐬𝐞𝐜𝐮𝐫𝐢𝐭𝐲. 𝐁𝐚𝐛𝐲𝐥𝐨𝐧 𝐂𝐚𝐩𝐢𝐭𝐚𝐥® 𝐚𝐧𝐝 𝐢𝐭𝐬 𝐫𝐞𝐩𝐫𝐞𝐬𝐞𝐧𝐭𝐚𝐭𝐢𝐯𝐞𝐬 𝐦𝐚𝐲 𝐡𝐨𝐥𝐝 𝐩𝐨𝐬𝐢𝐭𝐢𝐨𝐧𝐬 𝐢𝐧 𝐭𝐡𝐞 𝐬𝐞𝐜𝐮𝐫𝐢𝐭𝐢𝐞𝐬 𝐝𝐢𝐬𝐜𝐮𝐬𝐬𝐞𝐝. 𝐀𝐧𝐲 𝐨𝐩𝐢𝐧𝐢𝐨𝐧𝐬 𝐞𝐱𝐩𝐫𝐞𝐬𝐬𝐞𝐝 𝐚𝐫𝐞 𝐚𝐬 𝐨𝐟 𝐭𝐡𝐞 𝐝𝐚𝐭𝐞 𝐨𝐟 𝐩𝐮𝐛𝐥𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐚𝐧𝐝 𝐬𝐮𝐛𝐣𝐞𝐜𝐭 𝐭𝐨 𝐜𝐡𝐚𝐧𝐠𝐞 𝐰𝐢𝐭𝐡𝐨𝐮𝐭 𝐧𝐨𝐭𝐢𝐜𝐞. 𝐈𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐡𝐚𝐬 𝐛𝐞𝐞𝐧 𝐨𝐛𝐭𝐚𝐢𝐧𝐞𝐝 𝐟𝐫𝐨𝐦 𝐬𝐨𝐮𝐫𝐜𝐞𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞𝐝 𝐭𝐨 𝐛𝐞 𝐫𝐞𝐥𝐢𝐚𝐛𝐥𝐞 𝐛𝐮𝐭 𝐢𝐬 𝐧𝐨𝐭 𝐠𝐮𝐚𝐫𝐚𝐧𝐭𝐞𝐞𝐝 𝐚𝐬 𝐭𝐨 𝐚𝐜𝐜𝐮𝐫𝐚𝐜𝐲 𝐨𝐫 𝐜𝐨𝐦𝐩𝐥𝐞𝐭𝐞𝐧𝐞𝐬𝐬. 𝐏𝐚𝐬𝐭 𝐩𝐞𝐫𝐟𝐨𝐫𝐦𝐚𝐧𝐜𝐞 𝐝𝐨𝐞𝐬 𝐧𝐨𝐭 𝐠𝐮𝐚𝐫𝐚𝐧𝐭𝐞𝐞 𝐟𝐮𝐭𝐮𝐫𝐞 𝐫𝐞𝐬𝐮𝐥𝐭𝐬.

English

@DeepIceValue Imagine giving ur money to a fund just to invest it all in berkshire 🤔

English

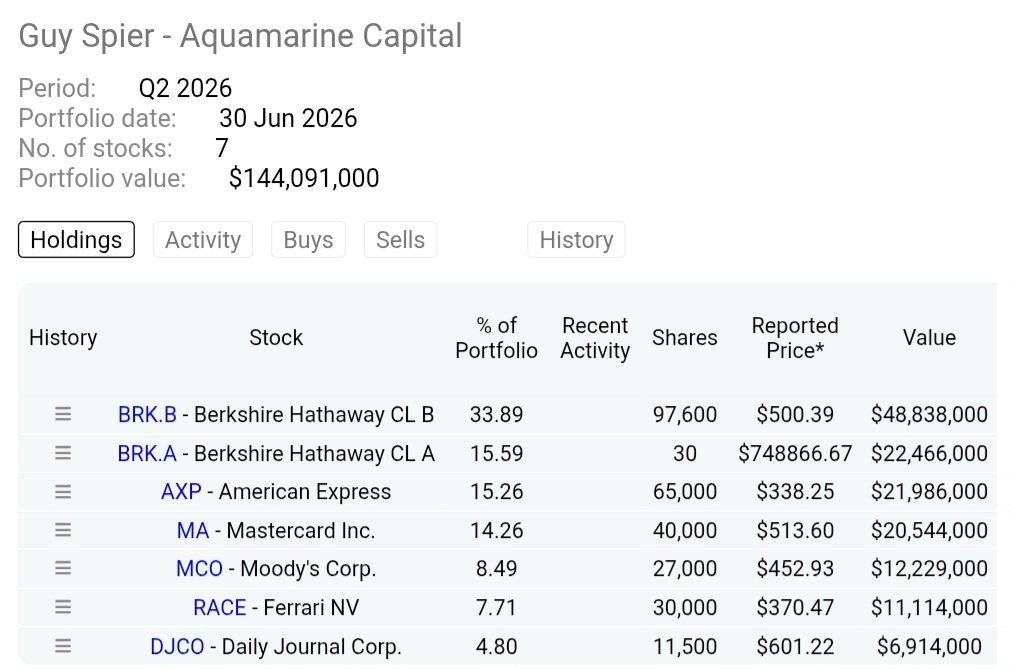

Superinvestor Guy Spier has reported no changes in his portfolio..

Last time we saw him making moves was Q4 2025, and he was closing $BABA, $GOOG, $AXP, $MA..

For people who dont know, Guy has been fighting aggressive form of brain cancer.. 🙏

English

BREAKING:

A potential terror attack against the Jewish community in France has been foiled.

France’s internal intelligence agency DGSI had information about a car potentially intended for use in a violent action against the Jews.

The car was found by the police in Sarcelles, just north of Paris, which has a large Jewish community.

300 people were evacuated from a cinema and several restaurants near the security perimeter around a car.

Bomb disposal experts were called in and carried out a controlled check shortly before midnight.

In the trunk, they found a rifle and a gun.

English

@MirkoBifano Esatto. Paghi e per questo funziona. In italia nn paghi e fa schifo. Poi paghi comunque per andare nel privato

Italiano

La sanità in Svizzera è un salasso!

Ora aspetto quelli che mi dicono che in Italia devi aspettare o andare privatamente, resta il fatto che in Svizzera 🇨🇭 la sanità costa un rene (per l’appunto)

Sicuramente funziona bene, ci sono degli ospedali che sembra di essere in albergo ma li paghi tutti, mentre le casse malati ogni anno aumentano i premi.

Oggi una persona da sola spende circa 300/400 € al mese di cassa malati con una franchigia di 2500 chf.

Si guadagna di più ma si spende di più.

Italiano

C’è un dato incredibile sulla Spagna.

Ha giocato SOLO 2 SEMIFINALI MONDIALI nella sua storia.

Ha aspettato 20 anni per giocare la prima nel 1950.

Poi addirittura 60 anni per giocare la seconda nel 2010.

E adesso può arrivare la terza dopo 16 anni…

Italiano

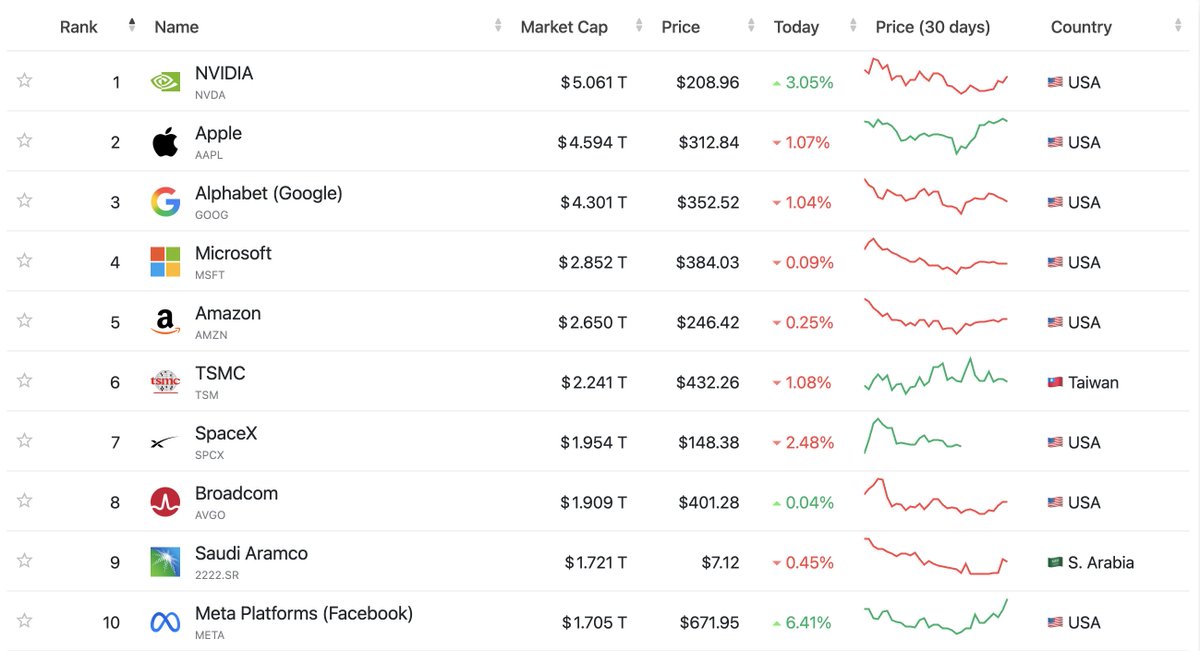

Of the companies currently in the top 10 market cap-

How many do you think will still be here 10 years from now?

English

@dividendology I think in a 90bln colossus there is some fat that can be cut. Elliot inv. will puah for that. Only thx to this uncertainty u get a discount. Otherwise it would be too easy :)

English

$PEP is trading very near a 5 year low, at $137.

This gives them a starting yield of above 4%, which is the highest yield the company has seen in over a decade.

I keep seeing people say that $PEP is a 'no brainer' at these prices, but looking under the hood just a little reveals some real problems: 👇

English

I’ve been saying since approx $30b market cap (more than a decade), that one of $NFLX biggest competitive advantages is its lowest content cost per subscriber.

Drew says monthly content cost per subscriber:

$NFLX: ~$5

$WBD + $PARA: ~$12

$PARA standalone: ~$18

With more than 325 million subscribers, every dollar they spend on content is spread across an enormous customer base. That translates into higher margins, greater pricing power, better returns on investment, and significantly stronger free cash flow.

And remember, $NFLX is already a free cash flow machine. If they eventually reach the 40% OM like Drew suggests, free cash flow will accelerate dramatically (from here), and really go gangbusters. That’s the real power of scale... 🌹

Drew Cohen@DrewCohenMoney

English

Shadowban🫸🏻🫷🏼 retweetledi

@dividendology Zoom out. Over the long run $PEP has soundly beaten $KO. Consider the current situation a buying opportunity.

Log scale adjusted for dividends.

English

Look at the divergence in the P/E multiple for $KO and $PEP.

Two companies that historically have traded hand in hand-

But one is now hitting new all-time highs while the other is approaching a 5 year low.

It isn't hard to know why this is the case...

English

@MirkoBifano Cioe in italia nn si lavora ci stai dicendo? Sara il motivo dei loro salari doppi?

Italiano

Può sembrare un video divertente ma è realmente così la vita in Svizzera 🇨🇭, non si vive giorno per giorno, ma si vive esclusivamente per lavorare.

Poi il fine settimana bisogna comunque tenere un profilo basso, perché i costi sono altissimi e non ci si può dare alla pazza gioia.

Poi attenzione io adoro quel paese, ma è completamente un altra vita rispetto all’Italia.

Italiano

L'allenatore dell'Egitto che a fine partita sputa ai tifosi dell'Argentina e va a fare brutto a un fotografo.

Non importa la posizione che occupano, restano spiritualmente dei maranza

Italiano

@IstLiberale @SalisIlaria Probabilmente non ha capito per cosa stava votando. O magari le chat criptate servono ai suoi amici violenti quando organizzano la prossima manifestassioneh x la pasceh

Italiano

Ci fa piacere che @SalisIlaria si sia opposta al Chat Control, votando meglio di tanti membri di partiti di destra (che di liberale non hanno nulla se sostengono questa deriva autoritaria).

Italiano

Feierabend. Sitz hier am Wasser und hab natürlich keinen Bikini 👙 dabei. Keine Menschenseele weit und breit… wisst ihr was? YOLO. Heute wird nackig angebadet und zwar JETZT. 🌊 Hoffen wir mal, die gelbe Flagge ist gnädig. 👀

Tag war eh premium bis jetzt. #Nacktbaden 🇩🇰

Deutsch

@realroseceline But narrative shifts dont always occur. Lets say i wait 5 year for a stock to catch up to its intrinsic value then it doubles. U would have done same sitting in the sp500 index.

English

Priced for perfection

If you own a wildly popular stock, always ask yourself one question. How much of today’s stock price is supported by the underlying business, and how much is simply excitement, momentum, and unrealistic expectations? Those are two very different things, yet investors constantly confuse them.

Imagine a business is intrinsically worth $100 per share, but excitement pushes the stock to $300. The business didn’t suddenly become three times better overnight. Investors simply became willing to pay three times as much for the exact same business.

Most investors celebrate that. I become more cautious. A higher stock price doesn’t automatically mean you’ve become wealthier. Sometimes it simply means your future returns have quietly been borrowed by today’s valuation.

Eventually, one of two things has to happen. The business can spend years growing into that valuation, or the stock price can fall back toward intrinsic value. There really aren’t many other outcomes.

The first outcome is more common than people realize. One of the greatest businesses ever built, $MSFT, spent years growing into an excessive valuation after the dotcom bubble. The business continued executing brilliantly, yet shareholders earned mediocre returns because they had simply paid too much.

It doesn’t have to be that extreme, either. Some of the world’s greatest businesses, including $SPGI, $MCO, and $MSCI, have produced flat or disappointing shareholder returns over roughly the last five years despite continuing to execute at an extraordinarily high level. Nothing was wrong with the businesses. The problem was that investors had already priced in so much future success that reality simply couldn’t keep up.

The second outcome is much more painful. The stock price falls back toward intrinsic value, and shareholders endure a brutal correction. History is full of examples, including $NFLX, $AMZN, $TSLA, and countless others that experienced enormous drawdowns despite remaining outstanding businesses.

This is one of the most misunderstood ideas in investing. A great business does not automatically become a great investment. There is a price where almost every business becomes a poor investment, just as there is a price where almost every mediocre business becomes interesting.

Most investors ask, “How fast is this company growing?” I almost never start there. Instead, I ask, “What assumptions must become true just to justify today’s price?” Those are completely different questions, yet one leads to speculation while the other leads to investing.

Imagine I offer you two investments. One compounds intrinsic value at 20% per year, while the other compounds at 12%. Almost everyone immediately chooses the first business because faster growth sounds like the obvious answer.

Now imagine I tell you the first business trades at 40 times intrinsic value, while the second trades below intrinsic value. Suddenly the answer isn’t so obvious. The greatest business isn’t always the greatest investment.

One of the cruelest paradoxes in investing is that confidence and future returns often move in opposite directions. When a stock doubles, investors usually become more confident. Ironically, that’s often the exact moment expected future returns begin falling because so much future success has already been priced into the stock.

Think of price and intrinsic value like a rubber band. Sometimes they stay close together, and sometimes excitement stretches them very far apart. Nobody knows exactly when they’ll reconnect, but history suggests they almost always do.

The biggest mistake investors make is believing rising stock prices create value. They don’t. Rising stock prices often borrow returns from the future, and eventually the bill arrives. Sometimes it arrives through years of flat returns, and sometimes it arrives through a painful correction.

1/2👇

English

Name one thing that Belgium does better than the US. I’ll wait.

English