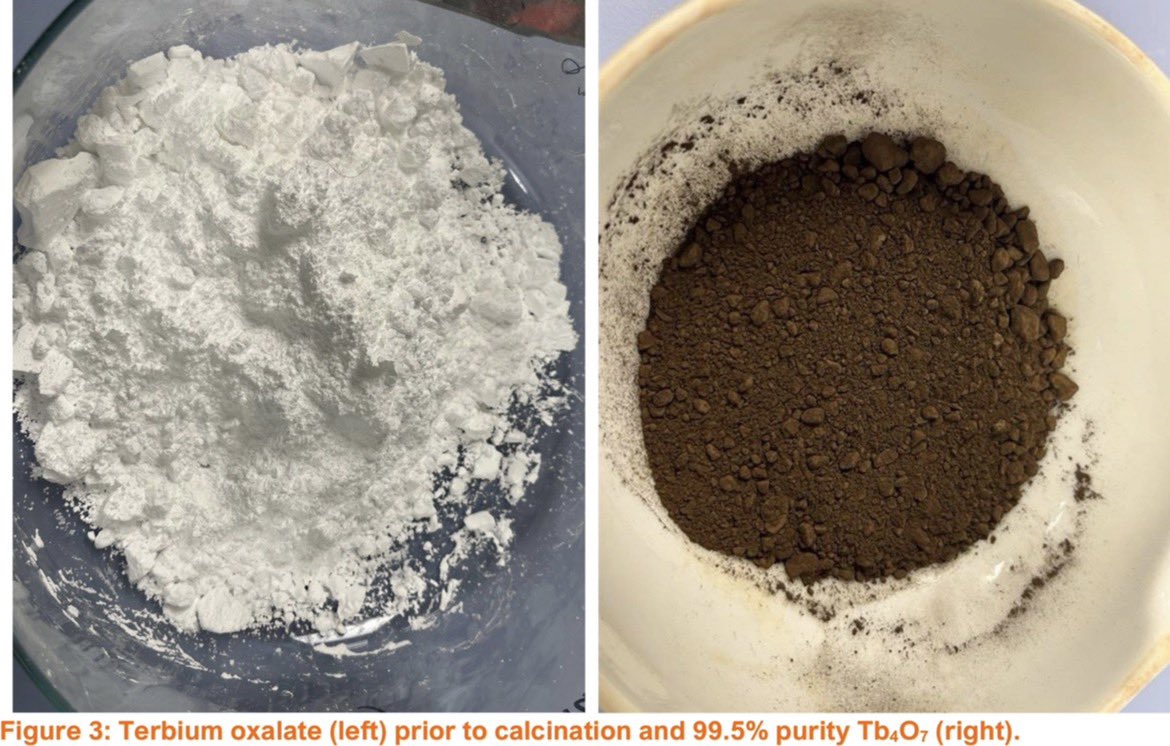

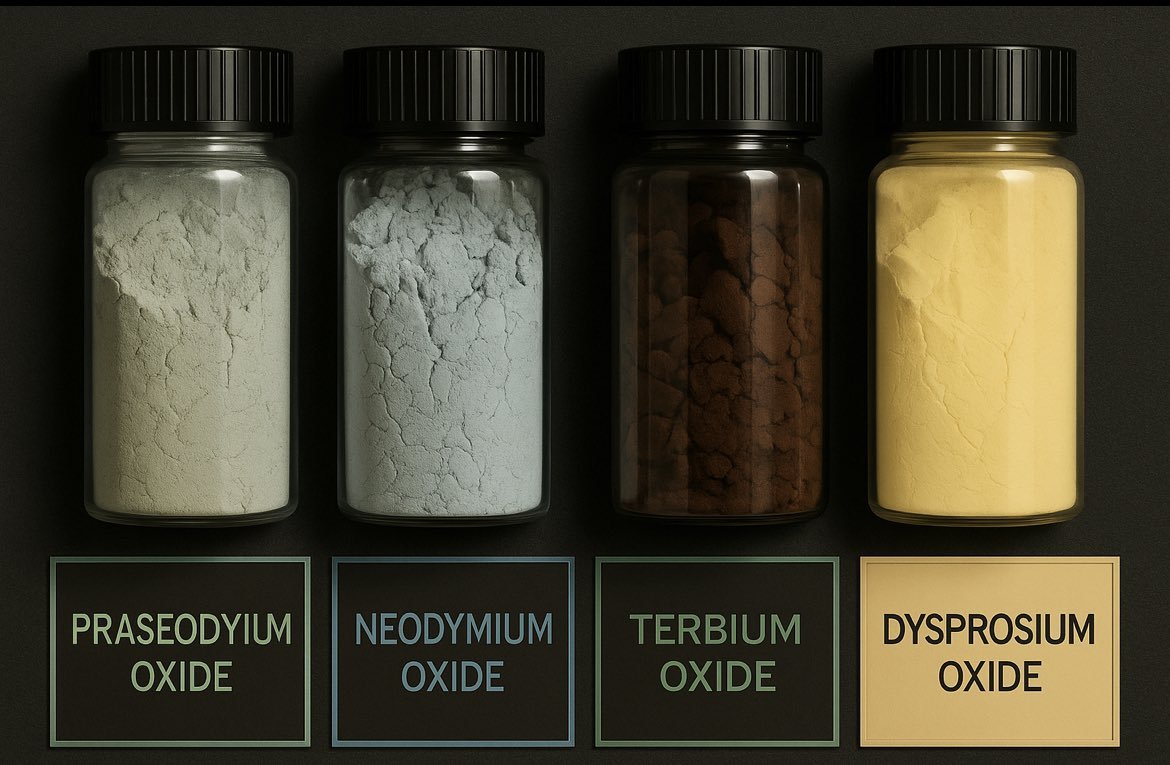

IXR Dy₂O₃ Tb₄O₇ retweetledi

USA Rare Earth, Inc. (Nasdaq: USAR) and InfraVia Capital Partners are each acquiring a minority stake in CARESTER, a leading French specialist in rare earths processing and separation.

With significant support from the French government, this investment creates one of Europe's most complete rare earth industrial ecosystems — integrating processing, metal and alloy production, and magnet manufacturing into a single, resilient value chain. It marks a major milestone in building the secure rare earth ecosystem that advanced technologies and the energy transition demand.

The broader partnership provides the Company and its subsidiary Less Common Metals (“LCM”) Europe the right to purchase some of Carester’s oxide output from its Caremag facility and access for USA Rare Earth to Carester engineering capabilities and related intellectual property for separation, processing, and recycling.

Conversely Carester will have long-term access to heavy rare earth feedstock from the Company’s Round Top deposit in Texas, which is expected to begin commercial operation in late 2028. The closing of the contemplated transaction is subject to customary conditions including confirmatory due diligence as well as the negotiation and execution of definitive documentation.

Founded in 2019, Carester is a French leading specialist in rare earths processing and separation technologies, with a strong focus on innovation and the development of more efficient, more environmentally friendly industrial processes. The company brings together decades of technical expertise, supporting the entire value chain from raw material sourcing through high-purity rare earth oxides, critical for advanced manufacturing sectors including renewable energy, electric mobility, and electronics. Carester is currently building its

The platform will unite the technological expertise, process innovation, and production capacity of USA Rare Earth, LCM, and Carester to accelerate development and strengthen capabilities across the rare earth value chain. In parallel, USA Rare Earth – through LCM Europe – is developing a 3,750 mtpa metal and alloy production facility at the same location. The partnership will create one of Europe’s most complete rare earth industrial ecosystems.

🧲 RARE EARTHS: TWO CONTINENTS, ONE METAL PARTNER

Big move overnight:

USA Rare Earth (USAR) is taking a minority stake in French separator Carester and locking in a 15‑year offtake deal for heavy rare earth oxides from Carester’s Caremag plant in Lacq 🇫🇷

At the same Lacq platform, LCM Europe will build a

3,750 tpa rare earth metal & alloy plant – turning those

oxides into NdPr, Dy and Tb alloys for magnet makers. 🔥

That makes LESS COMMON METALS the common thread:

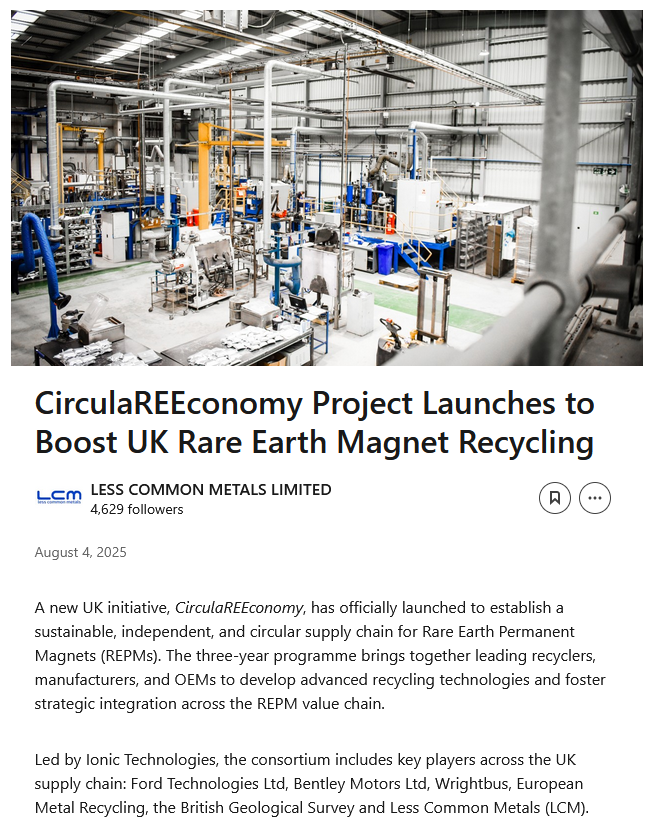

🇬🇧 In the UK

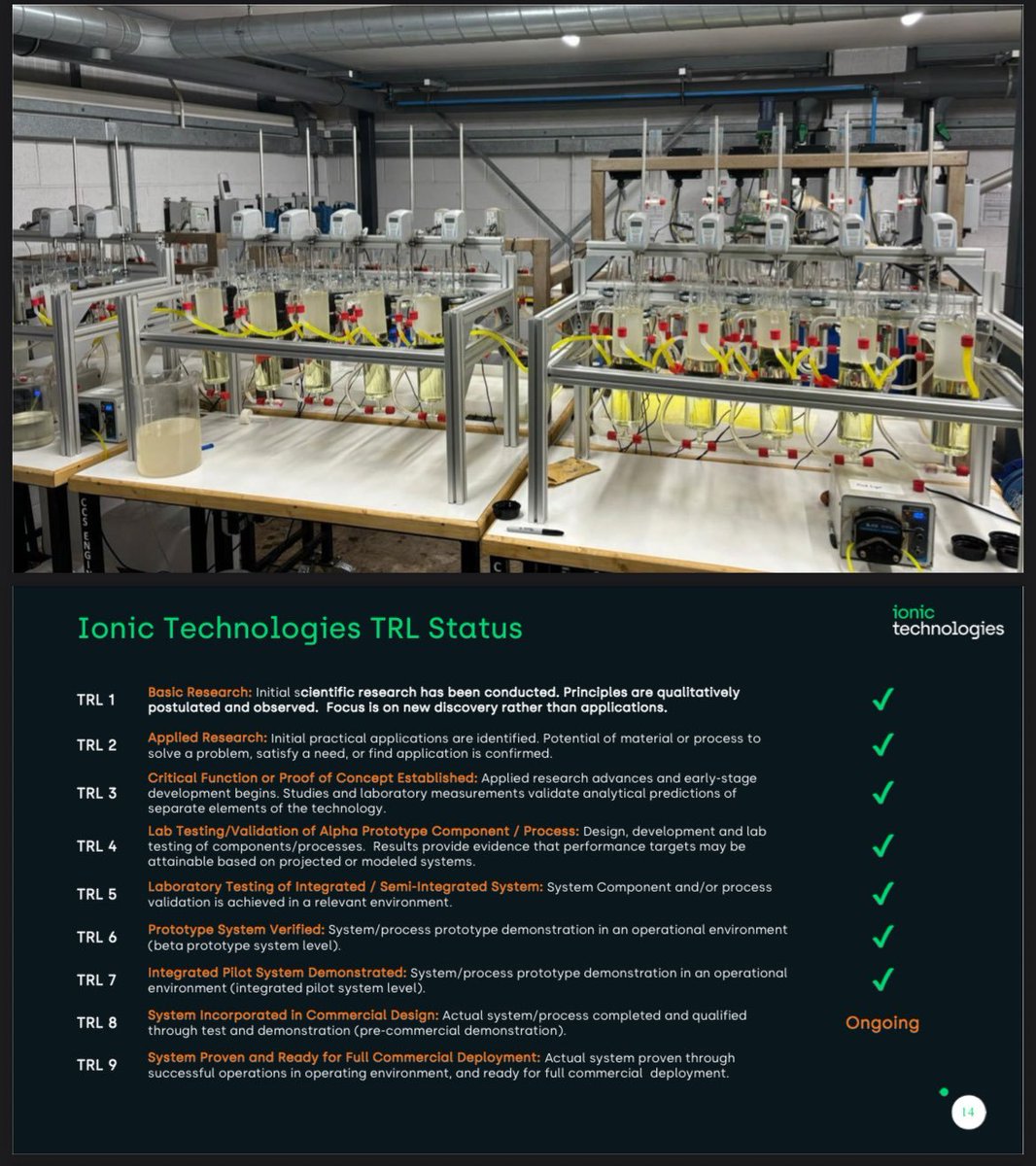

– LCM is metallisation + alloy partner to Ionic Technologies

– Together with Ford, Bentley, Wrightbus, EMR and BGS they are

leading the £11m CirculaREEconomy (CREEM) programme via APC UK

– Previous Innovate UK projects (CLIMATES, REEVALUATE, Drive 35)

have already proven the loop:

scrap magnets → Ionic hydromet process → high‑purity REOs →

LCM metal & strip‑cast alloy → new NdFeB magnets

🇺🇸 / 🇫🇷 Now in US–EU

– USAR’s Round Top deposit supplies heavy REE feed

– Carester provides separation & recycling tech

– LCM Europe converts oxides to metal/alloy in France

Mining gets the headlines, but it’s metallisation and

alloy making that actually turn separated oxides into

a weapon‑ and EV‑ready magnet supply chain.

LCM sits in the middle of all of it. 🧲🌍

#USAR #Carester #LCM #IonicTechnologies

#RareEarths #NdFeB #CriticalMinerals #Metallisation

#MagnetAlloys #CircularEconomy #CLIMATES #REEVALUATE @IXR2THAMOON @IONIC_RE @IONICTECH_UK @LCM_Metals @CMA_Minerals @USARareEarth

#Drive35 #CREEM #EVs #Defense #SupplyChain

English