Sabitlenmiş Tweet

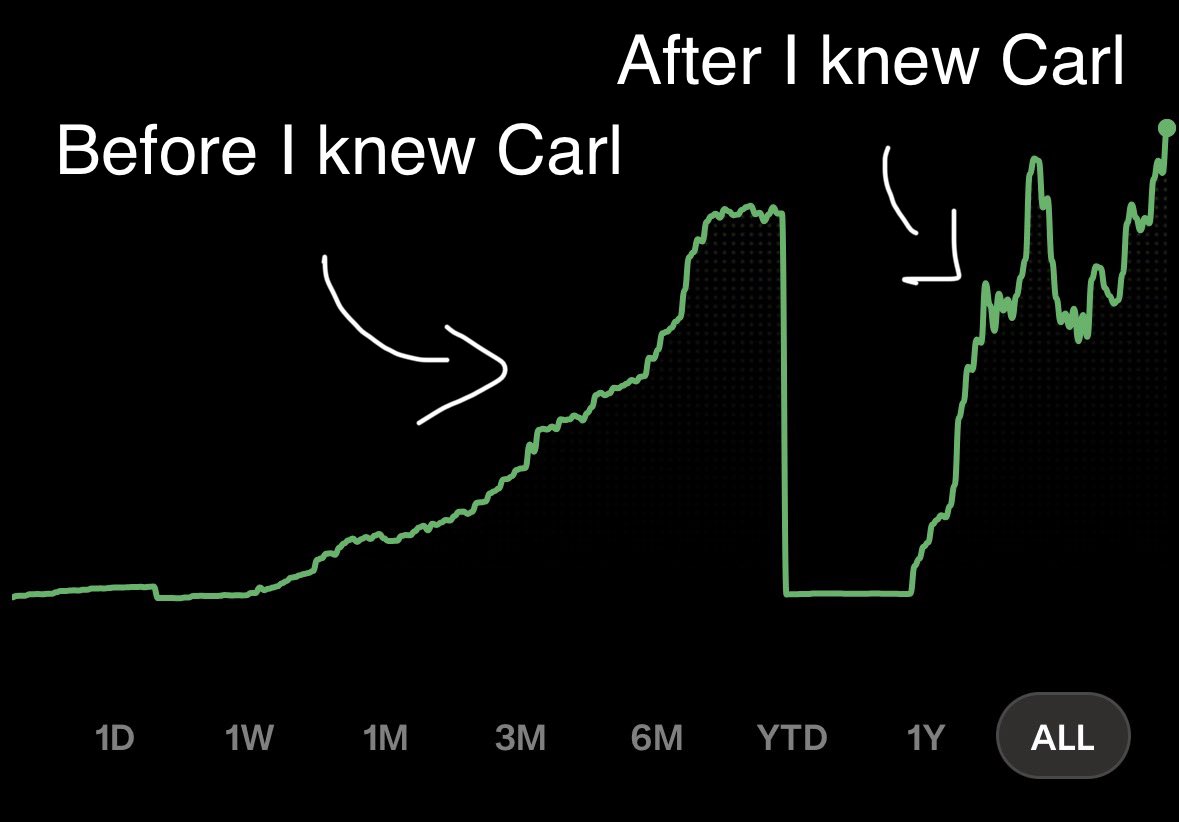

My reaction to my family and freinds when they did not invest in $ABCL

In Chad Hansen we trust

@JackPrescottX @iHooghvorst

GIF

English

The Golf Investor

2.9K posts

@ImmersedGolf

Golf - LOTRs - Investing - Fitness/Health. What did you get done this week?

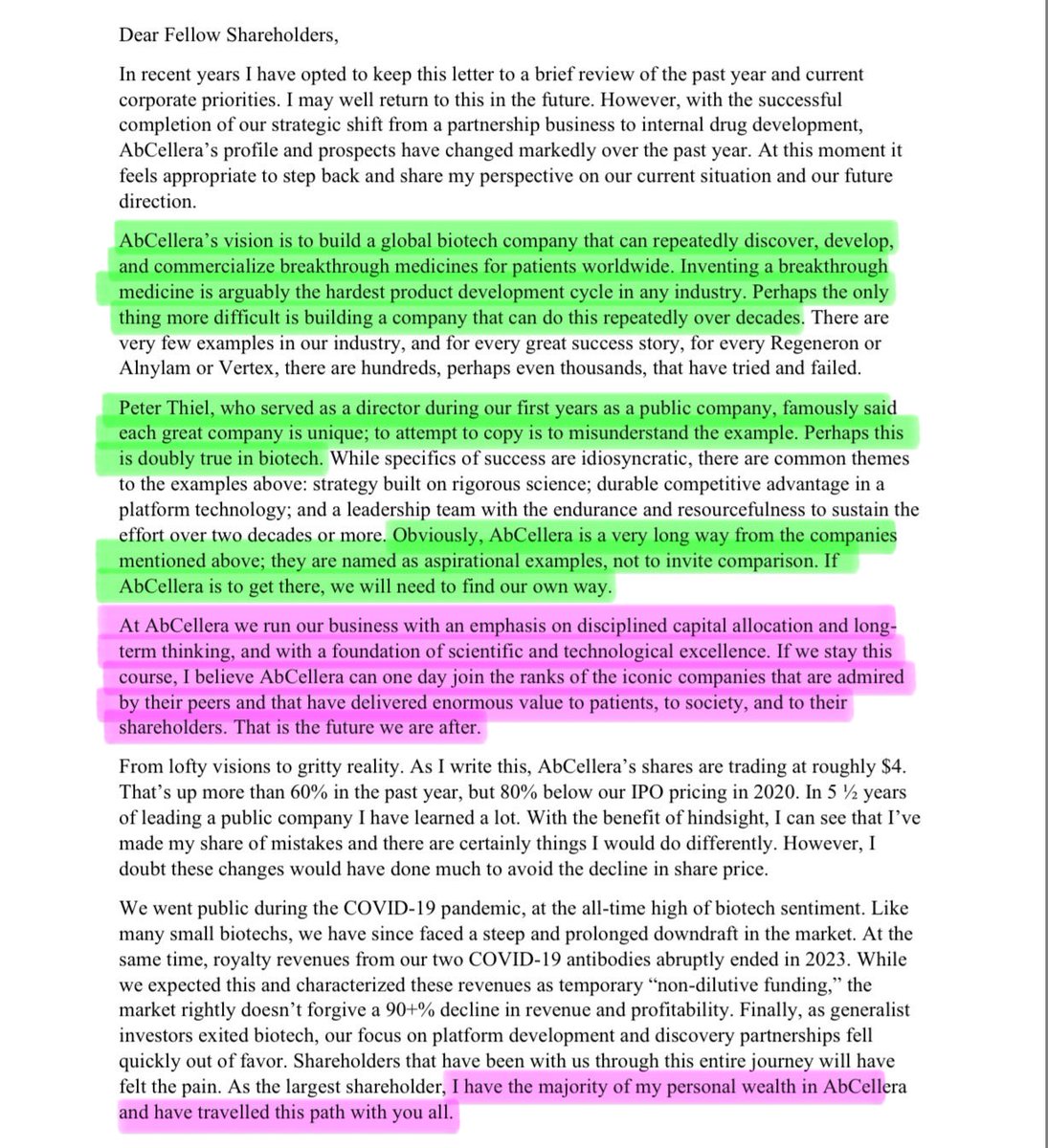

AbCellera CEO Carl Hansen’s holding company is named “Thermopylae Holdings” @grok provides an interesting summary of The Battle of Thermopylae: “The Battle of Thermopylae, fought in 480 BCE, saw a small Greek force led by King Leonidas of Sparta confront a massive Persian army under Xerxes I. At the narrow pass of Thermopylae, around 7,000 Greeks, including 300 Spartans, held off the Persians—estimated at 100,000 to 300,000—for three days. Despite their heroic resistance, a Greek traitor revealed a mountain path, allowing the Persians to outflank the defenders. Leonidas dismissed most of his troops, but he and his 300 Spartans, along with a few others, fought to the death, delaying the Persian advance. This sacrifice bought time for the Greeks to prepare a larger defense, contributing to their eventual victory. The lesson often drawn is that courage, unity, and strategic sacrifice can inspire and enable greater triumphs against overwhelming odds.”

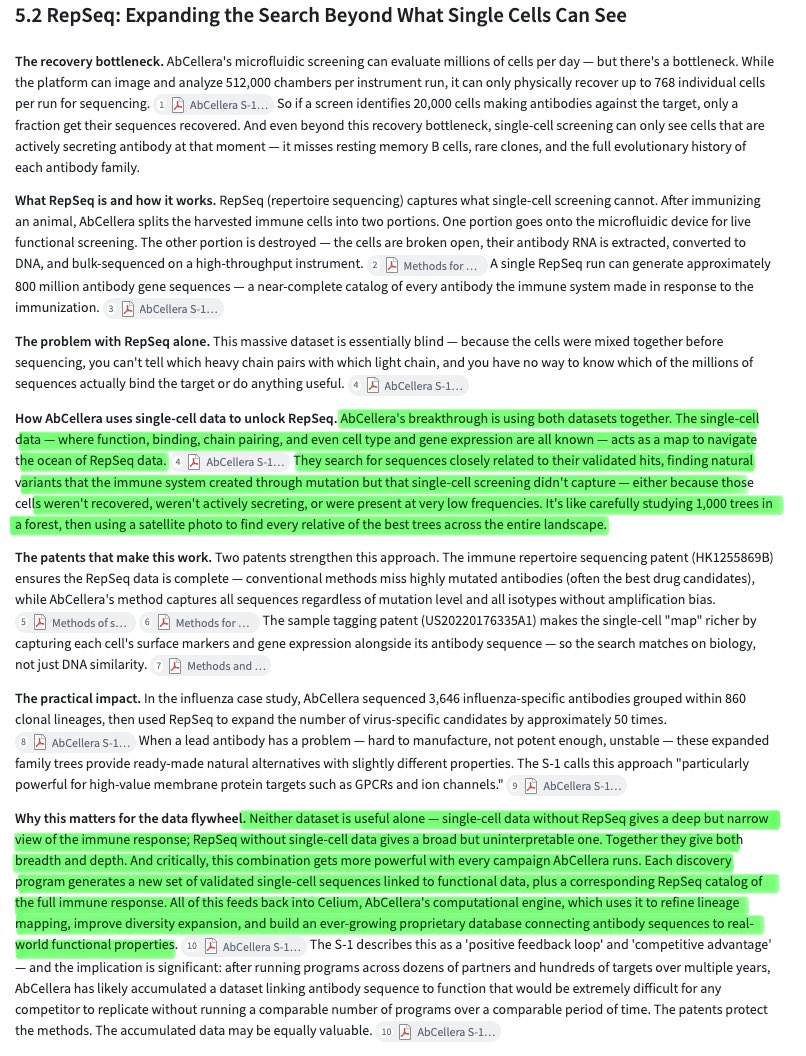

IMO, one of the more interesting parts of AbCellera’s antibody discovery process is the use of their RepSeq technology in combination with single cell data: “A single RepSeq run can generate approximately 800 million antibody gene sequences - a near-complete catalog of every antibody the immune system made in response to the immunization.” “AbCellera's breakthrough is using both datasets together. The single-cell data: where function, binding, chain pairing, and even cell type and gene expression are all known - acts as a map to navigate the ocean of RepSeq data.” “In the influenza case study, AbCellera sequenced 3,646 influenza-specific antibodies grouped within 860 clonal lineages, then used RepSeq to expand the number of virus-specific candidates by approximately 50 times. When a lead antibody has a problem — hard to manufacture, not potent enough, unstable — these expanded family trees provide ready-made natural alternatives with slightly different properties.” From the S-1: “We believe this approach, to use natural antibody variants from the repertoire to help design optimized candidates, is particularly powerful for high-value membrane protein targets such as GPCRs and ion channels (which cannot be optimized by conventional display-based methods). We also believe it can significantly improve the success-rate and reduce the time needed to optimize development leads.” $ABCL