Satyalal Devineni

2K posts

Just finished building my positions in $SNAP and $OSCR.

I’ll be looking to hold both of these for the long term and let the thesis play out.

Now I’m mainly eyeing dip opportunities in $SOFI, $NOW, and $ZETA.

Oh yeah, I also bought more $AMZN today.

English

@ant_trading1 Options are too emotional especially short term ones,,

English

@devineni6 I use QualTrim, I can run it for you

Just tell me what numbers you want to plug in, I can use a PE or FCF

English

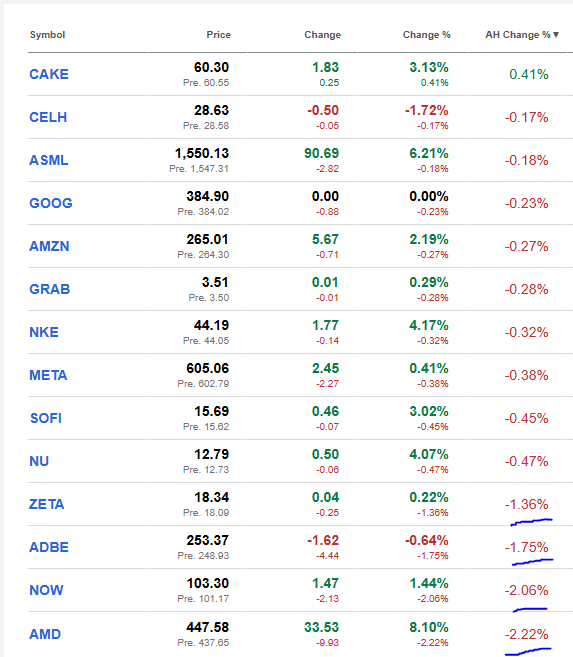

Is today going to break the trend?!?

$AMD and $NOW both red on the same day? Do you guys think both Semis and SAAS will be red today?

This should be bullish long term, I want to own both, so I want to see this trend break. I want to see $NOW and $AMD both going up 3+% on the same day

That's when the Carson Fund will truly start rolling

English

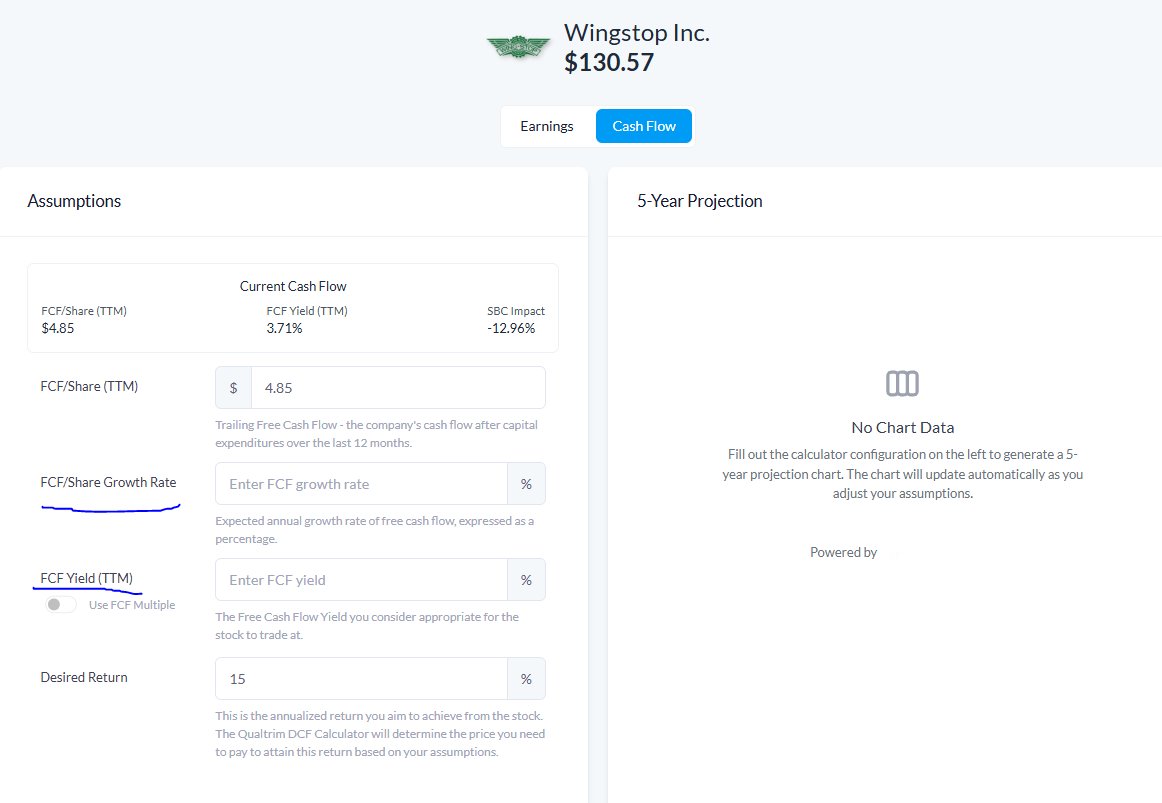

@value_invest01 @cashflow_king94 Want to know your thoughts on $WING?

English

The pain of opportunity cost, and it’s a very human reaction bro but let me tell you this

What happened to you was that relative underperformance was too painful, so you redeployed the capital.

This is classic performance chasing dressed up as discipline. You’re chasing a feeling. $MA is still a wonderful business.

The business didn’t break. The price simply lagged while the market rotated hard into AI/semiconductors. That rotation created the exact discount we like. This is where you buy not sell $MA

English

Fully exited $MA today.

Sad to see it go honestly... Mastercard is still a world-class business.

60% operating margins.

175 billion transactions a year.

A toll booth on the global economy.

But look at this chart.

$MA over the last year: -14%.

S&P 500 over the last year: +25%.

That's a 39% gap on a stock I was holding while the rest of my portfolio was ripping... I don't care how good a business is. If it's underperforming the index by nearly 40% over a year, that capital needs to be somewhere else.

Opportunity cost is real on this one - every pound sitting in $MA was a pound not compounding in $NVDA , $AVGO or $CAT

This is probably the hardest lesson in investing.

Letting go of a stock you love because the numbers aren't working - Your feelings don't make you money. The data does.

Never sell unless the thesis breaks? Sometimes the thesis is fine and the stock just isn't performing at all, even on a longer timeframe - That's enough.

Good company, wrong timing so my capital is redeployed elsewhere.

What's a stock you've held onto for too long?

English

@realroseceline Thanks Rose..Growth is the only thing concerning at this moment it shows 12% yoy .. but From 3000stores to 7000stores in 6 years and if we get same estimated revenue then it would be around 22% yearly.. let’s see 👍execution is matter.. now I know what’s your new pick🤑

English

Historically some of the best businesses in the world have been royalty models. Businesses like $MSCI, $SPGI, $V, $MA, franchisors, app stores, exchanges, and licensing businesses all share one common characteristic. They collect a percentage of activity while somebody else takes on the operating burden and investment. In many ways, the ultimate business model is simply owning a small piece of a giant ecosystem while other people do most of the work.

That is what makes $WING interesting to me. Franchisees are the ones putting up the capital to build restaurants, hire labor, and deal with day to day operations. Meanwhile $WING collects roughly 5.5% of system sales while maintaining an incredibly asset light structure. The economics of that become very powerful at scale because every additional restaurant adds high quality revenue with very little incremental capital required.

Today there are roughly 3,000 stores globally and management believes there is eventually a path to 10,000 stores. Even if they only get to around 7,000 stores over the next 6 years, the math already becomes extremely interesting. At roughly 14% annual unit growth, they would approach around 7,000 stores by the early next decade.

Now assume each restaurant eventually averages around $2.5m in AUV. They are guiding for $3m eventually, but I want to stay conservative. I do not think $2.5m is some absurd assumption considering domestic stores are already approaching $2m today and they still have pricing power, operational improvements, digital growth, and international runway. At 7,000 stores, system sales would approach roughly $17.5b annually. Since $WING collects around 5.5% royalties on those sales, royalty revenue alone could approach nearly $1b annually.

This is the part I think people really underestimate. Royalty revenue is incredibly good revenue. The incremental economics start resembling software, licensing, or index businesses far more than traditional restaurants because incremental revenue requires very little incremental capital. Even if you assume only 50% operating margins, which is conservative, $WING will generate close to $500m in operating profit.

After taxes and other expenses, maybe normalized earnings power eventually lands around $350m to $400m annually. Then on top of that, you also have buybacks steadily reducing the share count and dividends continuing to grow over time. Buybacks become especially powerful in royalty style businesses because every remaining share owns a larger percentage of an extremely high quality recurring cash flow stream.

This is another part of the story I think people are missing. If the business eventually earns around $375m annually and the share count declines to roughly 25m shares through ongoing buybacks, that would imply around $15 in earnings per share. If management eventually decides to return even 35% to 40% of earnings back to shareholders through dividends, that would imply roughly $5 to $6 per share annually in dividends.

At today’s roughly $125 stock price, that would equate to around a 4% to 5% yield on cost for someone buying shares today, and that is before considering continued buybacks or future dividend growth beyond that point. In other words, investors today may not just be buying a growth story. They may also be buying a future high cash yielding royalty business once the system matures further.

At a 25x multiple, which honestly does not feel unreasonable for a business with these types of economics, runway, and returns on capital, you could justify something around a $375 stock versus roughly $125 today. That would imply roughly 20% annualized returns before even including dividends. The important thing is this does not require some fantasy scenario with absurd leverage, impossible margins, or unrealistic same store sales growth. It mostly requires continued unit expansion, stable franchise economics, and reasonable AUV growth.

1/2 👇

English

@realroseceline I took paid subscription of your substack and able to DM in substack, could you please check when you get chance

English

@devineni6 I don’t do dms, sorry. All my interactions are public

English

I bought a new stock for my portfolio today. Only the second new position I have started this entire year.

It is a $3.5b small cap non tech company that I have admired for many years, but I was never able to buy it because the valuation always felt too expensive. I think one of the hardest things in investing is accepting that a great business and a great investment are not always the same thing. Sometimes the business is incredible for years while the stock itself is a terrible investment simply because expectations and valuation became disconnected from reality.

Ironically my first purchase this year was $NOW, which at the time was considered one of the worst buys imaginable on this platform and I got totally killed in here. People were acting like the business completely broke overnight. A few weeks later sentiment flipped and suddenly it became a loved companies again. The fascinating part is the actual business barely changed during that period. Mostly the stock price and the narrative changed.

That is one of the biggest lessons over time. Social media sentiment moves much faster than business fundamentals. Investors often confuse volatility with change. A stock declining 25% does not automatically mean the business is suddenly 25% worse.

Another thing I have learned is that patience in investing looks stupid until it suddenly looks disciplined. I only bought 2 new stocks this year because truly great opportunities are actually pretty rare. Most people trade constantly because activity feels productive, but some of the best returns I have ever had came from doing almost nothing for long stretches and then acting aggressively when price, expectations, and quality finally aligned.

What interests me most is not next quarter or even next year. I care far more about what this business can potentially look like 5-10 years from now. Is the moat strengthening? Are the unit economics improving? Does management allocate capital intelligently? Those questions matter infinitely more to me than whether social media currently loves or hates the stock.

I no longer really share my exact buys and sells publicly the way I used to. Not because I am trying to be secretive, but because I do not want people blindly copying me without fully understanding the risks, valuation, time horizon, etc. A stock that fits my portfolio, psychology, and long term expectations may be completely wrong for someone else.

I think social media has created this idea that investing is about copying and cloning instead of thinking. But real investing is much deeper than that. Two people can buy the exact same stock and have completely different outcomes because one understands what they own and the other is simply following a narrative.

🌹

English

$MSFT

$HIMS

$BIDU

$NMM

$NOW

$ORCL

Are all buys....

Hold for 18 months, and these will perform incredibly well.

English

@realroseceline I found substack and subscribed of yours and did send message over substack.. could you please check when you get chance

English

@realroseceline Was able to send you DM in substack.. pls check when you get chance.. Thank you 👍

English

@realroseceline Wanted to know are you active on substack? Is there way I can DM you?

English

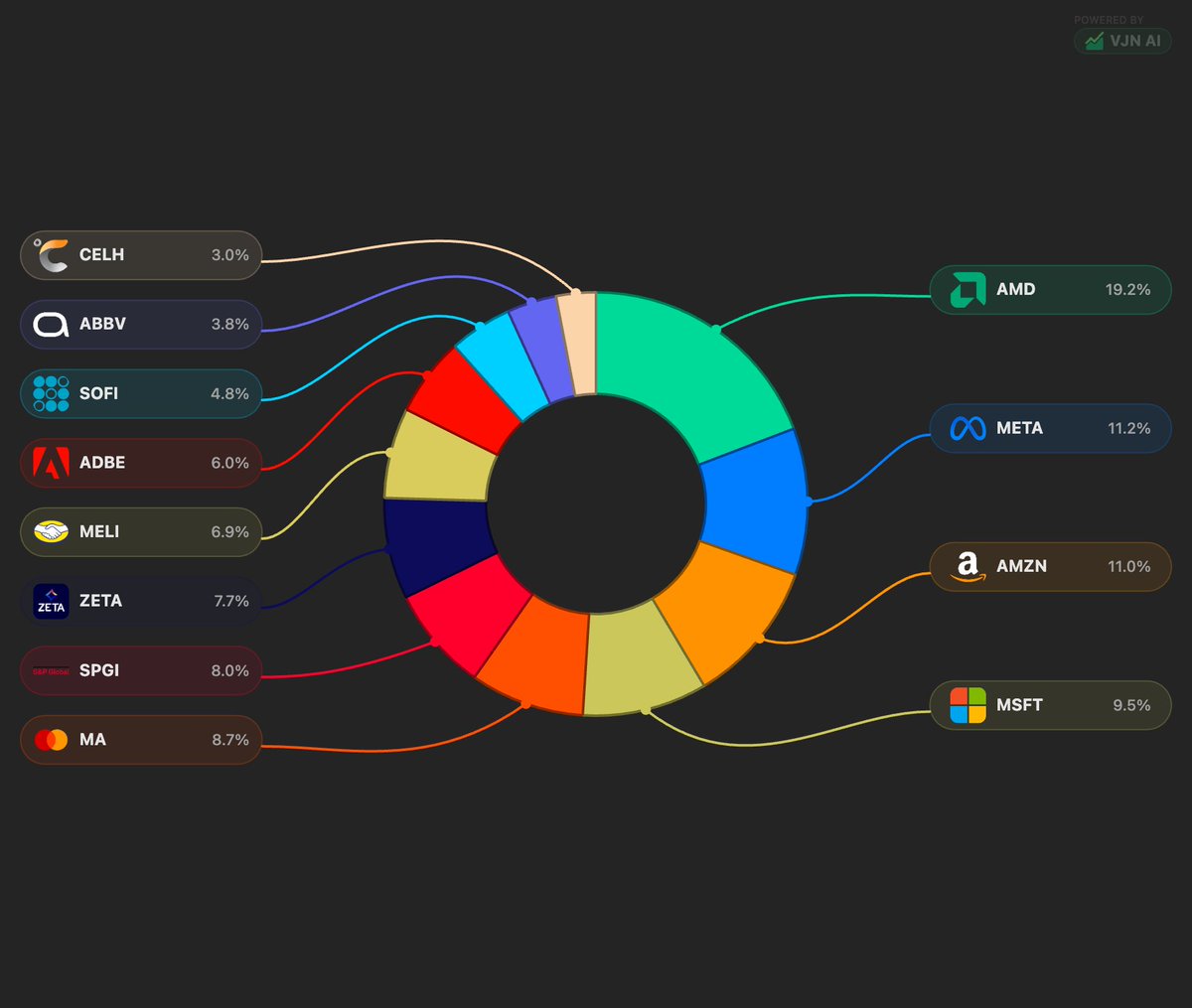

How would you rate this sample portfolio on a scale of 1-10?

25% $AMZN

20% $MA

20% $META

15% $MELI

12% $NOW

8% $TSM

English

@eenLien @offersforus Learnt one thing with these kind of things,, always be limited with sizing on these so we won’t get pressure then we set them and forget it

English

@offersforus We'll see... With Enovix, always be cautious with expectations.

English

$ENVX 🇲🇾 Enovix Malaysia partner (Orifast Solutions) is looking for a Supervisor Production...

👉To manage at least 20 - 30 people

👉With ability to work under pressure especially in high volume environments

🤫😇😁

English

@JackPrescottX Reserves for 3 more years the classic line 👍👏

English

Congrats to all $ABCL shareholders! Just got done listening to the call. Stock went from jumping 9% after hours to dumping 14% and now at -10%. None of that matters.

What matters right now is that 635 Phase 1 data was clean and management is confident going into phase 2. The company has $655M and Booth reiterates his classic line of “we have sufficient liquidity to fund at least the next three years of pipeline investments”.

Key priorities for the year include delivering top line data readouts for ABCL635 and ABCL575 (which we don’t care about anymore),advancing ABCL688 and ABCL386 through IND enabling activities, and adding at least one new development candidate to the pipeline.

Pretty much in line with what we were all expecting. It’s a long road but management is executing. This is good. Phase 2 readouts in Q3 are the big item on my calendar now…

Long and strong 💪

Jack Prescott@JackPrescottX

English

What is one stock I HAVE to own, but currently don't?

Always looking for new ideas.

English

@DGretta_Author Could you please share the subscription link i couldnot find it in your profile.

English

New ticker loading. shhhhh don't tell anyone yet, I'm not done buying.

English

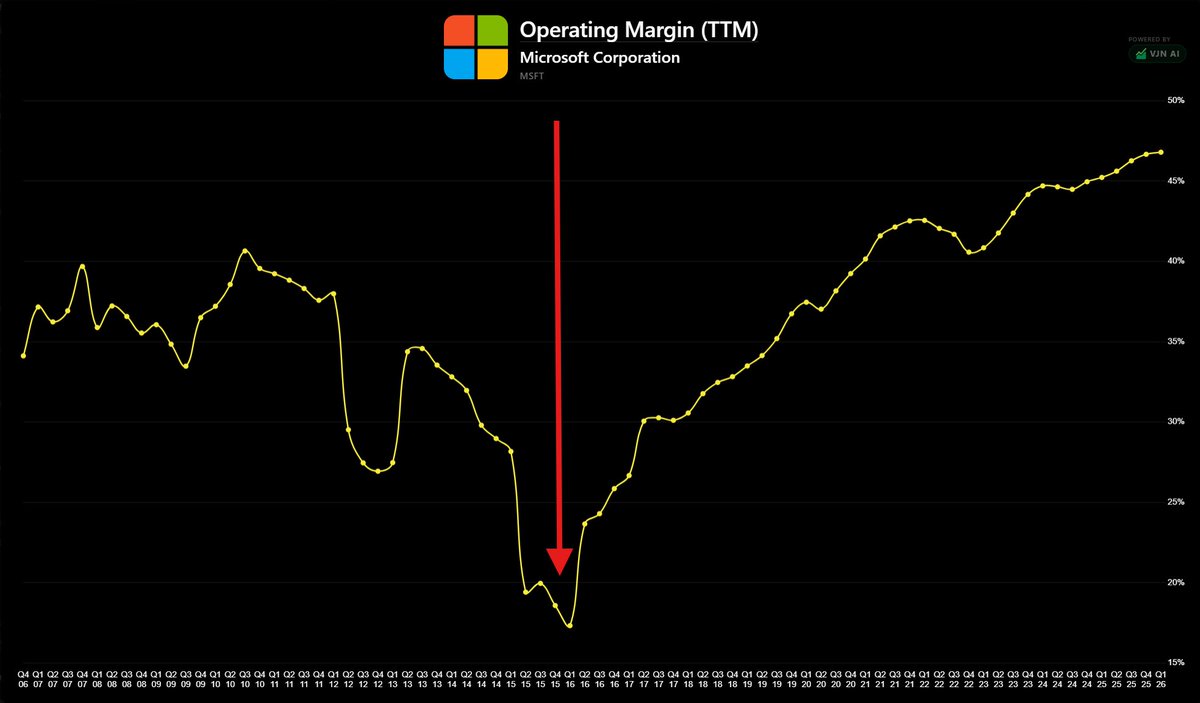

@VJNCapital But with google is providing all the docs/excel and Claude is also providing all of the Msoffice stuff for very cheap what happens to the subscription model revenue for $MSFT on msoffice related stuff ??

English

$MSFT made the switch to a subscription based model around 2016 and it is one of the most profitable decisions in history

Since then the operating margin has just continously kept marching upwards

English