Jukan@jukan05

Samsung Foundry "Targeting Profitability This Year"

Samsung Electronics has set a goal of turning its semiconductor foundry business profitable this year. It has been confirmed that the company moved up the timeline, which was originally scheduled to break even next year. After more than three years of sustained losses, attention is focused on whether the foundry can become a new growth engine for Samsung Electronics' semiconductor division.

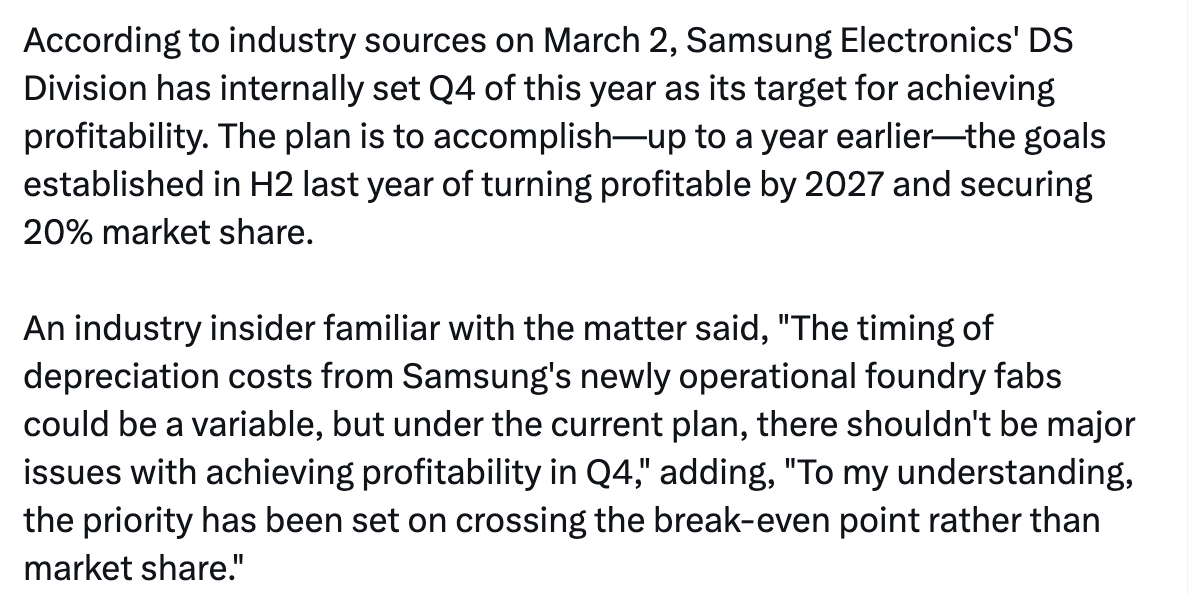

According to industry sources on March 2, Samsung Electronics' DS Division has internally set Q4 of this year as its target for achieving profitability. The plan is to accomplish—up to a year earlier—the goals established in H2 last year of turning profitable by 2027 and securing 20% market share.

An industry insider familiar with the matter said, "The timing of depreciation costs from Samsung's newly operational foundry fabs could be a variable, but under the current plan, there shouldn't be major issues with achieving profitability in Q4," adding, "To my understanding, the priority has been set on crossing the break-even point rather than market share."

Foundry is fundamentally a contract-based business. This means that approximate revenue projections can be made at the time fabrication contracts are signed with fabless companies. Samsung Electronics is analyzed to have set this target based on sales and operating profit estimates derived from these contracts.

As recently as H2 last year, when Samsung established its 2026 management targets, the company had projected profitability two years out (2027). However, as market demand expanded amid a semiconductor super-cycle and more customers turned to Samsung Foundry, the timeline was revised. This is interpreted as reflecting the major foundry contracts secured last year from big tech firms such as Tesla and Apple, as well as the continued addition of diverse customers from China, Europe, and other regions. TSMC's capacity bottlenecks driving some customers toward Samsung also played a role.

Only TSMC, Samsung Electronics, and Intel are capable of sub-10nm advanced processes. Samsung is absorbing substantial customer demand thanks to its broader range of processes, greater operational experience, and recent yield stabilization—giving it an edge over Intel.

As a result, utilization rates at Samsung's advanced process nodes are rising sharply. While rates vary by node, some cases at the 4nm, 5nm, and 8nm nodes have approached 90%. In particular, the 4nm node utilization rate is climbing rapidly as shipments of 6th-generation High Bandwidth Memory (HBM4) have commenced. Starting with HBM4—referred to as "customized HBM"—system semiconductors such as memory controllers are integrated into the bottom layer (base die). Samsung Electronics is producing these base dies in-house at its 4nm foundry process.

Another industry source noted, "The rapid ramp-up of HBM4 shipments was backed by Samsung Foundry's base die capabilities," adding, "This is a prime example of maximized synergy between the foundry and memory business units." The latest 2nm process node has also entered full-scale mass production, indicating high growth potential.

As foundry performance improves, Samsung Electronics is shedding its reputation as the company's "weak link." Samsung's foundry business had long underperformed relative to its massive investment, recording losses of approximately KRW 1 trillion per quarter since 2022. Upon turning profitable, it is expected to transition into a full-fledged revenue-generating business and serve as a key pillar of Samsung Electronics' growth.

A Samsung Electronics spokesperson said, "We cannot disclose specific management targets," while acknowledging that "it is true that foundry business performance is improving."