Sabitlenmiş Tweet

2026 FORECAST AND THOUGHTS:

These are my extremely unorganized thoughts for 2026. In short, good times at first, but mostly bad times this year, and lots of volatility.

In January, and possibly extending through Q1, expect a sharp run-up in alts and equities broadly. This rally will be driven by a perfect storm of tax-loss rebuying, gross under-allocation from sidelined players, a boost in retail from larger-than-usual tax refunds, and a favorable monetary impulse. Additionally, expect the administration to lean on the scale to juice their midterm odds. However, the optimism will be short-lived. While alts may outperform Bitcoin in January-Q1, BTC likely fails to hit a new ATH and the "rally" will end in extreme pain, failing to materialize in a sustainable bull market - similar to early 2024. This will keep the 4-year cycle theory in tact, something that no one believes in right now. I think we see a 2022-style down-only crypto market with most alts getting decimated. My guess is that BTC will eventually fall to the $38k–$48k range, which will be an all-time great buying opportunity.

For stocks, don’t expect a "down-only" 2022-style slaughter. It will look more like 2018: high volatility with the index finishing +- 5%. We are staring down a period of significant economic weakness. Housing is already in a recession, and will likely continue to be, and as the saying goes, the housing cycle is the business cycle. With labor deteriorating due to the first real wave of AI-related layoffs and the continued K-shaped economy dynamics, we will really start to see real economic weakness mid to late year, though it will not culminate in a recession as investment and government spending will be too high for that.

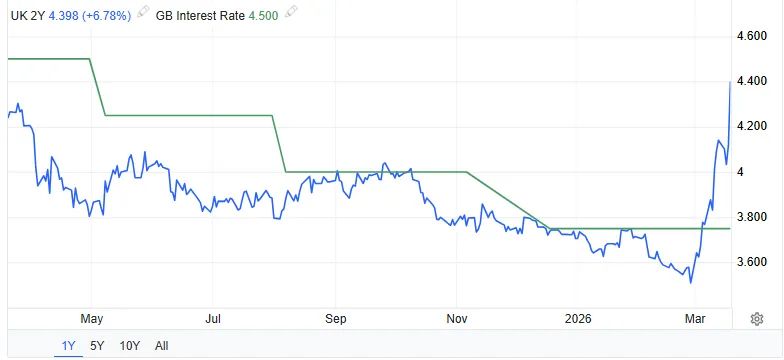

The market is currently pricing in instant rate cuts once Trump appoints a new Fed Chair, but that’s a mistake. The Fed will likely rebel to prove its independence, remaining more hawkish than necessary when Trump appoints a new chair. This will put immense strain on the economy, much more than is necessary, as the economy will continue to weaken, but will not receive the rate cuts that it needs. Furthermore, liquidity will lag behind economic needs. The Fed’s balance sheet expansion won't keep pace with the massive drain caused by the US having to refinance a mountain of debt - i.e., the liquidity base increases but does not keep up with the needs of the economic base. While AI earnings should hold up, the rest of the market, which is tethered to the "real" economy, will struggle.

I think that the economic weakness combined with a stubborn Fed will result in a shock to the economy sometime in H2 (whether it be really bad economic data, some bank failures, or funding market blow ups) that will force the administration to juice the fiscal lever and for the Fed to come in MUCH stronger than it otherwise would have had to. This will be the juice that starts the next bull move: a return of liquidity and a return of retail.

To understand the last three years, you have to understand the letter K. We have a K-shaped economy (the top 10% thrive while the 90% struggle), a K-shaped stock market (Mag 7 up, everything else flat/down), a K-shaped crypto market (BTC up, alts down), and a K-shaped Fed (pro-institution vs pro-administration). This K-shaped dynamic has infiltrated all parts of the economy, the market, and society. I expect that to continue.

The reason alts haven’t moved despite a "good" stock market is that crypto is still a retail-heavy asset class, and retail is at the bottom of the K. Retail simply has no money right now and is in a recession. In 2021, they had stimmys and low rates, but since then, retail has been in a recession, and alts have reflected that. Bitcoin, conversely, has become an institutional asset at the top of the K, thus outperforming alts. Additionally, crypto is still extremely tethered to liquidity, and since 2018, we haven't had a constant "QE push", only sporadic liquidity injections like BTFP or T-bill buying. Alts need that constant liquidity flow to shine. This results in alts getting hit twice as hard - no retail flow, and no institutional liquidity, thus the depressed prices.

The popular sentiment that "alts are dead" is particularly wrong. As the Fed eventually becomes a political, pro-liquidity institution, as alts finally start to embrace buybacks and all value accruing to tokenholders (i.e. Uniswap), and as the bottom K recovers, the very forces that suppressed alts this cycle will propel them in the next.

Wall Street is calling for a fourth straight year of +20% gains, and crypto-native circles think the four-year cycle is dead. I’m fading both. I don’t believe AI is a bubble in the traditional sense; the market is richly valued, but the earnings are real, and the earnings are coming from other businesses, so they are somewhat immune to real economy weakness. There are two real bubbles: the AI bubble bubble (i.e., the bubble about AI being a bubble), and the US AI supremacy bubble. The first is simple, in the dot com bubble and 2021, everyone talked about stocks and few thought there was a bubble. Today, everyone talks about an AI bubble. As a general rule, you always fade public sentiment. Because of this, I do not expect there to be a traditional "pop" in the AI bubble that the public is talking about. The second bubble is more nuanced: the US AI supremacy bubble - i.e., the bubble that the US is the only country where you can get AI exposure. This has forced huge multiples on Mag7 companies because US AI is the only game in town. I suspect that sometime in 2026, China will start to flex its AI strength, similar to the DeepSeek moment but at a larger scale. This will cause US tech multiples to compress as the bubble that US AI is the only game in town pops. Prices will drop while earnings hold mostly steady. The bulls will be wrong because prices fall, but the bears will be wrong because nothing actually goes to zero and earnings don't collapse. It’s a bubble deflation, not a pop.

Lastly, I expect there to be some kind of geopolitical issue that has last effects, unlike Iran/Israel that mattered for a few weeks. What that is, I'm not entirely sure. Additionally, I am highly convicted that inflation will be a non-issue, it will matter as it always does, but there is not risk that inflation reaccelarates. That said, we will likely not see a super weak dollar, in fact we could even see a stronger dollar due to the Fed lagging on rate cuts.

English