$DRX.TO CFO retiring on December 31st, and will remain a strategic advisor beyond that. Clearly an orderly retirement and I am not reading anything into it.

English

Inflexio Research

1.3K posts

@InflexioSearch

Looking for inflecting stories. special situation & long-term micro/small cap stocks. Primarily in US/Canada

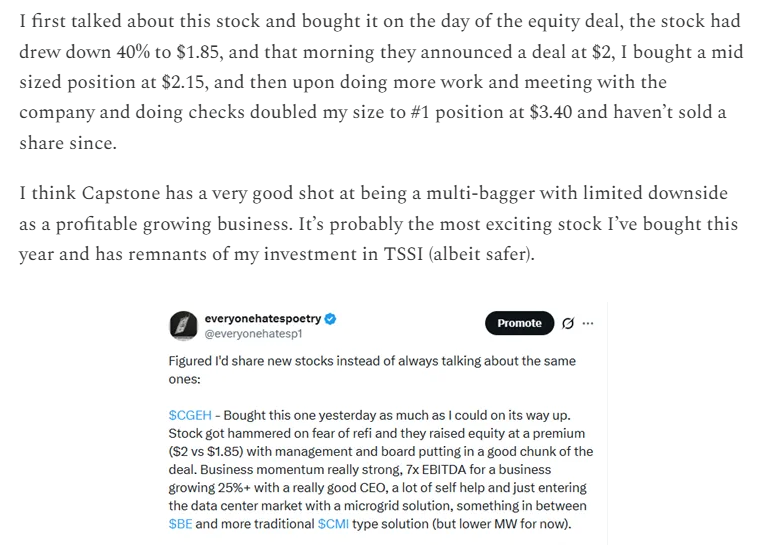

NEW PITCH: Happy to release my long-form pitch of $CGEH, the best story I've found so far this year, super excited. First mentioned it here late November, has gone up a lot since initial purchase but still think it has high odds of being a multi-bagger from here!

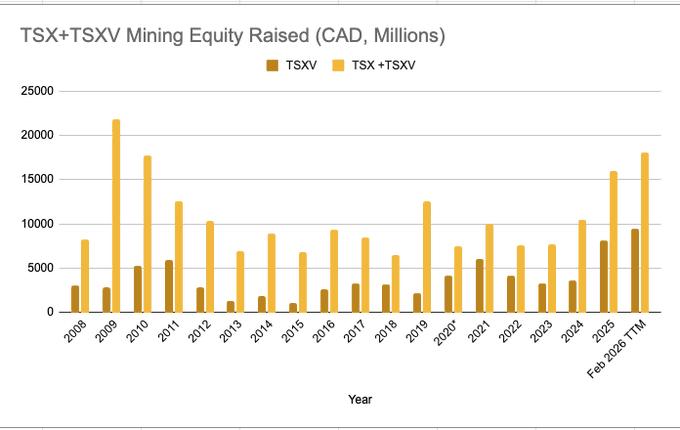

Mining companies raised ~1.3b CAD on the TSXV in March. This was only slightly below the 1.36b they raised in February 2026 & >4x what they raised in March 2025 (292m). So TTM TSXV mining equity raised still reached a new all time high in March $OGD.TO $FAR.TO $MDI.TO $GEO.TO

I am long $OGD.TO - Orbit Garant They offer Drilling Services for gold and copper companies. 72% Canada, 28% International (Chile primarily) and 65% gold/30% copper approximately 65m market cap, 100m EV, $25M EBITDA estimated for 2026 or 4x EBITDA It's a pretty simple thesis - Gold/Copper prices are very strong which will support exploration. Equity raised globally for mining companies accelerated massively starting october (Q4) of 2025, doubling versus 2024... and has continued into Q1. Exploration usually picks up 6 months following significant financing rounds. They have heavy exposure to Juniors exploration (22% of revenue) which has yet to pick-up. The drillers have seen significant competitive pricing pressure over the last 24 months and as the market tightens, that should turn into a tailwind. OGD is at 55% utilization with a goal to reach 70% and has reached 80% in prior cycles. Management has already confirmed significant pick up in bidding activity in recent months and has been an active buyer of their stock. Closest peer, and juggernaut $MDI.TO trades at 10x EBITDA and is making new highs daily. MDI trades at over $1.6m EV per rig versus OGD at $540K EV/rig. MDI has been acquisitive in the past, most recently buying a LATAM drilling company for $115m for 92 rigs ($1.25m per rig). I believe OGD would be a clear acquisition target for MDI as they fit perfectly within their strategy (North America & LATAM focus + specialized drilling) and MDI is actively looking to consolidate the market to reduce competition and pricing pressure. Founder Alexandre Pierre remains on the board, and owns 20% of the shares outstanding. He is a known seller. Selling to MDI would make perfect sense to finally monetize his full stake. Clear path to $30m of EBITDA (and more) at 6x EBITDA, and assuming $30m of net debt, it would be a $3.75 stock

$OGD.TO reported good results with revenue +10% and EBITDA +13%. Importantly, Drill utilization hit its highest level in 2 years. The commentary is bullish with utilization rates expected to further improve, and seeing 'accelerated requests for proposals from junior exploration in canada' and expects 'minimal mobilization costs' to improve utilization Stock trades at 4x NTM EBITDA while peers are 10x in likely one of the biggest exploration boom seen in the last decade

$DAC steady as she goes... BVPS now $207. 100% contracted for 2026, 87% for 2027, and 64% for 2028. $76m buybacks for the year. Earnings has started to grow again and drybulk is becoming a real contributor to the bottom line. On the negative side, they've bought 5 new containership and 2 new drybulk ships + made a new LNG investment. Their capital allocation seem to be more speculative than in the past. Containership orderbook continues to run hot at 36% of the fleet but it likely will not impact them Big position for me so given the above, I will be taking some gain on the strength. However, they have likely returned to earnings growth and discount to BV remains substantial, so I think it likely keeps grinding higher