Investy

1.9K posts

Investy

@Investy_

Investment ideas across growth, value, quality. Follow & subscribe for investment ideas. No financial advice.

Katılım Mayıs 2020

779 Takip Edilen695 Takipçiler

@Investy_ A huge amount of shares showcasing their friendly SH return policy. Also high insider ownership and a re rating could produce very reasonable returns. Not all successful investments need to be excellent businesses.

English

@RobiDeschampoo @aktien_max Wie sind denn die Abgaben in Polen oder China? Wie ist Rentensystem und Wohnraum Situation?

Wie ist Wirtschaftsförderung?

Deutsch

@aktien_max Aber wird doch überall. Wo ist Arbeit denn steuerfrei?

Sie Menschen in Polen, China etc. würden niemals so eine Wohlstandsdiskussion wie hier jeden Tag auf X starten. Da arbeitet keiner wegen Steuern weniget.

Deutsch

Investy retweetledi

Europe is on a path to destroying itself.

Unchecked immigration of millions of immigrants that burden their welfare states, bring violence and terrorism to their shores, and take over local governance, one city at a time.

Anti-capitalist policies that make it difficult for businesses to adapt their workforces to a rapidly changing competitive environment now accelerating due to AI.

A business environment and tax regime that is antithetical to startups.

The absence of any progress or innovation in AI and limited access to the compute necessary to compete.

Energy dependence due to the green movement at a moment when energy demands are rapidly increasing.

And now, the abandonment of the U.S. when we have asked for limited assistance — base access and flyover rights — in the midst of our efforts to eliminate Iran’s nuclear and ballistic threat which is already within striking range of Europe, after we have invested nearly $200 billion in helping Ukraine.

NATO is about to be toast. Europe’s defense burden is about to rise massively while their economies continue to fall further and further behind.

In short, Europe needs to wake up before it is too late, and it may very well be too late.

Bill Ackman@BillAckman

An important read on Europe and NATO.

English

@StephanHuber11 @Leonhard22010 Weil Beamte keine Sonderkaste außerhalb des Staats sind, sondern Teil des öffentlichen Dienstes mit eigenem Besoldungssystem.

Dein Problem ist nicht der Familienzuschlag, sondern dass du Besoldung, Kindergeld und Steuerpolitik weiter wild durcheinanderwirfst.

Deutsch

Wieso bekommen Beamte zusätzlich zum Kindergeld für das

1. Kind 300€

2. Kind 500€

3. Kind 1.000€?

Die Familie des/der Beamten/in ist zudem wie krankenversichert?

Wieso müssen Steuerzahler das alles stemmen ohne auch etwas davon zu profitieren!

Deutsch

@bundeskanzler Du bist ein Dummschwätzer und historischer Wirtschaftsvernichter

Deutsch

Was wir an Regulierung nicht brauchen, muss weg. Es muss sich etwas bewegen in Europa und zwar im Grundsätzlichen. Und deshalb ist die Rolle der Bundesregierung in Europa ganz wesentlich: Wir sind Antreiber in Sachen Bürokratierückbau.

Deutsch

@RadioGenoa Agreed, this has been the incentive and plan of established parties all along

English

Merkel unveils her plan and hopes that immigrant votes in Germany will surpass those of the AfD. She has devastated Europe and should be serving a life sentence.

English

@th3_m0l3 @GREYxCAPITAL Besetzen und Gebühr erheben wäre fair, um Iran an den Kosten für den US Steuerzahler zu beteiligen.

Es kann nicht sein, dass der Amerikaner, euch der Europäer, die Zeche für einen Terror Staat zahlt

Deutsch

@GREYxCAPITAL So dumm ist Trump nicht.

Er wird es besetzen und übernehmen.

Entweder direkte wirtschaftliche Beteiligungen durch US Unternehmen oder er erhebt auf alles eine Nutzungs- oder Transaktionsgebühr.

Deutsch

Breaking News!

Die USA haben nun militärische Ziele auf Kharg Island angegriffen, allerdings ohne die zentrale Öl-Exportinfrastruktur zu zerstören. Die Insel ist der wichtigste Exportknoten des Iran und wickelt rund 90 % der iranischen Rohölexporte ab. Parallel dazu wurde signalisiert, dass auch direkte Angriffe auf Öl-Infrastruktur möglich wären, falls der Iran die Straße von Hormus weiterhin blockiert. Diese Meerenge ist wie schon unzählige Male erwähnt, der wichtigste Energie-Transportknoten der Welt. Noch ist unklar, ob die jüngsten Schritte vor allem Teil einer Verhandlungsstrategie sind! Zumal geopolitischer Druck häufig dann erhöht wird, wenn die Finanzmärkte geschlossen sind.

Was außerdem spannend ist & eine weitere mögliche Wendung in der Krise ist: Öltransporte nur gegen Zahlung in Yuan?

Der Iran erwägt offenbar, Öltanker wieder durch die Straße von Hormus passieren zu lassen, allerdings nur unter einer Bedingung: Das Öl müsste in chinesischen Yuan statt in US-Dollar gehandelt werden.

Diese Idee hätte mehrere strategische Ziele:

- Umgehung des US dominierten Petrodollar-Systems

- stärkere wirtschaftliche Anbindung an China

- Aufrechterhaltung eines gewissen Ölflusses, ohne vollständig nachzugeben

Damit könnte der Iran versuchen, Druck auf die USA auszuüben, während gleichzeitig Einnahmen aus dem Ölgeschäft erhalten bleiben.

Warum aber dennoch Kharg Island der entscheidende Punkt bleibt:

Einige zentrale Fakten:

- Iran produziert etwa 3,3 Mio. Barrel Öl pro Tag

- 25–40 % des Staatshaushalts stammen aus Öl

- 90 % der Exporte laufen über Kharg Island

Sollte diese Infrastruktur zerstört werden, würde der Iran seine wichtigste Einnahmequelle verlieren! Der Aufbau einer neuen Exportstruktur wäre extrem schwierig, da Kharg über Jahrzehnte hinweg mit Pipelines, Lagerkapazitäten und spezialisierten Verladeterminals aufgebaut wurde!

Kurz gesagt:

- Wenn Kharg Island überlebt = kann der Iran langfristig zur Normalität zurückkehren!

- Wenn Kharg Island zerstört & oder besetzt wird = bricht das wirtschaftliche Fundament des Systems weg!

Deutsch

@libertas_HH @denniskoray Könnt ihr vergessen, das würde uns ja ermöglichen bei Innovation wieder annähernd mithalten zu können. Das scheint nicht das Interesse unserer Politik zu sein 😅

Deutsch

Den Spitzensteuersatz kann man von mir aus erhöhen. Aber dann bitte auch ehrlich sein: Der sollte erst bei 150.000 oder besser 200.000 Euro Jahreseinkommen greifen.

In Deutschland gilt man viel zu schnell als „Spitzenverdiener“, obwohl man oft einfach nur gut verdient und hart arbeitet.

ntv Nachrichten@ntvde

Als Teil eines Reformpakets: Union soll offen für höheren Spitzensteuersatz sein n-tv.de/politik/Union-…

Deutsch

$MELI is finished

Our video... not the company...

Longest video so far... and that was after cutting out a bunch of stuff.

It will drop this Saturday!

Who should we do next? Comment other options.

English

$INVZ @KeilafOmer

Waiting for Innoviz entry into military/defense. Come on now, your country needs your technology.

English

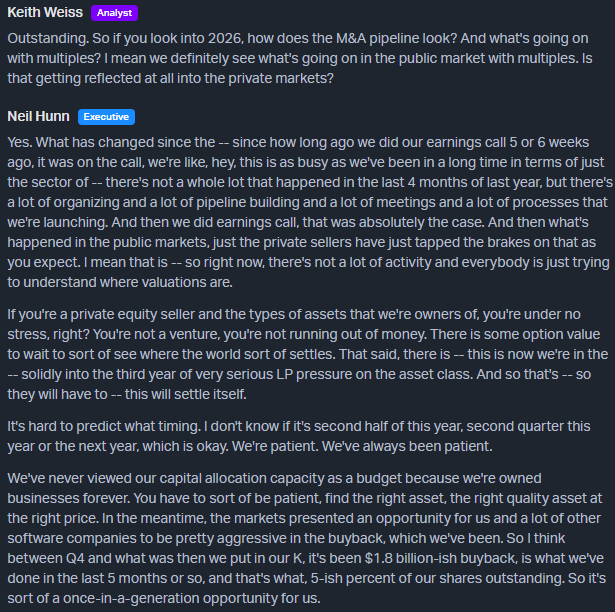

@RaleighPartners Interesting as $csu call highlighted they don't see any changes in private market valuation nor in pipeline volume.

$rop comments do make sense though, which could pressure overall deal flow from private market side for VMS acquirers

English

Comments from $ROP last week on the M&A pipeline

1. Private equity sellers have hit the brakes due to public market volatility and are waiting for valuations to settle. They are not distressed but face mounting pressure from LPs to eventually sell.

2. Roper is willing to wait for the right deals, as they buy businesses to hold forever. The company has repurchased 5% of shares over the past five months.

English

@JonahLupton @CaptainTight Yes, their Q4/2027 guide was from last year. They should've moved it out a year knowing their stock would tank with latest Q.

I'm assuming the 1b$ rev for 2029.

English

@CaptainTight I’d say mixed.. $HROW is up 350% over the past 5 years so it’s hard to dismiss that.. however I do think they were too bullish about 2025 and missed the goalposts. Now the question is whether they are still being too bullish about those 2027 Q4 targets. I honestly don’t know.

English

If you look through this thread you'll see my $HROW comments on where I think the stock can go over the next 2-3 years.

$HROW management continues to say they can get to $250M in quarterly revenues by 2027 Q4.

Their quarterly revenues are quite lumpy and that will likely continue.

They did $36.4M in 2023 Q4 revenues which was 18.2% of 2024 full year revenues.

They did $66.8M in 2024 Q4 revenues which was 24.5% of 2025 full year revenues.

They did $89.1M in 2025 Q4 revenues which would be 24.9% of $357.5M which is the midpoint of their 2026 full year guidance.

If management can really get $HROW to $250M in 2027 Q4 revenues, using 25% as our guide, it would imply they could do $1B of revenues in 2028.

$HROW has already said margins will be expanding rapidly over the next 3-5 years but lets be conservative and say it's only 450 bps better (150 bps per year) than the 22.7% ebitda margins they did in 2025... which implies 27.2% ebitda margins in 2028... which implies $272M of ebitda...assuming they get to $250M in 2027 Q4 which sets them up for $1B in 2028... using a very conservative 22x multiple on NTM ebitda... it would put the stock over $150+ per share (with $50M of net debt and 38M shares outstanding).

Keep in mind I'm being conservative with my margin estimates and my multiple estimates... both of which could be 10-20% higher... meaning ebitda margins could be over 30% by 2028 and that ebitda multiple could easily be 26x or higher if the company has de-risked the story and executed well enough to hit these numbers... in that scenario the market will reward them with a higher multiple considering how much FCF they'd be generating.

In closing, if $HROW management is telling the truth and they can indeed get revs to $250M in 2027 Q4 which should set them up for $1B in 2028, and ebitda margins can expand by 150-200 bps per year (for next 3+ years)... then this could easily be a $150+ stock in 2028

NFA.

DYOR.

**We own $HROW at @FirstWaveFund

James DePorre@RevShark

I am long $HROW. This is a good summary of why. As I have written several times, management has done a terrible job of managing expectations; as a result, investors were too focused on the short term, which undermined the long-term positives. @JonahLupton

English

@AuditTheHerd @Eyal__Weiss Expand how they can fix their major channel?

Clearly they'll diversify across other channels, which do you think they should add?

English

What’s your definition of risk? Short term margin and revenue pressure? If it’s complete business failure, I would disagree,

I work in commercial finance and have done a lot of work in e-commerce CPG. This happens more than you think. Albeit not at the severity of Oddity but still prevalent. It takes a time to reset algorithms in marketing and there are plenty of channels to market in.

English

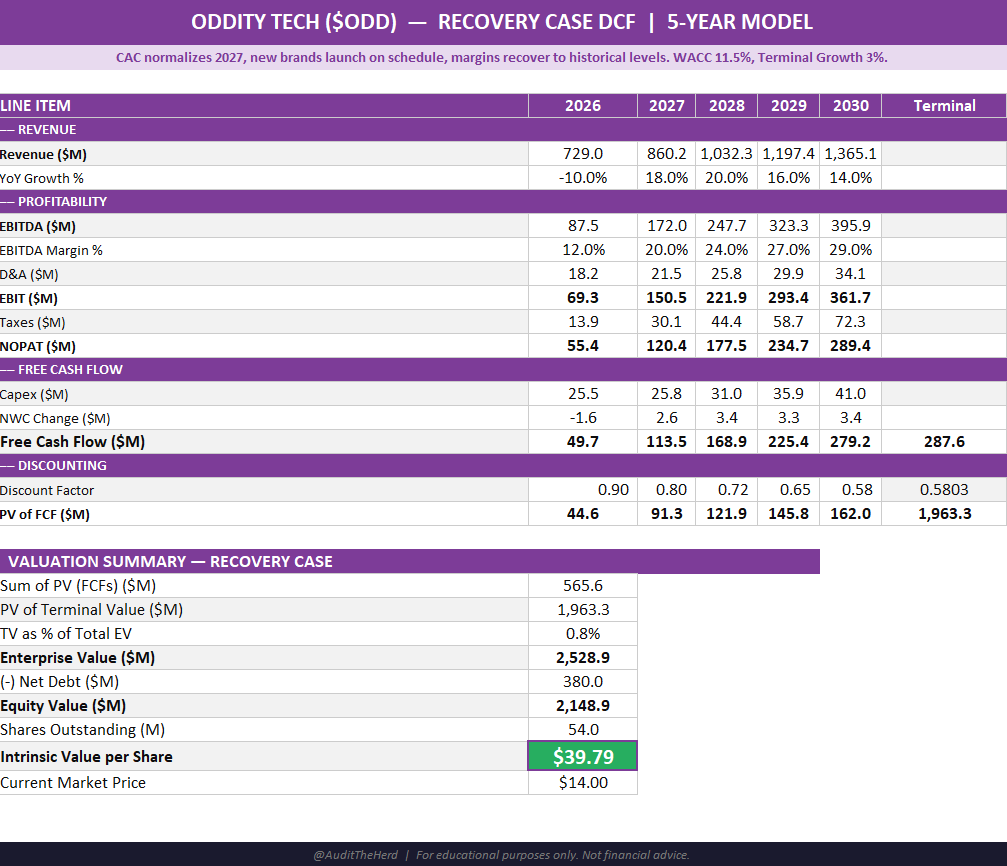

$ODD Recovery case summary

My thesis:

Q1 2026 was the bottom. (I don't think that the 30% haircut will be that bad).

Management resolved the algorithm mismatch.

CAC normalizes by mid 2027.

METHODIQ scales on plan.

Brand 4 launches 2027.

I am only assuming a -10% YoY impact for 2026 with slightly lower growth in the next few years. If I am wrong on this, you could assume a -20/-30% impact in 2026 with higher growth in the following years of 20%+ and get to around the same FV of $40.

The DTC playbook is proven with a small bump in the road. IL MAKIAGE and SpoiledChild both recovered from early setbacks and scaled profitably.

5 Year Outlook:

FY2026: $729M revenue (-10%) — trough year

FY2027: $860M (+18%) — inflection as CAC normalizes

FY2028: $1,032M (+20%) — Brand 4 ramping

FY2030: $1,365M (+14%) — durable platform

Margin Recovery:

FY2026: 12% EBITDA (crisis contained)

FY2027: 20% EBITDA (back to historical)

FY2030: 29% EBITDA (platform leverage)

Margins are achievable through cross sale of new brand 3 & 4 and leverage with scale (assuming CAC is fixed).

Valuation:

Intrinsic value: ~$40/share

Current price: $14/share

My assumptions:

WACC 11.5%

Terminal growth 3%

Net debt $380M (improving with FCF generation)

What Has to Go Right:

CAC normalizes 2027, METHODIQ scales, Brand 4 launches successfully, no further algorithm disruptions, consumer trust holds.

At $14, you're paying for near total failure. Recovery case implies significant upside.

Disclaimer: This is far lower than my previous model of $140. Keep in mind, that FV was based on a 10 year outlook with assumptions that growth and EBITDA remained consistent. NFA.

English

@weary_centurion Most important point you're missing, they've been riding one marketing channel w/o backup, no alternative, trying to fix that same channel. This was harakiri management. I hope CEO has been sleeping on one of his most important jobs because he was just blindly product obsessed

English

$ODD BEAR CASES DISPROVED🧵

This thread is dedicated to bear cases I have seen purported on here, which I can now confirm are false

English

$ODD Management has been absolutely reckless. Relying on only one channel would be like relying on only one supplier of your key raw material. Purchasing managers know they always need a second supplier as a fall back. Anything else is pure recklessness. Can they rebuild trust?

English

@Speedwell_LLC What other verticals are they considering? CFO mentioned repeatedly they will continue to add new verticals like in the past

English

We will be hosting the Shift4 CEO and CFO on our podcast in 2 weeks.

What questions do you have for them?

$FOUR

English