Sabitlenmiş Tweet

Semiconductors would like a word. Never get too cute. Ego investment is a death kneel in markets. Pivot fluidly and with grace. It’s ok to be wrong.

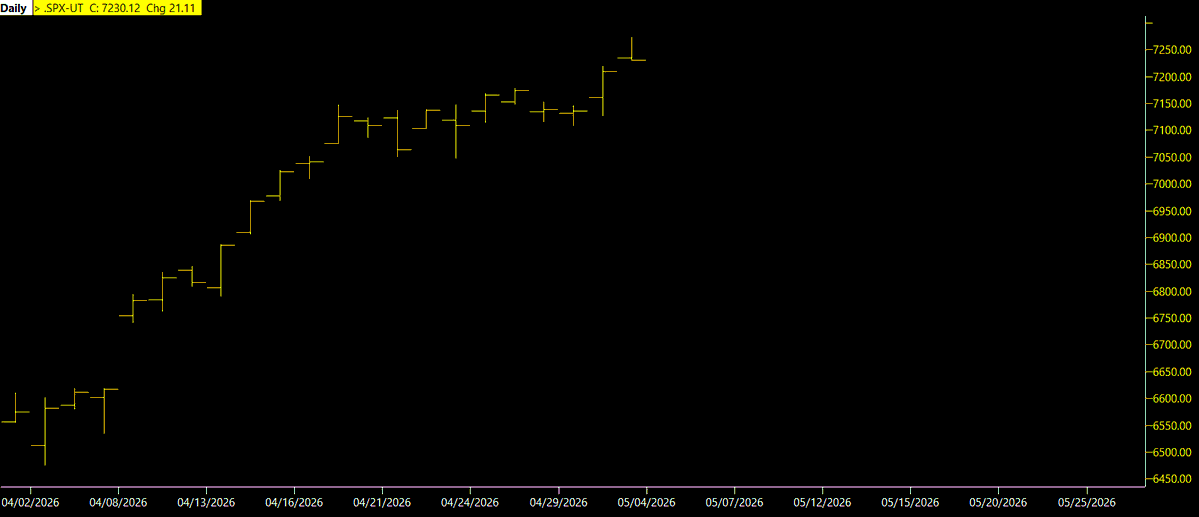

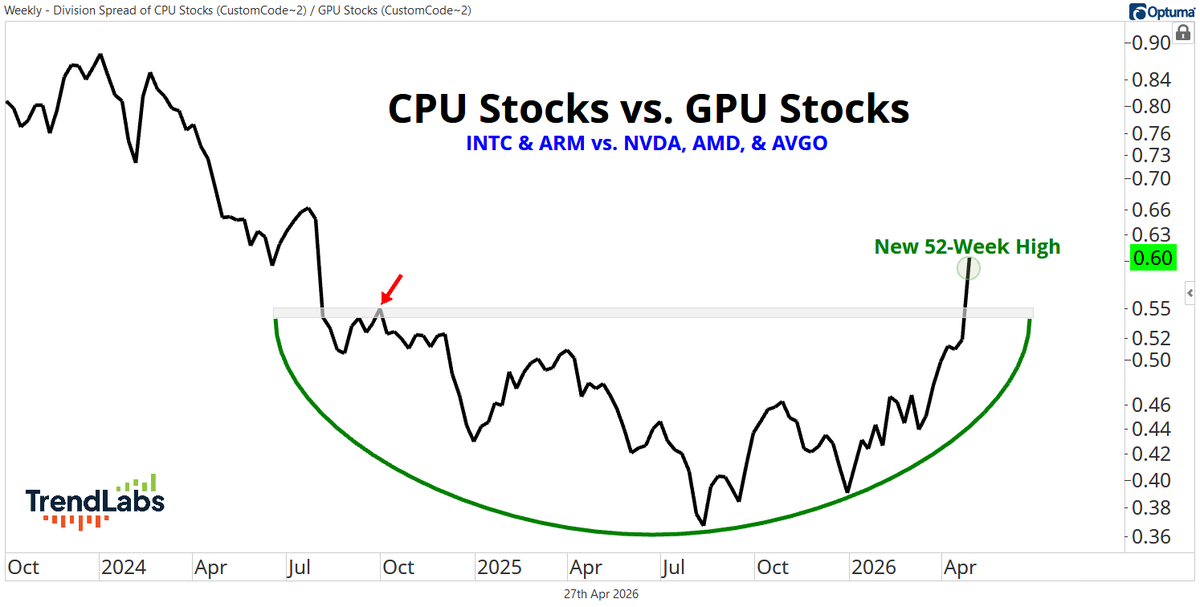

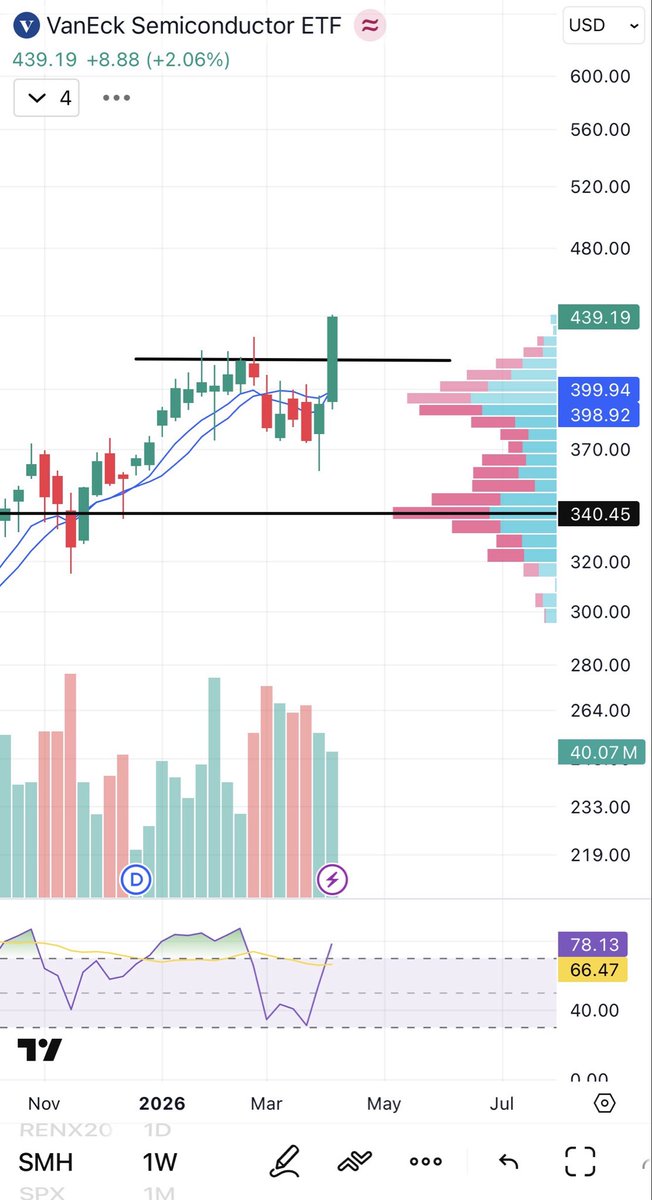

1) semis new ATH

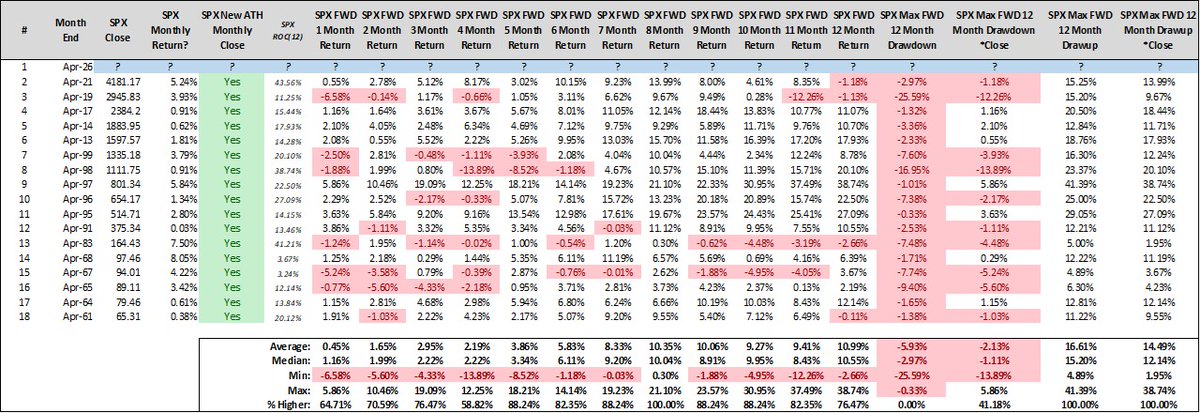

2) SPY weekly back above 680 (pending today’s close)

3) SPY weekly above the 61.8% of the ATH to interim low (pending today’s close)

These 3 put a massive dent in the bearish thesis.

Ben Kizemchuk@BenKizemchuk

7% in 7 days, -2% of ATH.... People forget what that those first bear market rallies often look like, before its officially called a "bear".

English