Sabitlenmiş Tweet

DoN

52 posts

DoN

@JMAN0670

Double or Nothing | M&A professional by day | Heavily concentrated small-cap value investor by night. Nothing is financial advice.

USA Katılım Mart 2014

261 Takip Edilen114 Takipçiler

@LoneWolfTwit58 @rsosa8 awesome, that’s a positive answer. much appreciated

English

DoN retweetledi

$GNRC $ACFN $100 LFG

“Although our fourth quarter results reflect a softer outage environment and lower shipments of home standby and portable generators, our momentum in the data center end market has further accelerated as we continue to develop our position as a key supplier to multiple hyperscale customers which are expected to add significant volumes to our backlog over the next several quarters,” said Aaron Jagdfeld, President and Chief Executive Officer.

English

@Fierce__beast Curious why they would use operating cash flow for debt pay down when the strategy is either longterm lisence deals or asset sales? Companies don’t typically use up cash flow when debt can just be extended. Your other points are business risks. Assume you’re short?

English

One example of this today is $PLBY.

By my estimates $PLBY will likely spend all of its operating cash flows on paying down its debt. So yes this deal announced today helps it, but also cannot hide the concern that its operating business is in pretty bad shape. Can they keep pushing out new license deals? Maybe but what if these license deals get renewed in a year but no partner wants to renew at current rates or just cancel all together? What if next quarter a few cancel, or the declines in their store business accelerates?

Fierce_beast@Fierce__beast

For $ANGI not even cost cuts seems to help the stock. For declining businesses cost cuts may only be perceived as temporary cash flow boosts. Stock goes up initially but then normalizes to what its true value is and in most cases is just going to be anchored a lot to its terminal growth prospects

English

@JMAN0670 Yeah im just trying to be conservative, because the thesis is really compelling even if that's all the get.

English

$PLBY more people doing the math today.

My numbers, welcome pushback if I am getting any of this wrong.

Fully diluted now ~$275m. Net debt end of Sept was ~$130m. For simplicity assuming $45m purchase price proceeds received today + $5m FCF, pro forma net debt is $78m. So call it $350m EV. What do you get?

1. China licensing business.

Worth thinking about the implied mark on the 50% sale. Annualizing last Q, China revenues are ~$12m. UTG is paying $122m (front loaded) over 8 years for half of this...which is eye-popping when you consider the min guarantee is $8.3m + another $3.3m the first three years - i.e. UTG is paying PLBY almost all of the existing business' revenue as a guarantee...which tells you they have extreme confidence in being able to meaningfully grow this revenue stream. (unsurprising given PLBY's China licensing used to be $40m)

PLBY participates in any upside presumably once UTG's 50% distribution equals the min guarantee - i.e. after $16.m of cash flow.

PLBY trading some upside for less risk and a partner that can better navigate China, but they presumably see some upside to their distribution. Say they earn $11m in revenue from this annually.

2. Ex-China licensing

$20m guaranteed annually from Byborg, with 25% of the upside beyond that. Like UTG, clear Byborg expects upside to that guarantee (hence their big equity stake in PLBY). Call it $22m annually to PLBY.

Other licensing. Already running at >$15m. Significant upside to that over time from endless monetization angles: playmate paid search, night club, etc.

So call it $35m annually for core licensing.

Adding China back --> ~$45m of extremely high-margin licensing revenue (90% gross margin today), with most of that guaranteed. Last Q, ex Honey Birdette opex was ~$9m, but ~$2.8 was one-off legal and severance costs. So closer to $6m or $24m annualized. Room for that to come down. $20m EBITDA?

High margin, largely guaranteed royalty revenue attached to incredibly durable IP, with optionality for long growth runway... 20x EBITDA? = $400m EV.

3. Honey Birdette

This biz is whatever, but it's growing and has decent gross margin ~60%. Expect this will get sold, I think $50m of proceeds is reasonable. That would yank most of the cost/capital out of PLBY and ROICs will explode.

Putting it together...

Net debt post HB sale, $45m UTG proceeds, and $10m of FCF --> net debt drops to all the way down to $20m. $400m EV --> $380m market cap = $3.30/share vs. $2.40 today. Fair value can compound for a long a time, given capital-light model with limited terminal value risk.

Dylan Marrello@ragingbullcap

People starting to do the math...

English

Market is fundamentally misunderstanding the $UPWK trade. @mattscottcap has an excellent earnings reaction to this evening's release. thesis still well intact.

English

Regardless of what folks think of $PLBY mgmt., it has become obvious that they are laser focused on de-levering the balance sheet. What are we left with? One of the most recognized brands in the world in an asset light licensing model with a retail call option. Undervalued.

English

@k_ristovski @CasinoCapital this, + the success of Anthropic. Why pay for a Salesforce CRM license when you can pay a contractor on $UPWK to build one for you

English

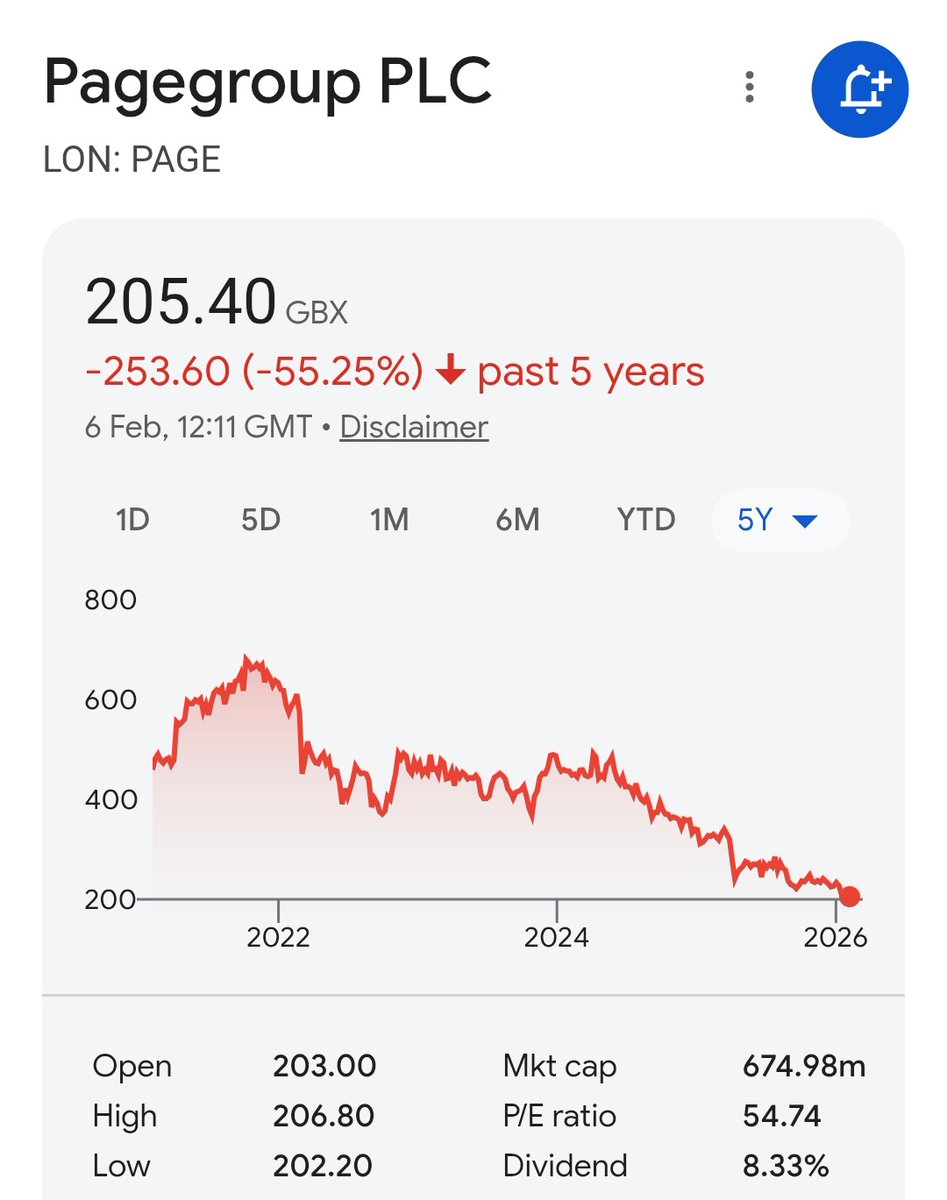

Professional services recruitment firms don't stop going down.

Our robot overlords won't need white collar workers?

English

@MagicCompounds @eriksen_tim Depending on source, seeing AIO revenue anywhere between $16M-$54M without any NA sales. Assume half of that is SaaS, and assume $ACFN can match 20%-100% of those results in NA. Low end improves GP$ by ~20%, high end potentially triples it. Obviously will need to win new deals

English

Fair points… on one hand I would have preferred the type of deal you are discussing due to the aforementioned, on the other hand this could lead to more total gross profit dollars. Would like to see them sign a contract more similar to the telco or execute on some m&a in the NTM. That said, I think prior to this the market wasn’t pricing in any deal in 2026.. so I think some uptick makes sense. Magnitude obviously is up for debate and would not be surprised if 20 is the cap on share price until further clarity.

I think the monitoring split is fine to me… it’s basically just them charging a lower cost for monitoring equipment given the high gms on that side. HW margins will likely be very low for these volumes if I had to guess.

What will you be watching for?

English

Acorn Energy $ACFN I’m not a current shareholder. While today’s news is positive it is also a bit concerning that they have to partner and thus get half their normal margins in order to get this growth versus growing organically (which was everyone’s original thesis).

English

@eriksen_tim Should also add that mgmt. has been very up front for past several earnings calls that they have been pursuing OEM relationships. To me, this falls right within that strategy

English

@eriksen_tim FWIW, heard from $ACFN yesterday. Believe strongly this brings a more fulsome offering that lowers barriers for OmniMetrix for customers that want a more holistic monitoring solution. Everything to be white-labeled under OmniMetrix brand. Accretive in year 1. Execution is key

English

@TiehackCapital + the potential value of their owned real estate (two facilities worth a potential ~$75M based on Orlando and Marquette local manufacturing /sqft values). an interesting one if Marc is open to new endeavors. been on several value screens of mine

English

@Lab_Stocks Thanks for detail, all makes sense and understandable. I guess it was just ZDGE’s turn to be an all day fader

English

@Lab_Stocks Thank you. Totally understand how day traders think. I’m more so questioning why this attracted so much early volume in the first place. Earnings were good but not company-altering. There was no reason for a pump (e.g., dilution). It just seems odd

English

There it is. $ZDGE

Lab Stocks@Lab_Stocks

There’s the rug pull. Wouldn’t be surprised to see this close in the $2’s

English