Jose Manuel Amor retweetledi

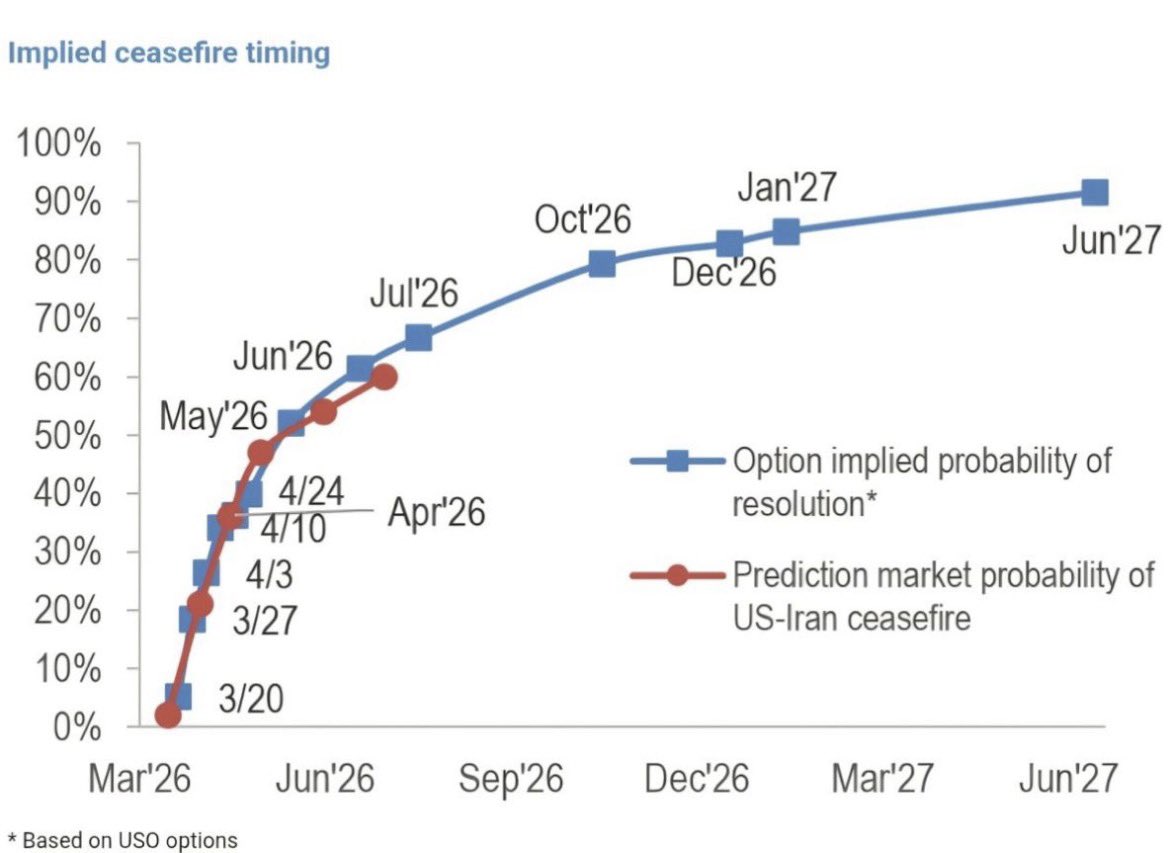

Markets are pricing both the probability and timing of a US–Iran ceasefire. Prediction markets imply ~60% odds by mid-2026, while oil options suggest a gradual resolution with risk fading into 2027. The option surface shows hedging demand, not panic, meaning markets are pricing insurance against shocks rather than a structural supply disruption.

English