Jake

85 posts

I know on very red days like today most of FinX is losing their mind, but for those who read the latest SemiAnalysis article, the new Nvidia financing model is actually giga bullish for $NBIS.

What's happening?

Nvidia is starting to backstop GPU financing.

Meaning: lenders can fund neocloud GPU clusters more easily because Nvidia guarantees a minimum revenue floor.

That solves the main true bottleneck for Nebius right now: capital.

Very important because one of the key concerns around $NBIS is "How will they finance massive AI infrastructure growth?” -> Dilution?!

If Nvidia-backed financing becomes standard, credible neoclouds can scale faster, raise cheaper debt, and sign more flexible customer contracts.

Btw I'm not 99% $NBIS as some of you wrote, I'm 100% in $NBIS rn :) IBKR dashboard is buggin lol

English

NEW ALL IN: $OUST @ $40.55

First alerted to subs at $39.88. Currently at $42.68.

They make colored lidar tech for robotics. Literally invented it.

That means 1 sensor instead of 2. With millimeter precision.

Was down -10% today on no news so it felt like a good risk / reward balance.

This is related to my overall thesis on physical AI and how there's not that many ways to play it with public stocks.

$OUST is the infra that almost every robot or physical AI automation needs. And they seem be rapidly signing up customers.

No immediate catalyst but a good one to hold.

Credit to @jiahanjimliu for the best $OUST writeup on X: x.com/jiahanjimliu/s…

---

As a reminder: this is my challenge account where I restarted with $35k to go all-in swing trading 1 stock at a time to $10M again.

Realtime alerts to subscribers. Summaries after market close to non-subscribers.

As always, please do your own research with your own independent thinking and risk tolerance and decide your own buys and sells. I may trade on a whims notice.

Kevin Xu@kevinxu

ngl this ones gonna be a banger

English

@CoffeeStocksGuy @jiahanjimliu jim, you are a good guy, I just feel bad for you, you deserve better company.

English

又是100%正确的一周。

周日夜盘进了koru,soxl,crdo,周一早盘止盈减仓。

周三盘前继续吸入半导体,大盘跌破7375止盈,反手继续做空,最低点平空,发现大盘已经处在put heavy状态,又继续抄底crdo,klac,dram,nbis。

周四继续加仓spy call。

彻底成功!

谢谢大家。

中文

@Jakeqsp2 @Momo19584530 @haochihaochiaaa 你真的是穷的想钱想疯了 好吃说的是看好meta现金牛 财报不会差 但是已经提前和大家说了不止一遍 就算财报好 都不一定百分百涨 愿意承担这份风险的可以参与 你竟然是想着百分百挣钱跟风炒股 所以你带脑子来炒股了吗?再说meta第二次财报不是给你涨回740 让你等10年了吗? 不懂下车是不是贪了?

中文

@Momo19584530 @xue_ella99112 @haochihaochiaaa 你这逻辑也是蛮可笑的 所以作为一个天天推荐股票的人 信誓旦旦的说会涨 带着大家赌财报 跌了之后几个月涨回来了就没有她的问题了?那我和你说去买任何一只股票吧 10年后会涨回来的 脑子都被洗了吧

中文

中文

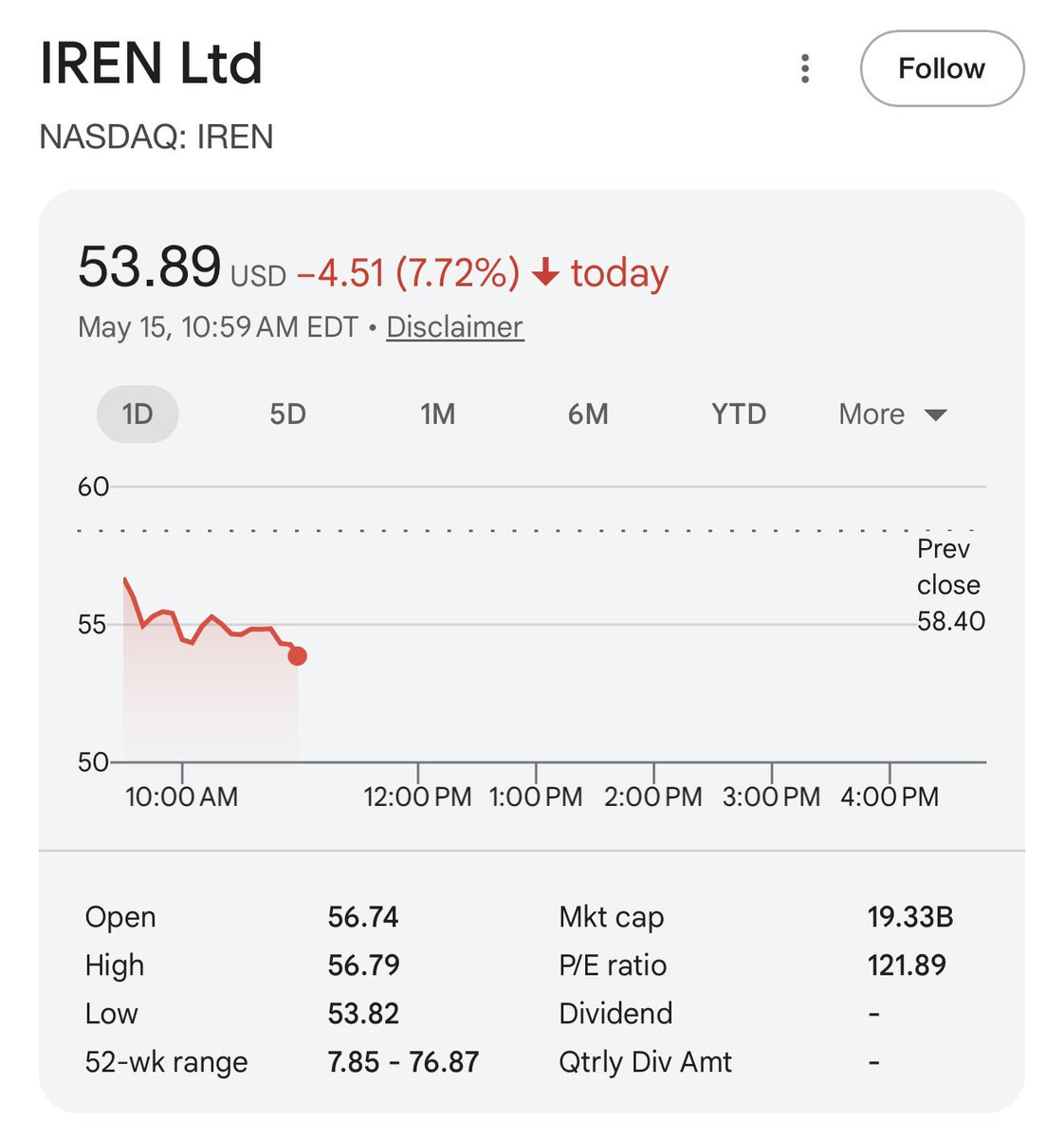

There is likely a 30-50% chance that $IREN announce a new Hyperscaler deal within the next 1-3 Months.

Shares do not currently have this priced in.

English

Many don’t want to hear this but $IREN is about to explode up. Every single thing in my analysis is pointing higher.

James@JamesTrvdes

$IREN is next, and I think we start to see lift off in the next ~2 weeks. I’m targeting a retest of ATH by June. Nuts on the line for the world to see here. Chart is reminding me of $NBIS back when I longed it in August. *Disclaimer I am long.

English

@GrindeOptions How to get you out of my list. Tired to see anything you say

English

What’s the worst performing stock you hold in your stock portfolio right now? 👀

English

@iJonJonJon @jiahanjimliu that is so true. I also made the mistake choosing iren but I didn’t spent so much time on it. Considering Jim’s time on analyzing this silly company, I feel sorry bad for him. He definitely deserve better reward.

English

@jiahanjimliu Jim you would be 20x right now had you not chosen probably the worst datacenter pick

English

$NBIS: Fantastic Job on Double Beat on Revenue and Adjusted EBITDA

Financials

1. Quarterly Revenue $399M, up 684% YoY from 50M last year. Annualized to 1.596B ARR.

2. Adjusted EBITDA positive: $130M

+17% Today: Rerating to Catch CRWV

Market is rerating Nebius to CRWV which has a 60B market cap and 35B debt for an enterprise value of 95B. Nebius is one year behind on revenue but in much better debt situation which the market likes.

They haven't announced new deals on earnings day so this +17% is from their double beat and rerating towards CRWV.

Announced yesterday was their Clarifai acquisition to improve their inference optimization. Nebius are going all in optimizing their open sourced inference solution.

Secured Power

Nebius has 4GW of secured power through a combination of colocation or greenfield. They say 4GW secured 2026 - it's secured in 2026 but power comes online anytime 2026-2031.

40% Adjusted EBITDA Margin

This is inline for a provider of mostly bare metal offering. CRWV had 56% adjusted EBITDA margin which reflects a mixed bare metal / software offering after paying colocation fees. I do expect Nebius to move towards CRWV's adjusted EBITDA margin.

Takeway for IREN

When revenue beats and ARR surpasses 1B, the rerating towards CRWV will come. NBIS Q1 last year was at 50M quarterly revenue but in this market as long as you can put GPUs online, the revenue will come. Even AKAM who lost to NET and FSLY in CDN is getting Anthropic contracts.

The market rewards when GPUs come online and are billing. The market does not give checkpoints for power secured and datacenters shells built. IREN has to get GPUs online.

Huge congrats to @MarkosAAIG who invested in NBIS day 3 of their relisting from Yandex.

Markos@MarkosAAIG

Nebius Earnings Through My View And What Most People Will Miss On The Call✍️ So guys, $NBIS just dropped Q1 2026. You all see the numbers, which are decent. Revenue $399M, up 684% YoY, beat consensus. Adjusted EBITDA positive to $130M. The headline net income of $621M is mostly a paper gain on their ClickHouse stake strip that out and they’re still running an adjusted net loss of around $100M, which is fine for a company in heavy build mode. So the print is solid. The deeper things are in the call. When I listened to the call and looked for strategic execution and what they’re actually doing, the following things is what caught my eyes the most, and which will probably be underlighted for most people. Starting with Arkady’s opening. He mentioned that they’re building across four dimensions (capacity, product, customers, and capital.) pay attention to the order here. Capacity first, capital last. His commentary strengthened essentially the neocloud case where Nebius is saying: we will build it, then we will fund it, and the funding will come because of what we’ve built. And that gives you a structurally different bargaining position with lenders and equity markets. Because when you walk into a financing conversation with contracted backlog, asset-backed-financeable customer credit, and capacity you have more influence on the terms. It comes with risk also you will see that later. The second thing that stood out for me and you all know I’ve been working on memory for a while, and a lot of people have been stressing how much memory prices will impact cost pressure for downstream for the neoclouds. Nebius secured a lot of their 2026 components in 2025 already. Andrey pointed out on the call that because of securing early, component inflation was only at a low-single-digits level as a percentage of total spend. Low single digits, while most of the industry is staring at mid-to-high single digit cost pressure for the same buildout year. So good execution on that part. Now what does this mean for 2027? Honestly, this was not addressed directly on the call. They talked about 2027 sites, 2027 power contracts, 2027 customer commitments but they did not disclose anything about 2027 component pricing. NVIDIA gave them line of sight to 5 GW of supply allocation through 2030, but that’s a volume commitment, not a price commitment. So we don’t know at what price they’re getting that supply. The risk skew is materially worse for 2027 than 2026, and you have to understand why. As you know HBM4 is a key component in the architecture of Rubin and by the time Nebius is buying Rubin systems for 2027, HBM pricing will be locked at the new contracted-tier levels we saw confirmed on the SK Hynix call, That’s a structural step-up in BOM. On top of that you have 800V DC architecture transition, co-packaged optics ramp, high-voltage power gear, switchgear, transformers with 18-24 month lead times all in constrained phases. These vendors with pricing power are raising prices. Read further 👇

English

@jiahanjimliu I feel sorry for your time and effort spent on this, all these analysis are wasted by the incapable management team

English

Let’s see what $IREN does with these convertibles as they close out old bonds, ramp up SW1 to start DC building, prepare H5-6 and get Mackenzie retrofitted. The terms of these convertibles are among the best that IREN’s ever had:

- 1% interest

- $72.87 convert price

- Oversubscribed to 2.6B

₿itcoin ₿utcher 🥩 🐑 🐷@bitcoinbutcher1

H/t @jmonroeinvest $IREN 55*1.325=72.875 exercise Capped call protects dilution up to $110 $2.6B raised will likely grow to $3B See 👇 IREN Prices Upsized $2.6 Billion Convertible Notes Offering Key details of the transaction $2.6 billion convertible senior notes offering (1.00% coupon, 32.5% conversion premium) Capped call transactions entered into in connection with the notes, which are expected generally to provide a hedge upon conversions up to an initial cap price of $110.30 per share, which represents a 100% premium (as compared to the 32.5% conversion premium under the notes) The issuance and sale of the notes are scheduled to settle on May 14, 2026, subject to customary closing conditions. IREN also granted the initial purchasers of the notes an option to purchase, for settlement within a period of 13 days from, and including, the date the notes are first issued, up to an additional $400 million principal amount of notes

English