@MoodyWriter13 @DogeChainMaxi @yourkleinod I actually like your analysis a lot. Then I think whether the company you're discussing fits with me or not and make a decision. Not that hard, people are just crazy

English

Jesus Lloret

611 posts

$SIVE has gone up more than 1,700% since I first pitched it on X. Is there anyone who bought it back then and is still holding it? That person probably owes me a coffee.

$SOX Semis UPD Thread: 1) Blow off top in progress - question is where does it end? -I find calling tops before we see rollover pointless, we are simply looking for conditions for a top and RR for any future trades -Our best matching cycle from Jan 1 analysis was 94-98 which has come to a spot where that cycle started putting a 2 month distribution top followed by 12 month correction (see updated price and close up view) -Current 3.5Y cycle is already extremely long; I think topping and correction phases will be more compressed and bottom ~Q4.

The majority of my audience is ~33, so here’s a message to you. Even though markets are currently moving lower, and headlines are filled with negative narratives pushed by mainstream media, I believe these are the moments that truly separate investors. The ability to remain objective in times like this is one of the most important strengths you can have. Over the past couple of months, I’ve been preparing you for a moment like this, consistently emphasizing diversification, maintaining a moderate cash allocation, and avoiding leverage. If you’ve been following me for a while, you already know this has become my core approach. Now it’s time to act. Now it’s time to reduce exposure to defensive sectors, gradually deploy cash, and start scaling out of hedges. When fear peaks, that’s when opportunity is created, not when everyone is euphoric. Right now, everyone is focused on narratives and uncertainty, while ignoring the fact that these moments have historically offered the best buying opportunities. I believe the macro setup is shifting. The labor market is weakening, growth is slowing, and the pressure on the Fed is building. Liquidity will return and the Fed will have to cut rates. But before that happens, I think market makers will continue pushing prices lower to force distribution and shake out participants because accumulation always requires a counterparty. So if you’re in your 30s, this is where you take calculated risk. Not at the top, not during euphoria, that’s when we were raising cash and de-risking. This is where the positioning begins. If you want to follow along, join our group. We share daily updates, reports, and focus on the next buying opportunities: patreon.com/c/cryptictrade… We’ll also be giving away five 1-month Premium subscriptions soon. If you want to enter our campaign, like and repost.

In hindsight, this will be a great buying opportunity.

$FLY, earnings looks good to me - Management delivering on their very bullish guidance: > Q1 revenue of $80.9m (+45% YoY) and reiterated $420–450m FY26 guide (i.e. most of revenue should come in Q2-4) > Stuff we already knew: Golden Dome selection + $109m FORGE ECP + a clean Alpha Flight 7 > Losses widened on R&D, but we expected this. Next catalyst probably Alpha block 2, though I am personally more excited about lunar lander and Scitec stuff

#GDP 2026 Cycles Fed database doesn't have enough data, so best we can do is identify what fits the current data set -5.5Y cycle is common across many macro data sets and if it is in play then growth should have a low around now and expand into 2027 or even 2028 - It's not as clean and given data limitations take it with a grain of salt. But given the expansion in the money supply till late 2025, I think it's reasonable to expect both inflation and growth surprise to the upside next 2 years. P.S. Projection is from July 2023

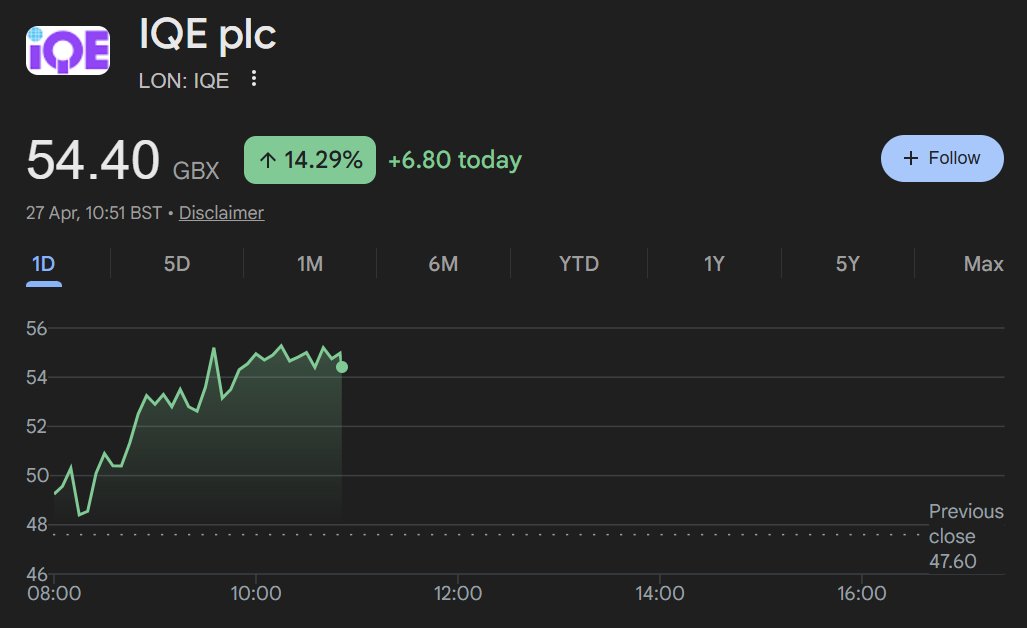

“ $IQE dropped 20%. Shall I sell?! ” No. I added heavily to my position on last week's dip. Summary on why I'm adding to my $IQE position on any dip: 1. Upstream supply chain tailwinds: $IQE's photonics & GaAs segments rely on $AXTI's substrates. $AXTI guided “sequential revenue growth in Q1 2026, driven by growth in InP for the AI infrastructure build-out.” With InP backlog >$60M and plans to 2x capacity in 2026. Since InP substrates are crucial for 1.6T transceivers and CPO: $AXTI's capacity ramp directly removes any chokepoint for $IQE's photonics epi output. And still, $IQE has internal substrate manufacturing capabilities in UK/USA - which produces GaAs, InP, and GaN. 2. Downstream demand sold out: $LITE are $IQE's flagship customer (multi yr VCSEL/EML epi partner): - $LITE has its hyperscaler order book sold out through 2028. - $LITE CEO said “we’re falling further and further behind the demand” - With agreements locking multi yr visibility straight into $IQE's photonics segment. - $NVDA $2B+ investments in $LITE & $COHR signal hyperscalers are locking in capacity yrs ahead, with epi being a huge bottleneck. $LITE's VCSEL & EML epiwafers are exactly what $IQE grows on InP/GaAs. So, locked-in multi-yr volume + sold out book = multi-yr revenue for $IQE's photonics segment. Then you also have $QRVO + $SWKS as $IQE customers for GaAs/GaN epi. It’s less obvious, but $AVGO also source GaAs/GaN epiwafers from $IQE too for its RF business - even while maintaining captive InP epi capabilities for its photonics products. 3. $IQE are an irreplaceable foundry: - patents on epi wafer growth processes (GaAs, InP, GaN) - 35+ years of proprietary tuning for yield/defect control - $IQE Serves everyone ($LITE, $COHR, $AVGO, etc.) without competing downstream - Chinese players face Western export/qualification walls 4. $IQE is different to competitors (and superior): - Substrate specialists (e.g. $AXTI): Sell raw wafers and lack $IQE's IP. - Vertical integrators ( $COHR, $WOLF, Sumitomo): Do some in-house epi but still outsource for flexibility. $IQE is purely neutral foundry - broader access, no channel conflict. - Asian players (e.g. IntelliEPI): Cost-competitive in GaAs but lack Western defence quals + geopolitical risk. $IQE wins on yield, reliability, and secure supply. $IQE's differentiation is pure-play scale + IP + global compliance = “safe” supplier for customers ----- MC forecast: I personally forecast $IQE to >2x until end of 2026 to ~£1.1B MC. Driven by photonics tailwinds materialising + strong execution - $LITE's 2028 sell-out + $AXTI's capacity doubling signal sustained (and accelerating) epi demand. Then any sale of their Taiwan ops would carry a further premium on top (Board are already encouraging bids). Imo, the 20%+ drop last week was just noise r.e. Iran, and nothing to do with fundamentals.