Jitendra Singh retweetledi

Cables and wire sector

#Polycab near all time high

#KEI near all time high

#Apar at all time high

#Universal cables near all time high

#RR CABEL NEW HIGH

Sector is well positioned for excellent move.

English

Jitendra Singh

2.3K posts

@Jitendrasaying

Stock Investor, Running, Health, Food.

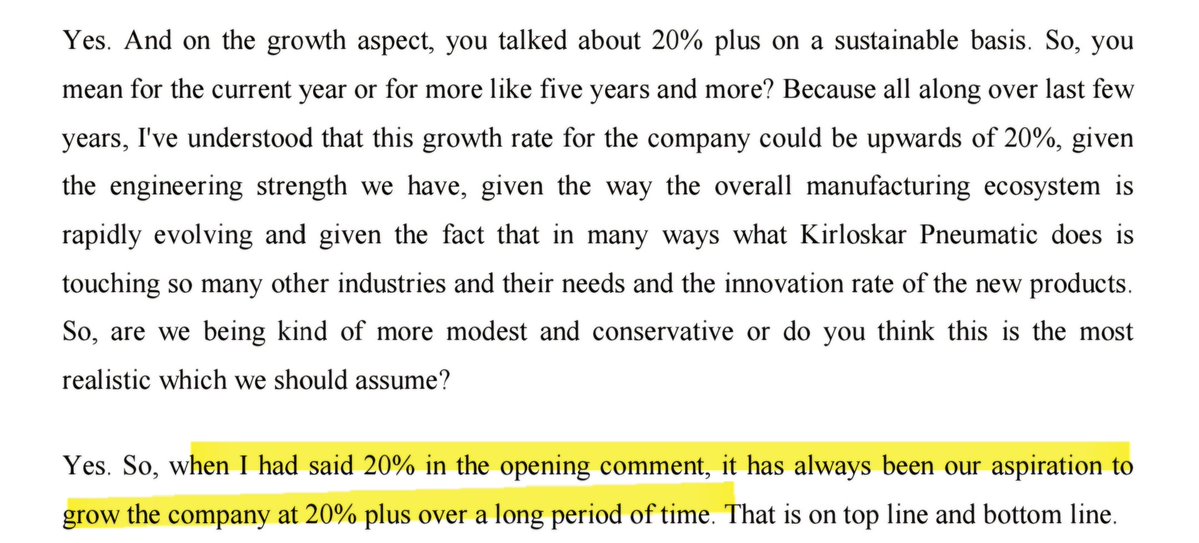

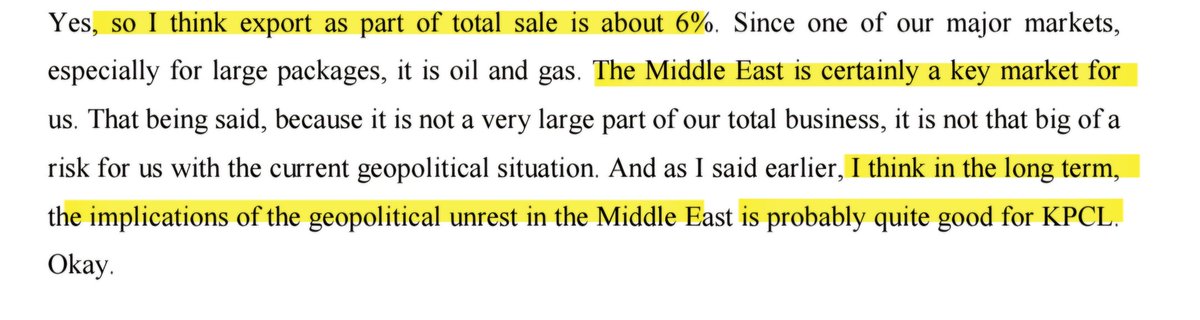

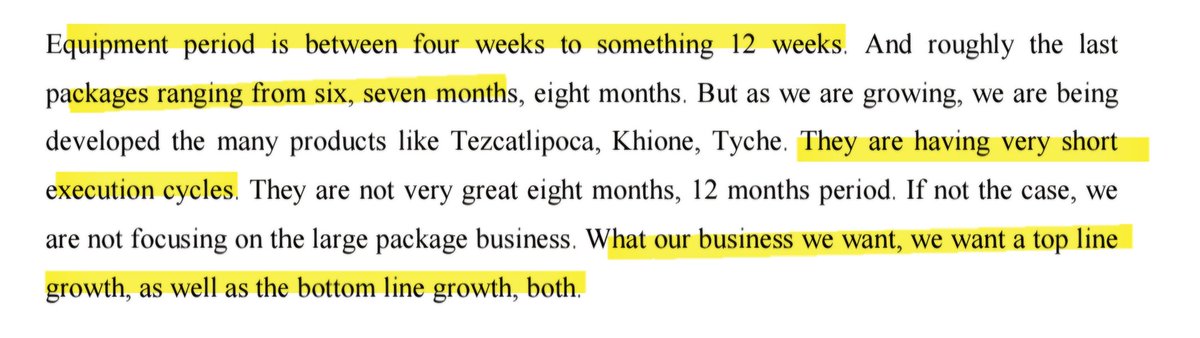

Kirloskar Neumatic & Elgi Equipments ✔️ Kirloskar Pneumatic: The Specialist • Dominant Market Share: KPCL holds a 60%+ market share in India for CNG systems and oil/gas refrigeration, and a 70% share in ammonia refrigeration • Niche Moat: It is the world’s largest manufacturer of industrial gas compressors, making it a high-conviction play on India's energy transition and CNG infrastructure ✔️ Elgi Equipments: The Global Challenger • Global Diversification: Unlike KPCL, Elgi is a global top-6 manufacturer with roughly half of its revenue from international markets like the USA and Australia • Broad Exposure: Its compressors serve general industry (Textiles, Pharma, Automotive etc.), making it a proxy for global industrial growth rather than just energy • Vertical Integration: Elgi is moving toward 75-80% in-house manufacturing of critical components like motors to control costs and global supply chains 👉 Follow @vishan_29 for more updates.

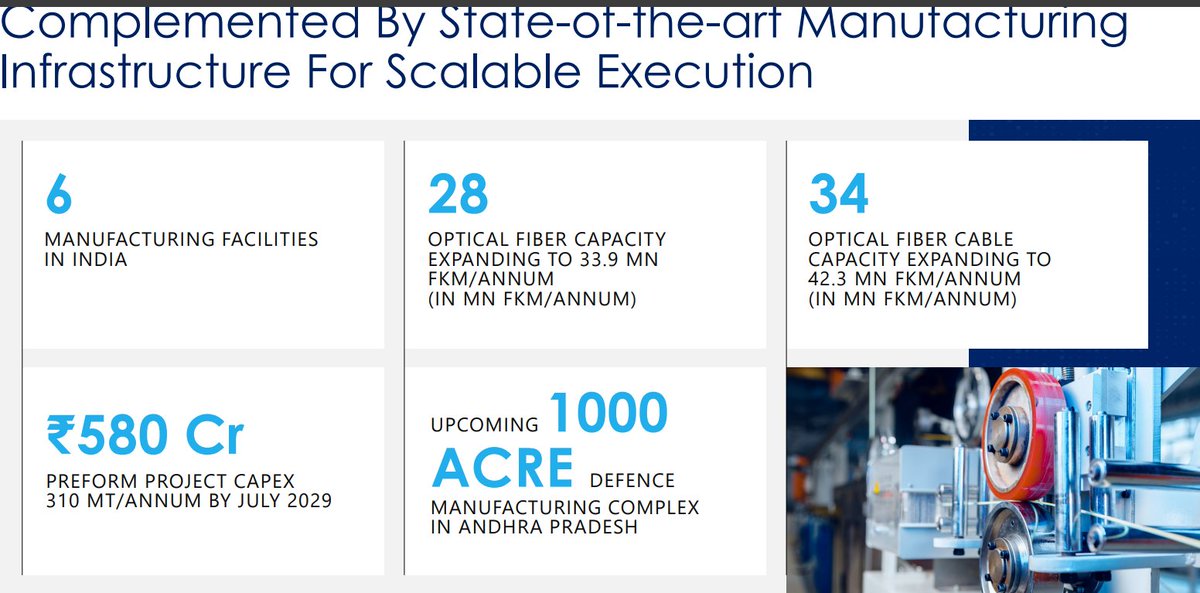

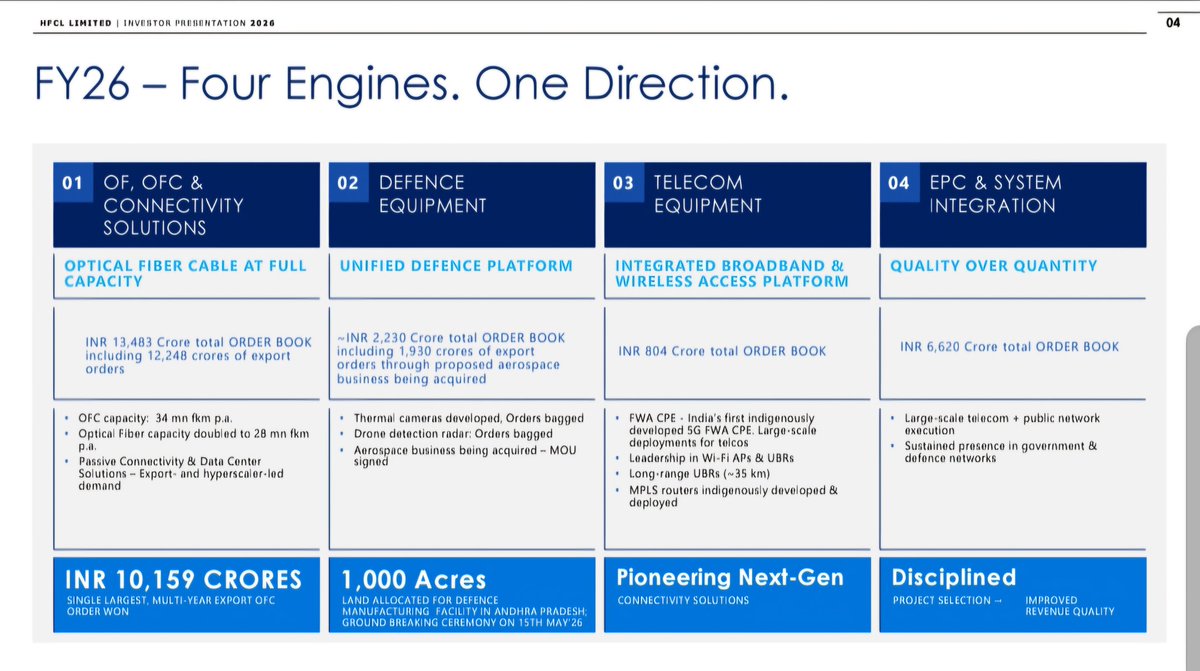

Optical Fibre Cable - structural demand tailwinds + strong pricing power + margin expansion cycle Both optical fibre players Sterlite Technologies Limited and HFCL delivered blockbuster Q4 results. Demand Drivers • AI DC - GPU racks require ~36x more fibre vs CPU, Big Tech capex at $762 Bn by 2026 • BharatNet Phase 3 - ₹65K Cr govt initiative targeting 1.5 Cr rural homes • 5G - structurally elevated fibre demand • Defence - military UAV systems consuming 50–100 Mn fkm annually • Exports - constrained global capacity, Indian players filling the gap Pricing Power -> FY27 realisations ~2.5x vs FY23

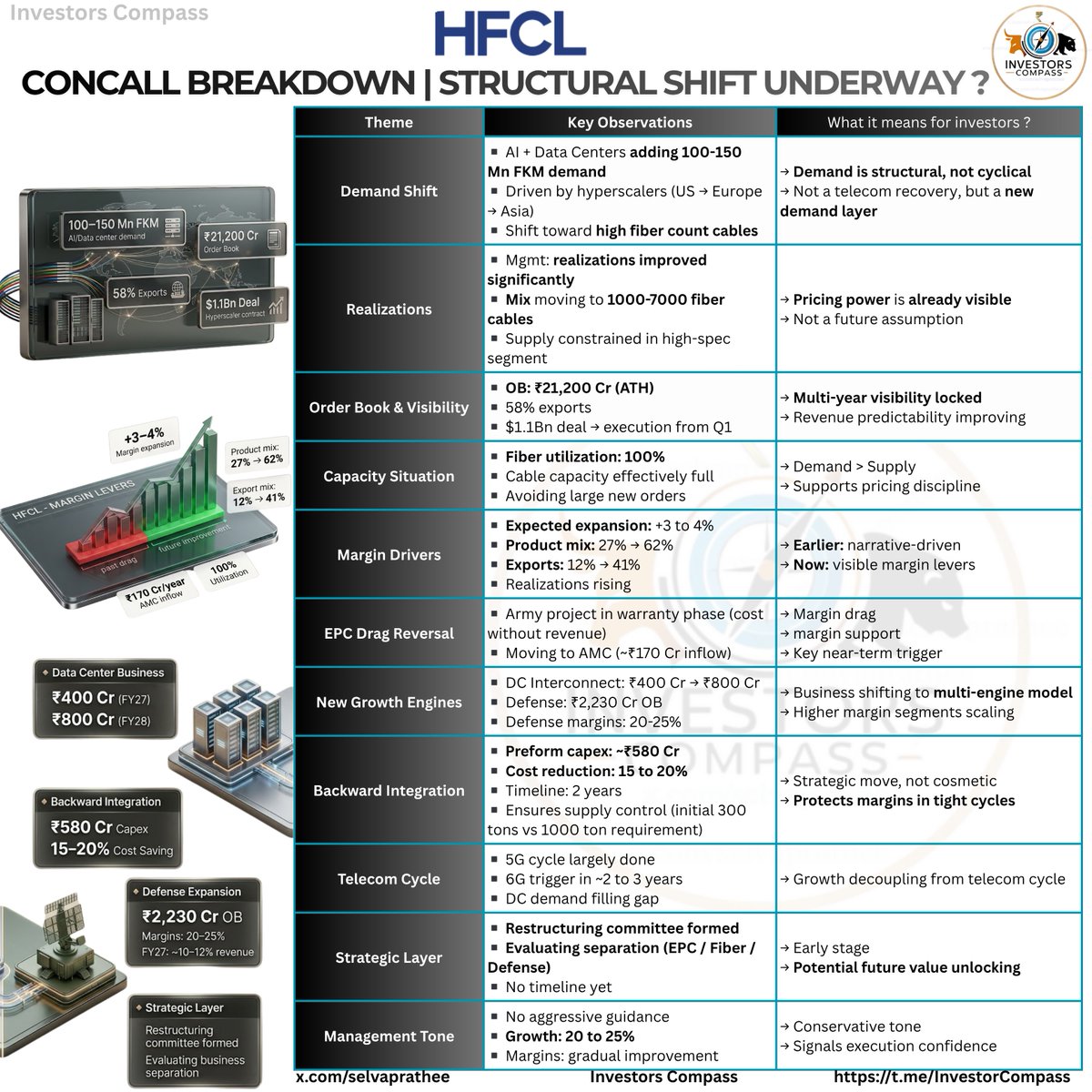

@SureshKBN Sir in #hfcl FY-29 Revenue guidance -10000 cr , Historical PAT margin near 7%, warrant (putting 555cr at 74/share) may dilute eps but many other factors may also improve PAT margin like it's preform manufacturing (310 MTPA) boosts margin by 5-6% which get operational

While the insulators & bushings remain tight in global supply.

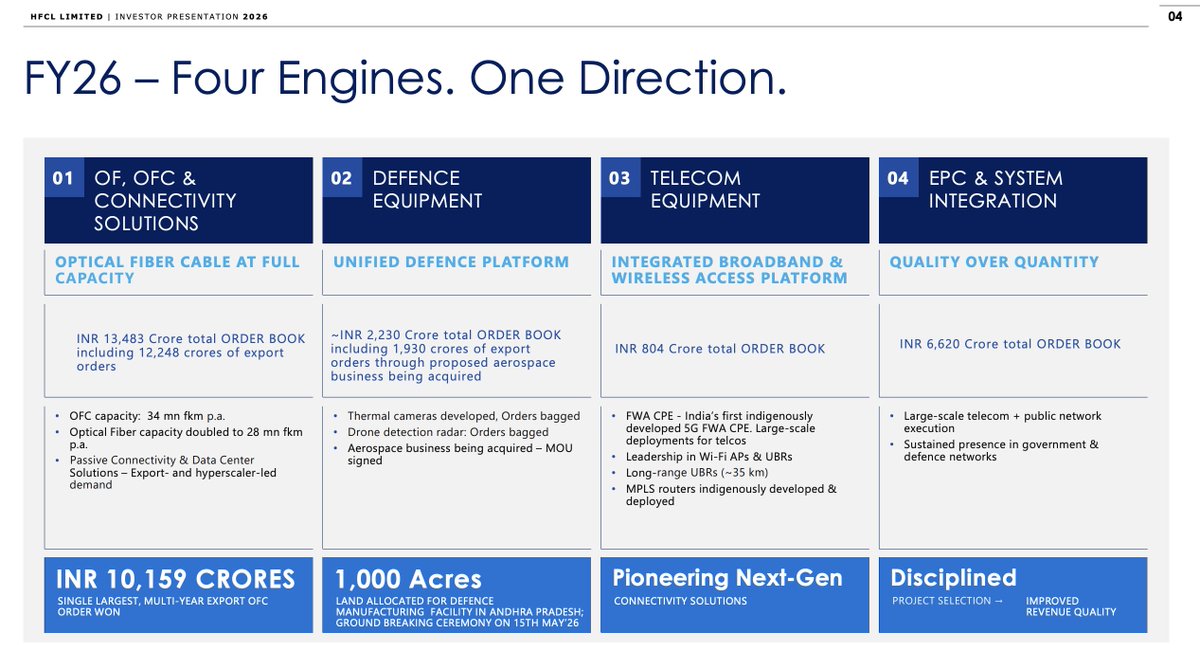

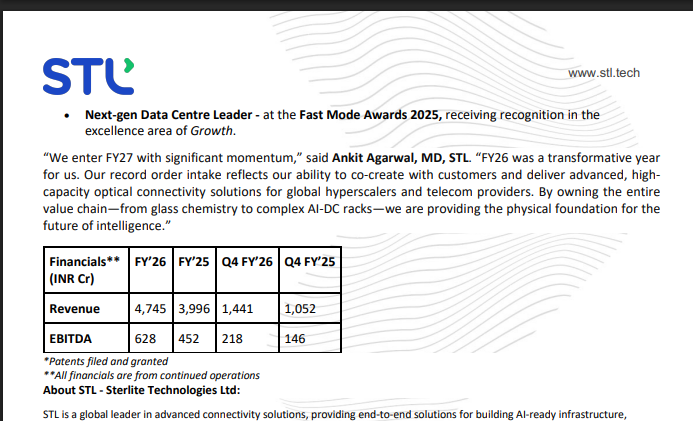

Sterlite Technologies Ltd Q4FY26 Results:- #Q4Results #Q4FY26 #Stockmarket #Nifty #sterlite Revenue 1441 Cr vs 1052 Cr (+36.98% YoY┃+14.64% QoQ) EBITDA 218 Cr vs 146 Cr (+49.32% YoY┃+68.99% QoQ) EBITDA Margin 15.1% vs 13.9% YoY & 10.3% QoQ EBIT 141 Cr vs 67 Cr (+110.45% YoY┃+182.00% QoQ) PBT +109 Cr vs +2 Cr YoY & -21 Cr QoQ (+5350% YoY) PAT +59 Cr vs +5 Cr YoY & -17 Cr QoQ