Jithin George

89 posts

Jithin George retweetledi

Boond boond se ghada Bharta hai …

162 might look small today but the smartest 50 year old capital allocator in slowly ramping up the number .

6.5K today ~ But I am living in 10K soon state🎯

Still a Steal deal 🌸

#FMF39

English

@JithinG16197054 Now own the Playground thanks to the MARCH Sale . Ok ?

English

At ₹100 Cr., the market thought it was a toy. 👀

I thought it could own the playground 🛝

English

Someone reached out after seeing this tweet saying : “your tweets are making 15% moves in the stock”😅

I am a NO ONE ,and cannot do that even without naming the company .

I do have MAXIMUM allocation here & it’s a bet on INDIA 🇮🇳 😅

#FMF20

Ron || Mad About Stocks@MadAboutStocks_

Global market for this category: $30–35 Billion 🌍 India’s share: <2% And today… a new product quietly enters the arena 🚀 But here’s the real story 👇 India’s TAM is set to move from ~150 Mn → ~300 Mn over the next 2 decades That’s not growth… that’s a demand reset I’m playing the long game here 😊 (Not everyone has the patience for this kind of compounding… and that’s okay) Added more yesterday… Had no clue the launch was coming 🫶🏻 Trivia: The current market cap of this company is just ~25% of the entire category size in India 🇮🇳 Sometimes the market whispers early… You just have to lean in 🍀 #FMF20

English

@JithinG16197054 Jithin, we have asked the relevant team to look into this and reach out to you. Please allow us some time to quickly check this internally, and we will share an update with you at the earliest.

Pratyush

PW88060

English

Never buy policy from @policybazaar

Their claim assistance is a nightmare

English

@policybazaar Surveyor has replied that he needs to talk with the repairer.but we have already forwarded the mail which I received from the workshop.

English

@JithinG16197054 Hi Jithin, I understand the delay it has caused. However, to look into your concern and expedite the process. We request you to share your registered contact number via DM.

Pratyush

PW88060 twitter.com/messages/compo…

English

@MadAboutStocks_ Got it this time.... both 39 and 40 starts with S...

English

Tranche 5 ✅

#FMF40

Have a sense it has hit bottom 🔆 Can be completely wrong .

English

@policybazaar Now I am directly contacing insurance company office on daily basis....never buy online policy...it sucks

English

@JithinG16197054 Hi, I want to know what exactly went wrong with your experience. Please share your concern and registered details via DM. I will look into it and pass it along to the appropriate team.

Pratyush

PW88060

twitter.com/messages/compo…

English

WIN one of two VIP @ManUtd experiences, including an exclusive player welcome!

🎟️ VIP tickets for you and a friend for Man Utd v Aston Villa

🤝 An exclusive player welcome

To enter:

✅ Follow @Snapdragon_UK

🗣️ Tell us your favourite Man Utd player!

English

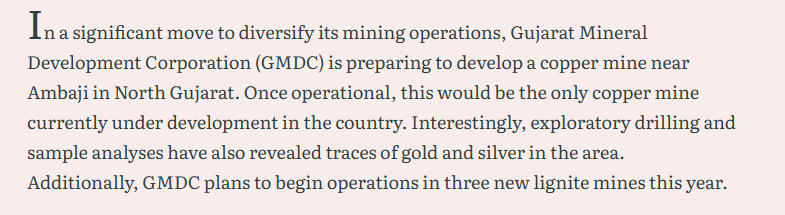

@alphainvestor_n But may take more than 10 years to extract copper from a new mine

English

Timepass talk on Sunday

1. Time to Be a Small-Cap SIP Investor

Small-cap investors are completely squeezed. SMEs are facing a liquidity choke, and metals have suddenly grown Red Bull wings. Yet the age-old truth remains unchanged: small caps create disproportionate wealth when bought at reasonable valuations and held patiently until the tide turns.

That patience, however, demands a strong stomach, one that allows us to see a sea of red in the portfolio. If that isn’t your temperament, the safer route is simple: opt for small-cap funds. Any decently managed small-cap fund tends to deliver 70%+ returns within a year once the cycle turns.

Even ICICI Prudential Small Cap Fund, which had shut the doors to fresh inflows for nearly two years, is now saying, “Mutual Funds Sahi Hai."

So, if you’ve stayed invested through the pain, don’t quit now. Just ensure your stocks are falling because of market conditions, not because earnings visibility has collapsed.

The antithesis is equally important: Holding companies with no earnings visibility is dangerous, such names can permanently destroy capital, even take it to zero.

Conviction matters. So does discrimination.

2. Multi-baggers and the ₹100–1,000 Cr PAT Transition

Amit Jeswani (@Amit_Jeswani1) famously mentioned at an @ias_summit a few years ago that most multi-baggers are created during the journey from ₹100 Cr to ₹1,000 Cr in PAT.

A textbook example of this phenomenon today is MCX.

MCX reported a PAT of ₹149 Cr in FY23, which dropped to ₹83 Cr in FY24, largely due to the technology contract issues that played villain during that phase. Post those setbacks, the turnaround has been phenomenal: PAT jumped to ₹560 Cr in FY25, and for 9M FY26 itself, MCX has already delivered ₹801 Cr. The company is now well on track to cross ₹1,000 Cr PAT for the full year.

Unsurprisingly, the stock has delivered ~10x returns over the last three years.

Another powerful example is Laurus Labs. Laurus already delivered disproportionate returns once during the 2019–2022 cycle, when PAT surged from ₹94 Cr to ₹984 Cr. That was followed by a downcycle, but the next upcycle clearly started from FY24 onwards.

PAT in FY24 stood at ₹162 Cr, while the last four quarters have reported ₹233 Cr, ₹162 Cr, ₹194 Cr, and ₹252 Cr respectively. The stock has already turned into a multi-bagger again during this phase, and arguably, the journey is still far from over.

The real exercise, therefore, is simple but not easy: Identify companies currently in the ₹100–300 Cr PAT range and assess which among them have the management quality, scalability, balance sheet strength, and sectoral tailwinds to compound into a four-digit PAT business.

The hard truth is that nearly 80% of such companies may never get there, which is why this game is never easy. But the formula remains valid, and repeatedly proven.

3. MTF and the Recent Sell-off: A Reality Check

MTF has been the talk of the town lately, and some stocks may indeed have felt the pressure during the recent sell-offs. That said, when you actually run the numbers, the issue appears far less systemic than it has been portrayed.

Yes, the impact will vary from stock to stock, and a few names could see temporary stress. However, at the aggregate market level, the risk seems contained.

Consider this:

Out of 2,134 stocks with MTF exposure, ~83% can be fully unwound within ≤5 trading days based on average traded volumes.

The total MTF outstanding for these 83% names stands at approximately ₹91,000 Cr. The combined market capitalisation of these companies is around ₹382 lakh Cr. Put differently, MTF exposure is a small fraction of overall market value.

4. Hospitals Are Getting “Admitted” Too

In this sell-off, even hospitals, typically considered safe havens during brutal markets, haven’t been spared. Several leading names have seen meaningful corrections from recent highs:

Max Healthcare Institute: ~24%, Narayana Hrudayalaya: ~23%, Artemis Medicare Services: ~22%, HCG: ~21%, Apollo Hospitals: ~16%

Hospitals, of course, go through their own earnings cycles, largely driven by capacity additions and ramp-ups. That said, structurally, the sector remains a strong portfolio candidate for stable and consistent compounding, given predictable demand and improving operating leverage over time. Medical tourism from Bangladesh would have obviously slowed, but this should be more of a short-term blip.

At this stage, it may be worth evaluating how close these names are to their long-term median EV/EBITDA valuations. Any meaningful deviation below historical averages could start throwing up selective entry opportunities.

5. Menon Bearings

Menon Bearings delivered one of the strongest quarters in its history. Exports rose to an all-time high of ~36% of revenues, notably without any adverse impact from US tariffs. In its recent concall, management noted:

“…we have already started additional business with one of the major customers from the US… we hardly see any impact from the tariffs imposed by the USA. On the contrary, our exports are poised to grow further going ahead...”

For a company of this size, this is an interesting and positive development, especially in a challenging global environment.

That said, management also acknowledged that elevated copper prices are a margin headwind. While the company claims a pass-through mechanism, the timing and completeness of quarterly/monthly pass-throughs remain an open variable and need close monitoring.

From a cautionary standpoint, it’s worth recalling that in 2023 the company had articulated an ambition to double revenues by FY26. At the current run rate, the company appears far from that target, and it no longer seems to be a stated objective in the latest investor deck.

Nevertheless, a company executing well amid headwinds deserves a closer look.

6. Zydus Lifesciences - Zycubo (US$50 mn Peak Sales Opportunity)

Zycubo, a brand under Sentynl Therapeutics (a subsidiary of Zydus Lifesciences), has recently received approval from the U.S. Food and Drug Administration for the treatment of Menkes disease.

Menkes disease is an ultra-rare, life-threatening genetic disorder, diagnosed in newborns, with an estimated ~56 new cases annually in the US. If left untreated, median survival is less than 18 months.

Zycubo is the first and only FDA-approved therapy for this condition and has demonstrated meaningful survival benefits. In pivotal studies, when treatment was initiated early, within 10 days of birth, median survival extended to ~177 months, representing a step-change in clinical outcomes.

From a commercial standpoint, @SystematixGrp estimates price realisation at ~US$600,000 per patient per year. While affordability raises legitimate ethical and policy questions, Zycubo offers real hope to families with access through insurance or alternative funding.

7. Mackenna's Gold

Krishnadevaraya was the greatest ruler of the Vijayanagara Empire, presiding over an era of exceptional prosperity where gold, trade, and culture thrived at a civilisational peak. Legend has it that during his reign, gold and diamonds were so abundant that they were traded like grain.

That legacy seems to have quietly endured. Even today, Indian households are estimated to collectively hold ~34,600 tonnes of gold, one of the largest private gold stockpiles in the world. At $4,700 per ounce, this hoard is worth approximately $5.2 trillion.

For perspective, India’s GDP is about $3.7–4.0 trillion, while the total equity market capitalisation stands near $5.0–5.2 trillion.

Some civilisational habits don’t fade, they compound. The Jewellery companies and gold lenders are certainly trying to take advantage of it!

8. Defence Goes Global

On Jan 18, 2026, Rajnath Singh flagged off the first export consignment of guided Pinaka rockets from Solar Defence and Aerospace’s Nagpur facility. This marks the first export of the guided variant, following completion of unguided Pinaka deliveries by late 2024.

Armenia had earlier signed a ₹2,000 crore (US$250 mn) contract in 2022 for four Pinaka batteries, making it the first overseas customer for the Defence Research and Development Organisation (DRDO)-developed system. Pinaka offers precision strike capability up to 75 km (trialed up to 120 km).

This milestone reflects India’s defence export journey, from <₹1,000 crore a decade ago to ~₹24,000 crore today.

Globally, defence spending hit US$2.7 trillion in 2024, with 100+ countries increasing spends. With global tensions unlikely to ease soon, defence remains a structural, multi-year theme.

India, the world’s 5th-largest military spender with the 2nd-largest standing army, is uniquely positioned to benefit from this trend, both domestically and via exports.

From a market lens, the Motilal Oswal Nifty India Defence ETF (MODFENCE) is ~20% off recent highs and near a key support zone. Direction from here is uncertain, but with the Budget approaching, the theme is worth tracking closely.

9. Chemicals: Bottoming Out?

I came across a chart from Nuvama Research suggesting that both RoE and RoCE are likely at the bottom of the cycle after a sharp correction from FY22 peaks.

RoE declined from ~20.5% in FY22 to ~8.1% in FY25 and RoCE fell from ~23.2% to ~11.6% over the same period.

This compression reflects the severity of the chemical downcycle, weak demand, inventory destocking, and elevated costs.

At current levels (RoE ~8%, RoCE ~12%), return ratios are near the lower end of historical ranges. More importantly, the trend now points to stabilisation with marginal improvement, rather than further deterioration (of we course, we can never say never).

While a return to peak profitability will take time, the data suggests that most of the downside to returns has already played out, shifting the narrative toward gradual recovery and operating leverage.

Within this space, a few names I am actively tracking include:

📌Aether Industries – transitioning from a heavy capex phase to monetisation.

📌Acutaas – moving into a faster-growth CDMO phase.

📌Balaji Amines – positioning FY27 as a recovery year.

Each has a distinct playbook, and these are not a BUY or SELL recommendations.

10. DIIs & Retail Running Out of Gas?

Aggregate cash holdings of equity mutual funds have declined from ~7% in April 2025 to ~5.5% by December 2025, the lowest level since H1 2024.

Large-cap funds: ~6% → ~3.9%

Small-cap funds: ~9% → <6%

In simple terms, most funds are already fully invested. That limits incremental buying power from DIIs unless fresh inflows come in. Adding to the pressure, FPIs have already sold ~₹33,000 crore YTD.

With mutual fund cash buffers thin, market upside now depends more on new money and earnings, while corrections may feel sharper in the absence of dry powder.

The open question though: Can the Budget pull a rabbit out of the hat, via tweaks to LTCG, STCG, or STT, to revive FII participation? Or is that asking too much?

That’s all for today’s version. Happy Sunday!

English

Hey @grok, in the next 48 hours, help us spot the 5 comments that truly deserve the #iQOO15. #BeTheGOAT

T&Cs: bit.ly/3XQYvaG

English