Sabitlenmiş Tweet

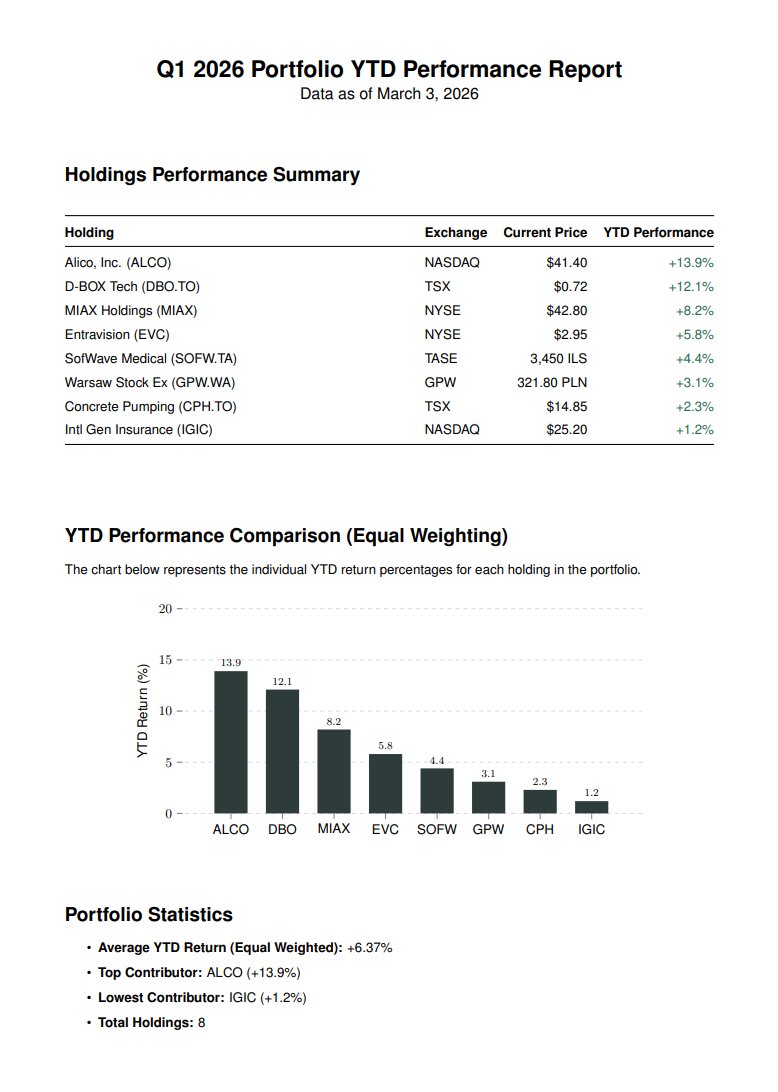

A snapchot of the performance of my portfolio for Q1 2026, generated by ai (in merely 5 seconds).

$ALCO $DBO.TO $MIAX $EVC $SOFW.TA $GPW.WA $CPH.TO $IGIC. Due to specific weighting and closing some winners that missed my hurdle rate due to share price appreciation, I managed to achieve 16.40% YTD so far.

English