Mark Boon

661 posts

Mark Boon

@markcboon

$ASPI $DGXX $SIVE $NUAI $TMC $IREN $BGDE

Netherlands Katılım Nisan 2023

246 Takip Edilen196 Takipçiler

Not everyday a company CEO publishes a thesis on why be a shareholder. Worth a read for $IREN holders although in my mind, when this starts happening, it’s never good.

Daniel Roberts@danroberts0101

A thread on where AI infrastructure is heading - and where IREN fits. 🧵

English

@kkz8gs6cyh @SunvMikey Your conclusion may be correct, but the reasoning is flawed. Shipping the silane gas in cylinders / batches of certain quantities around mid-year could mean they have inventory of finished product in the interim.

English

@SunvMikey @markcboon Its says right in the report that they are planning commercial shipments of si-28 for mid-year 2026. They pushed it back again - this is for something else

English

@samelifeenjoyer This is one of the best dig ups I have read on X. Thank you!

$NUAI

English

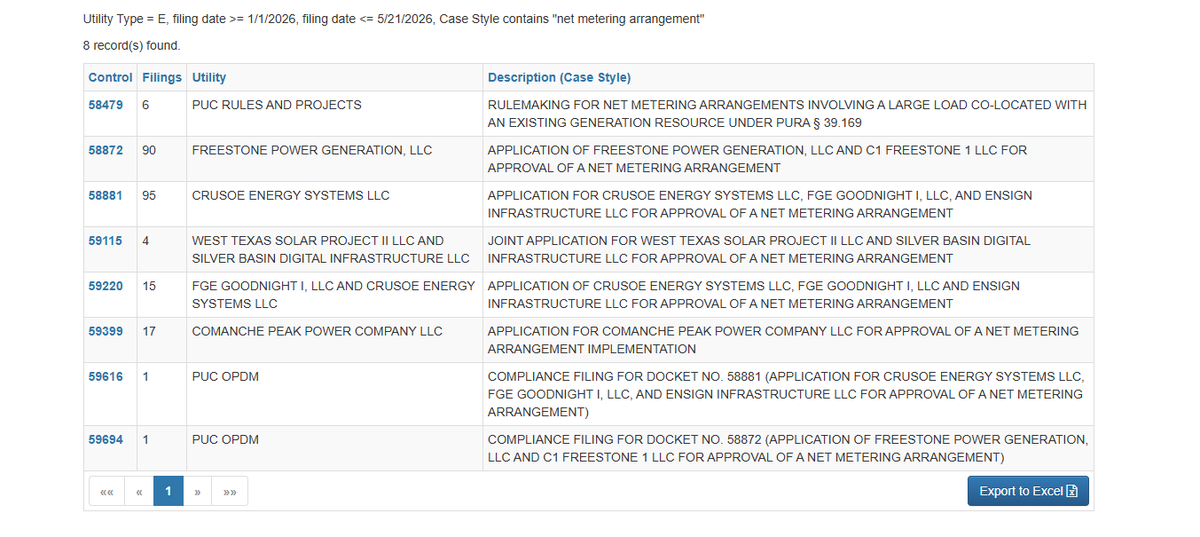

Following up on my $NUAI BTM colocation post. Did some digging into the PUCT docket and the regulatory picture just got significantly clearer.

The final rules for net metering arrangements under PURA § 39.169 were adopted last month. The framework $NUAI would use is now fully in place. Turns out my post was not speculation but is concrete which is good news for all of us.

Vistra filed comments in PUCT docket 58479, the exact rulemaking governing BTM colocation between existing generators and new large loads arguing specifically for a faster legacy track with a strict 180 day approval timeline. Companies don't spend legal resources on proceedings that don't affect their active business plans.

There's already a live Texas precedent. CyrusOne filed a BTM colocation application with Calpine for a 760 MW data center in Freestone County under the exact same framework. Fossil gas generator plus large data center load. Same structure $NUAI would use.

This is directly relevant to $NUAI's TCDC project. Calpine operates Quail Run directly adjacent to TCDC on the investor map. Vistra operates Odessa Ector Power Partners also directly adjacent. $NUAI has two active BTM colocation counterparties sitting on their fence line and at least one of them just proved the model works in Texas.

The 54 acre corridor connects TCDC directly to them. Yes, $NUAI would need a tie-in-station on their 54 acres of land. I do not want to oversimplify these engineering milestones but between Charlie, Will, HS selected engineering partner - Ramboll, and Stream I would suspect they are ahead of the curve on this.

One more thing worth addressing directly since I know someone will bring it up. No, Vistra/TCDC net metering application has been filed at PUCT yet. Just because there is not a public filing does not mean it is not in the works. Again, reminding us Charlie hinted at "one big signing day".

Here's why I am not currently concerned:

I pulled every active § 39.169 net metering application currently on file in Texas. There are five of them, see attached photo which highlights these documents. Every single one lists both the generator AND the large load customer as joint applicants. Freestone Power Generation filed with C1 Freestone 1 LLC. Crusoe filed with Ensign Infrastructure. The generator and the confirmed load file together. The Vistra Comanche Peak docket 59399 detail proves Vistra specifically knows how to file these applications and has done it already.

$NUAI hasn't announced a hyperscaler lease yet. That's the known missing piece, not the power solution. You don't file a net metering application without a confirmed load customer because ERCOT studies the specific load characteristics of the facility being co-located. Filing before the lease would be premature and put the cart before the horse.

If you would like to search around the PUCT site. See the link below. Maybe you will find something I did not! I found this to be directly relevant for all invested or looking to invest in $NUAI and figured a post here would be appropriate.

interchange.puc.texas.gov

English

@SunvMikey Yes, entirely possible. Perhaps even more likely.

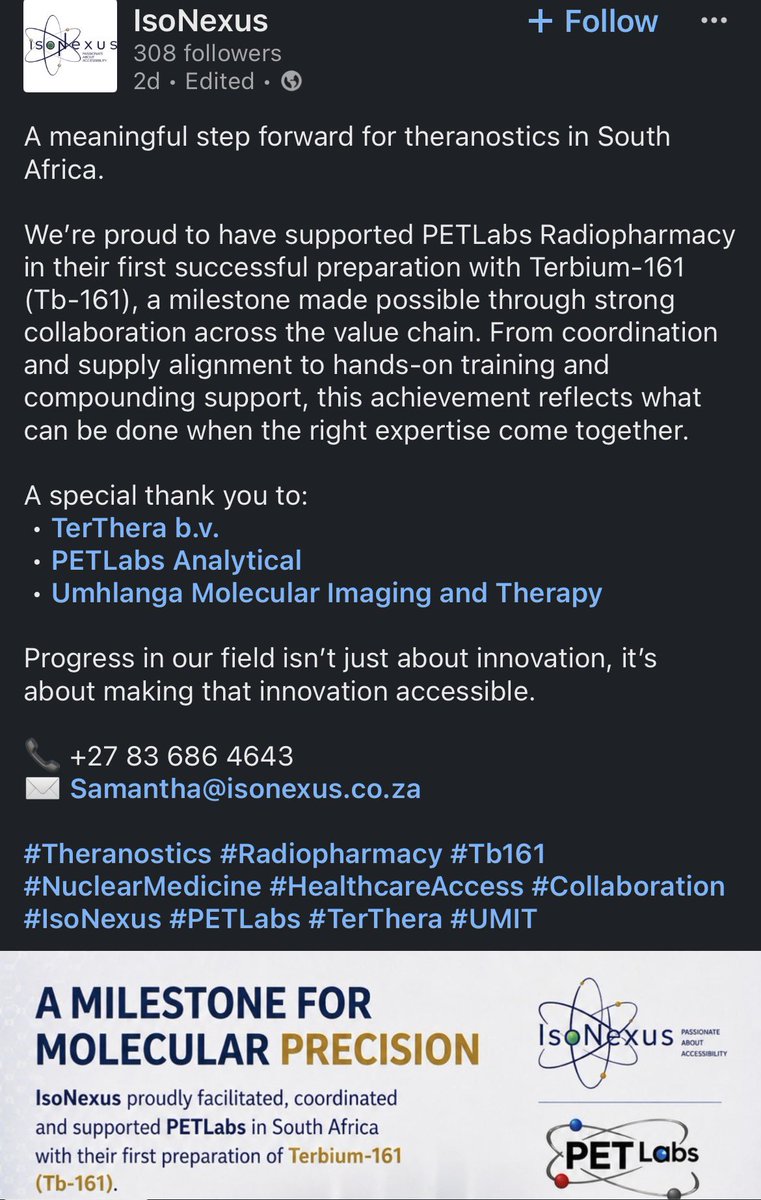

But $ASPI isn't communicating anything at the moment IMHO, like the recent successful production trials of Tb161 from Gd160.

Dan Cahill, CPA on X: "This is the first I’ve heard about it. Breaking news! "

English

@markcboon You sure it's not helium / lng from renergen? Feel like Paul would of held a conference for finally producing silicon

English

@Jaro_rogue How does $ASPI fit in your 5 year look ahead these days?

English

@SteelWoolSponge @Civic108 @litigious_dulce Same vibe here. But look at their partners who already have gotten over it. Just gotta follow the trail.

English

@Civic108 @litigious_dulce I think its just his way of speaking, which I need to get over

English

$NUAI: The Last Asymmetric Bet in the Data Center Trade

Look across the small-cap data center cohort right now. NUAI is the only remaining sub-$500M name with a real, exclusive, late-stage hyperscaler negotiation in motion. And after parsing the Q1 2026 call, conviction goes up, not down.

The Lease Math Now Works Backwards From 2027

Charlie Nelson laid out the schedule cleanly:

"Our schedule is largely driven by power availability. The power that we have available in phases 1 and 2 is in second half of 2027. Everything that we're doing is kind of back-solving from those dates... We still feel good about second half of 2027 in-service date for the first phases of this."

Working backwards from ~August 2027 with Stream's compressed 12-14 month build cycle, the lease has to be signed by July or August 2026 to preserve schedule. The construction calendar is a hard forcing function — every party at the table knows it, including the hyperscaler.

The Documents Are Closer Than Anyone Realizes

When asked about sequencing, Charlie was specific:

"The JV docs are well underway, multiple turns already with the lawyers, and the lease as well, as well as the PPA. All of these are progressing concurrently... And this is how it goes with most of these types of industrial developments — concurrent execution, especially when they're all kind of lining up around the same time, just makes sense. And you just kind of have a signing day, if you will. A very fun day, by the way, for any industrial development."

"Multiple turns" means the documents are mature. What's left should be legal documentation — a slower, more deterministic process than commercial negotiation. The phrase "signing day" is not casual. It's deal-maker code for a coordinated execution event where multiple interdependent documents close together.

The Hyperscaler Engineered This Deal

This is the part nobody is talking about enough. The hyperscaler wasn't recruited. They initially came to NUAI wanting to buy the land. Ted Warner walked through the sequence:

"We were also getting offers to buy this from actual hyperscalers... One of those we did, we signed an exclusivity agreement because we kept turning them down on selling, and we wanted to work with them on how can we partner with you to own something here. Essentially, it was, 'You've got to work with a really reputable developer.' We went and tried to find one, that exact same party sort of led us to a different party. Now here we are with that party, Stream."

The hyperscaler directed NUAI to Stream. They didn't just suggest a developer — they pre-approved their own counterparty. Stream walked in with existing commercial agreements and pre-approved designs with this specific hyperscaler. Charlie confirmed it:

"Having pre-approved designs with this particular hyperscaler, which is why we were guided into the relationship with them, frankly — to the fact that they house long lead time equipment that goes towards these projects, and it's a rinse and repeat design."

A hyperscaler that takes the time to direct partner selection, share technical specs, sign exclusivity, and cooperate through a developer restart is not a hyperscaler that walks away at the finish line. That's a counterparty that has been quietly engineering the conditions for this deal to close on terms they already endorsed.

And It's the Same Hyperscaler

Ted's clarification on the Sharon AI confusion was the most underrated moment of the call:

"The same party, that hyperscaler is still the person that we hope will be our tenant, that our designs are specifically for... [Stream has] been incredible to work with, just every day checking boxes. It's been awesome to watch them work."

No one walked. The hyperscaler that wanted this site in 2025 still wants the site in 2026. The designs are still tailored to their specs. The exclusivity is still in place.

The Balance Sheet Is Built For This

Ted's segment removed the financing overhang that haunted this name for months. $80M+ cash on hand. $290M Macquarie credit facility. The Sharon AI note is gone. Liens lifted. They illustrated the math:

"Our cash needs for phase one would be roughly $180 million before the credit that we'd get for the land contribution... That theoretical $180 million investment is more than covered for phase 1."

NUAI's expected equity check for Phase 1 is fully funded. No more "how do they pay for this" question hanging over the stock.

The Setup

The market just sold the stock 11% on a quarter that confirmed every workstream is on track

The lawsuit resolution should come soon

PPA likely ready first

JV DA close behind — Stream is the most motivated party in the deal

Hyperscaler lease execution window: late June through Early August 2026

One signing day, three documents, complete rerate

This is the playbook setup for an asymmetric trade. The downside is bounded by the cleaner balance sheet, the Stream-driven execution model, and the standing hyperscaler engagement. The upside is a name with a sub-$500M market cap signing a lease comparable to deals that already moved peers multiples higher.

"As a shareholder, I sit here with you, and I wish I could announce who the prospective tenant is, and I can't wait to announce it one day. We've been working very, very hard to get there." — Will Gray, closing remarks

NUAI is the last shoe left to drop.

investing.com/news/transcrip…

English

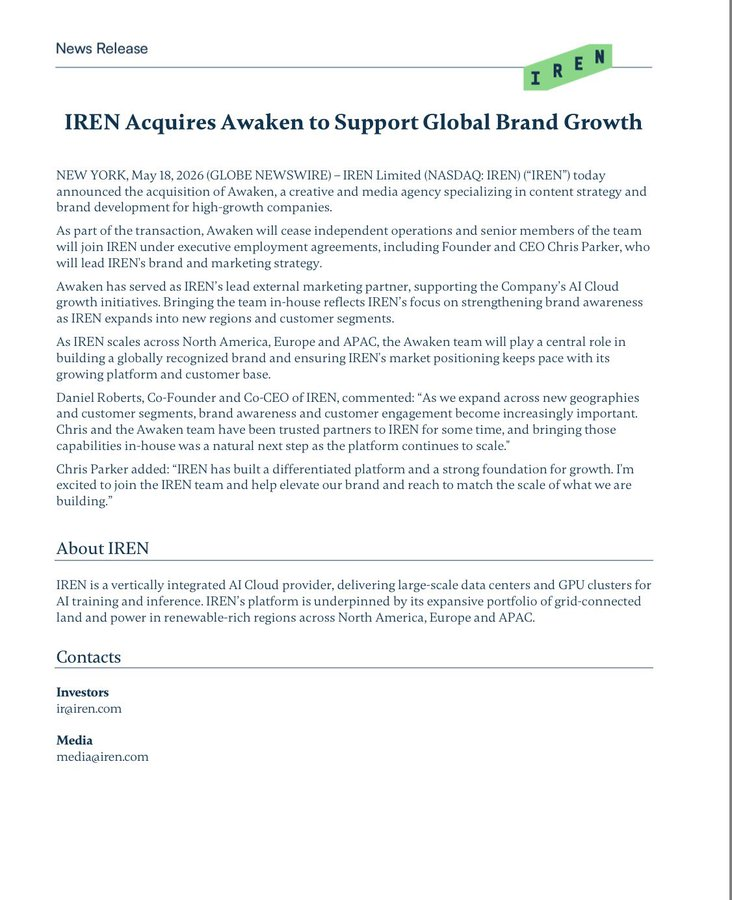

@TheBigBerbowski stating the obvious guess that they feel that the brand recognition by smaller mid-tier co's with compute needs is too low, and that the higher margins on those clients will pay for the acquisition and diversifies their client portfolio for the better.

English

Tbh, I was a long term supporter of $IREN and even today while I'm not invested I'd still like them to succeed. However, this move is weird IMO.

Why waste money on this?

Why do you need to focus on brand in the midst of your building phase?

How is this helping capex in any way?

Help me understand how is this beneficial for the company and its finances?

English

@PepInvestStocks Not high conviction yet, but my top three long-term (5 - 15 yrs) holdings are:

1. $ASPI

2. mix of $IREN, $DGXX, $NUAI, $BGDE, $VIVO a.o.

3. $TMC

(4. $BTC)

English

My Top 3 stocks that I will hold with high conviction for a very long time 🔥

$SIVE

$PENG

$LPK

These are true long-term holdings for me – I am very confident about them.

What are your Top 3 stocks that you will hold with high conviction for a long time?

English

YouTube

English

@Mindwalletbody Looking forward, thanks! I'll try to stay awake in the meantime.

English

@markcboon $aspi

This is what they sent me when I reached out for comment just now regarding SI – 28 sales

GIF

English

@aleabitoreddit Cool to see $ASPI in the list. Currently trading at only half of its ATH six months ago, but a re-rate might be "imminent", as the CEO repeats, upon first commercial shipment of Si-28 this quarter to what's rumoured to be $INTC.

English

Woah, this list compiled by you all….

Actually cooked so hard.

Many are up 2-6 times already.

Serenity@aleabitoreddit

Serenity's Followers Favorite Stock Parabolic Growth ETF: The most anticipated ETF of all time: $TRT - $5.88 $HGRAF - $4.49 $SIVE - 9.9 SEK $QURE - $17.21 $AEHR - $45.08 $ENVX - $5.07 $ASPI - $4.2 $EONR - $11.79 $LPK.DE - 6.59 EUR $MITK - $13.9 $EQR.AX - .315 AUD $WATT - $15.8 $VLN - $1.16 $BZAI - $1.79 $TMC - $4.59 $ALCJ - $74.57 $POET - $6.11 $AAOI - $108.86 $ADUR - $10.37 $P4O.DE - 6.85 EUR $PLAB - $40.87 $FLY - $33.16 $LASR - $60.7 $AL2SI - 28.70 EUR $ENAFF - $1.71 $VPG - $44.7 $EOS.AX - $9.00 I haven't heard of 1/3rd of these names, but if my followers have high conviction that their name will 10x... So do I.

English

@Mindwalletbody Has it been in the public domain before that $ASPI successfully produced its first batch of Terbium-161 (Tb-161) through PETLabs?

To me this is a first. Great find!

English

@Thebullwhisper Yes, though a little different from the "ASPI stands for as soon as possible" and the "imminent" communications by the company themselves.

English

Wondering whether $ASPI could ever become a trusted supplier (Si-28?) for mitigating thermal issues like this.

Sean@sean_________

Aletheia's Warren Lau's $NVDA channel checks suggesting Rubin delays on heat-spreader redesign:

English

@stocks4545 @litigious_dulce Same here, together with $BGDE in the more medium term.

English

@litigious_dulce I have my own Data Center ETF in my portfolio 😜- basically been/am bullish on many in sector no brainer for me!!

That being said $DGXX and $NUAI are two of my "dark horses" - $DGXX hit yesterday - NFA but I truly believe $NUAI time will come!

English

I learned a lot the past 6 months. Despite an objectively successful "career" investing, the market humbled me in a thousand ways. It is no secret that I have a large position in $NUAI, and my thesis for buying it was actually very accurate, notwithstanding the timeline (I was too optimistic in that respect). See substack.com/home/post/p-19… for a good overview by @ThePrudentWhale.

Per Tyler Page, the CEO of $CIFR, “behind the meter gas powered sites may be the highest upside convexity in our portfolio," and NUAI specializes in behind the meter gas. Interestingly, CIFR's Odessa site is approximately 30 miles from TCDC, and CIFR confirms that “We do have a lot of interest in Odessa. We have a hyperscaler interest in that site. I think I’ve mentioned before, we would be interested in potentially evolving that site much like we did Black Pearl from a Bitcoin mining site to an HPC campus.”

NUAI's Macquarie credit facility (which can be used at least in part to finance TCDC buildout, thereby reducing dilution) validates the legitimacy of the hyperscaler interested in TCDC, and Stream as execution partner significantly derisks construction. Further, the preexisting relationship between the hyperscaler and Stream truncates the normal leasing timeline, e.g., by 50% or more. Now, obviously nothing is definitive yet, but the upside is clearly there: from every angle, the NUAI thesis checks out.

However, despite being right about so much, I was also wrong about so much--not NUAI specifically, but the market generally. I obviously had not anticipated Trump causing just a global shitstorm, even if such shitstorm was necessary (likely debatable). I further failed to recognize how risk-averse institutions have become regarding AI plays, strongly preferring companies that have deals in hand to the point of neglecting companies with deals in the making, no matter how good these potential deals are. At the end of the day, institutional investors just place mature business and pre-revenue startups in different categories, regardless of how promising the latter might be.

My delayed recognition of the above resulted in me missing many things. For the longest time, I did not appreciate CIFR, $WULF, $HUT, and $APLD, instead only really praising and investing in $IREN for its more ambitious (and risky) strategic vision. Now, in hindsight, it's clear that a diversified bet on the entire data center sector (only including the serious contenders) would have done exceptionally well. This is a lesson I will remember going forward.

I know NUAI's time will come. It may not be obvious on the surface, but behind the scenes every tailwind is converging to support NUAI's approach. Besides the growing popularity of behind-the-meter power, NUAI's partnership model is extremely powerful. See the following white paper and article by Stream's CEO are quite informative on this topic: streamdatacenters.com/wp-content/upl… and streamdatacenters.com/articles/what-…. A careful reading will reveal that NUAI's perspective is significantly aligned with Stream's, although I don't know if that's coincidence or design.

That said, I know my timing for NUAI was too early, something I could have hedged by diversifying more meaningfully in the data center sector. Many peers are announcing deals literally this week, whereas NUAI's timeline is more like 1-3 months (of course, no one knows for certain). Given that I already made my bed and have no desire to chase, there's not much I can do except wait for capital to rotate from the higher valuation players to NUAI.

At the end of the day, maxims like "don't put all your eggs in one basket" and "patience is a virtue" are maxims for a reason. They stand the test of time, particularly in volatile times like today. But, when NUAI signs a deal for TCDC with a hyperscaler and it rerates accordingly (fair value of about $11 based on phase 1 alone), I don't think I will regret my decisions very much. I'm still young, and it's good to learn lessons sooner rather than later. The tuition I paid in opportunity cost was required for me to grow.

English