Julie Guo🌳🌿🍁

1.4K posts

Julie Guo🌳🌿🍁

@JulieGuo19

AI-powered data visualization and diagnostics for better supply chain KPIs

Los Angeles, CA Katılım Temmuz 2020

150 Takip Edilen115 Takipçiler

@XH_Lee23 As much as I love China, I want to be somewhere with no one around

English

Chongqing is hugely popular on the first day of the Labor Day holiday.

China's total cross-regional population mobility is expected to hit 344.1 million on the first day.

This is roughly the entire population of the US relocated in just one day.

English

another incredible day of being an ai bottleneck investor

English

@ZaStocks Thank you! I'm heavily concentrated and that's how i grow the size of my account but it also hurts to see missing other opportunities, it's all tradeoffs

English

What makes this market so fun is there are new themes and leaders emerging what feels like daily.

Rare earths, neoclouds, space, energy, the list goes on.

This is a textbook hot market.

When there’s so many stocks and groups setting up or going higher at once you feel like you can’t even keep track.

The key is to not worry about missing a trade or idea, in a hot market like this you’re not going to catch everything. All you need to do is eat a piece of the pie, not the entire pie.

English

@aleabitoreddit lol, are you on the $20/month price tier? I have the same experience, they probably don't have enough compute to allocate?

English

Both Anthropic's Opus 4.6 and 4.7 are probably the dumbest LLMs I've interacted with recently?

Did they get hit in the head by a rock. Or just retrained off $IREN investor conversations?

Probably not going to use it again for awhile.

Felt like God-Mode when 4.6 first came out and just the stupidest LLM I've interacted with recently.

English

@BlackPantherCap Needham just raised new PT to $190, by the end of the 2027, this has potential to reach 40B market cap when the capacity fully catches on

English

Last March, $AAOI was a $10 stock.

Today it's sitting above $144 on the back of something most retail investors still haven't connected.

Applied Optoelectronics doesn't make chips. It doesn't make GPUs. It makes the LASER transceivers that let AI data centers actually talk to each other at scale.

800G and 1.6T speeds. Without them, the data center buildout is a building full of expensive hardware that can't communicate.

That's a bottleneck. And the market is just now pricing it.

On April 17, the company announced it's expanding its Houston-area manufacturing footprint to 900,000 square feet. Two adjacent buildings in Pearland, Texas. 388,000 new square feet of capacity.

The target production rate: 700,000 transceivers per month.

Let that number sit for a moment.

The CEO's quote: "The demand for optical connectivity in data centers has exceeded our expectations."

This is a company that guided $1 billion in revenue for full-year 2026. It has already landed a $200M+ volume order for 1.6T transceivers and a $124M backlog of 800G orders from a single hyperscale customer.

They're not expanding to speculate on future orders. They're expanding to fill contracts already signed.

The risk is real: high customer concentration, still unprofitable, stock is ahead of its analyst consensus of $90.

Execution on this capacity ramp has to be >flawless<

But Q1 earnings drop May 7. Guidance of $150M-$165M revenue. If they hit it, this story has a long way to run.

I'm long $AAOI and have been since before this move. The photonics bottleneck was always going to play out. It's playing out in real time.

-BP

Not financial advice. Do your own due diligence.

English

@yianisz Vineland site won't be operational until Nov (that is without any delays), the new 1GW+ site in Missouri won't be done until late 2027, so majority of the AI compute is co-lo right now which means margin shrink. They will not recognize significant revenue in 2026

English

Here is why I am so bullish on $NBIS right now..

Goldman going from: $68 > $160 > $205 after $META isn’t bullish… it’s them admitting they completely misread the duration. They’re catching up, not leading.

Meanwhile credit guys price NBIS at 1.25% vs $CRWV ~10%. That’s the cleanest signal in the entire sector. Equity debates stories Vs credit prices risk.

And this 60/40 model? Customers fund most of the capex and NBIS keeps the upside. That’s borderline unfair.

I’m also watching hiring.. youdon’t keep hiring like crazy if infra isn’t ready. You slow hiring when execution phase starts.

This quarter is going to be big.

English

@jawwwn_ Peter Thiel looks terrible in the video, what happened to him, he looks like mummy

English

Peter Thiel: The US has a lot of problems but we're not declining as fast as the rest of the world.

"Demographically people in the US are not having enough children—but we are beating China. China will disappear before the US disappears."

"We have too much debt. We have not enough growth in the US economy—but the technological future is being built in the US with computers, internet, and AI."

"Maybe it's not enough. Maybe these things are dangerous. But the US is beating not just Russia and Iran—but countries like France. France is not even on AI."

"It seems that the US is winning against the whole world."

Via @gekkan_bunshun

Jawwwn@jawwwn_

Palantir CEO Alex Karp and Jensen Huang: AI = American Intelligence 🇺🇸 “AI makes America the dominant country in the world.” “I spent half my life in Europe—they’re whining and crying. We have the right chips, software, engineers, culture…” “It’s combining into a juggernaut.”

English

LFG @damnang2 your substack article on $RMBS was great and worth the subscription fee alone(as well as the recent ones on CPO/Photonics), but definitely understates the potential of MRDIMM and overall product business for Rambus that did ~$350m last year- I know you wanted to focus more on IP but the product biz is a major growth driver and high margin busines that deserves extra recognition- I think now is a good time to inform people why the $650m mrdimm TAM Rambus management gave in december 2024 is likely to be revised MUCH higher.

Here's a list of just a few growth drivers that are NOT fully priced into RMBS share price yet.(some mrdimm, some rdimm-none priced in)

1. $AMD huge deals with $META and OpenAI(all will use Venice CPU and next gen, all mrdimm capable)

2. Intel $INTC x86 CPUs in $NVDA Rubin NVL8 system

3. X86 Socket sighting with rdimms in NVDA LPX(groq) systems-these will be 20% of total Rubin output accoding to Jensen! Huge volume product-this is not confirmed but all signs point to it being accurate(ai image recognition and @Patrick1Kennedy whos opinion I trust-he said those are x86 sockets)

4. $ARM new CPUs, they are saying $15b in annual revenue at maturity, for perspective, $INTC did $53b in revenue in 2025, this is a huge new market opening up and these ARM CPUs also are clearly using RDIMMs and DDR5

5. Cerebras deals with OpenAI $AMZN and many more to come. Cerebras systems all have x86 cpu attached.

6. Todays news about $GOOG and $INTC working together

None of this is being spoken about by any of the analysts covering $RMBS. I do not see a situation that $RMBS doesnt

$MU $SNDK $WDC $STX $MRVL $CRDO $AAOI $LITE $COHR $VIAV $AEHR $VICR $TSM

Damnang2@damnang2

Let’s get in before everyone catches on🚀🚀🚀

English

@Kross_Roads I found it funny they say their capacity exceeds demand but they couldn't realize those backlog/bookings

English

$AEHR The earnings were VERY good for Aehr Test Systems in their Q3, with several strong signals and a couple areas of weakness. Let's take a look.

🔴BEARISH

There were two softer spots. This quarter's revenue (a miss, around ~$10m), and (related) the clock issue miscommunication (which is resolved).

However, I said going into this call that this quarter wasn't about revenue or EPS. Those become more important in the second half of our 2026.

🟢 BULLISH

In the call, there are a TON of highlights. Four things stand out to me.

1⃣ NEAR-TERM REVENUE RAMP

You might say, "What revenue ramp?" You won't be saying that in the future, however. Aehr reaffirmed guidance of the high side of their $25-$30m through the end of May.

Gayn also confirmed they'd come on the high side of bookings (the $60-$80m figure) by the end of this next quarter, translating to a nice ramp for the 2nd half of 2026 (their first half of fiscal year '27).

So we get a 2x in revenue next quarter, and another 2x from there in the following.

Q3'26 - $10m (just reported)

Q4'26 - $20m (next quarter)

Q1'27 - $30-50m

Q2'27 - $30-50m

2⃣ BOOKINGS

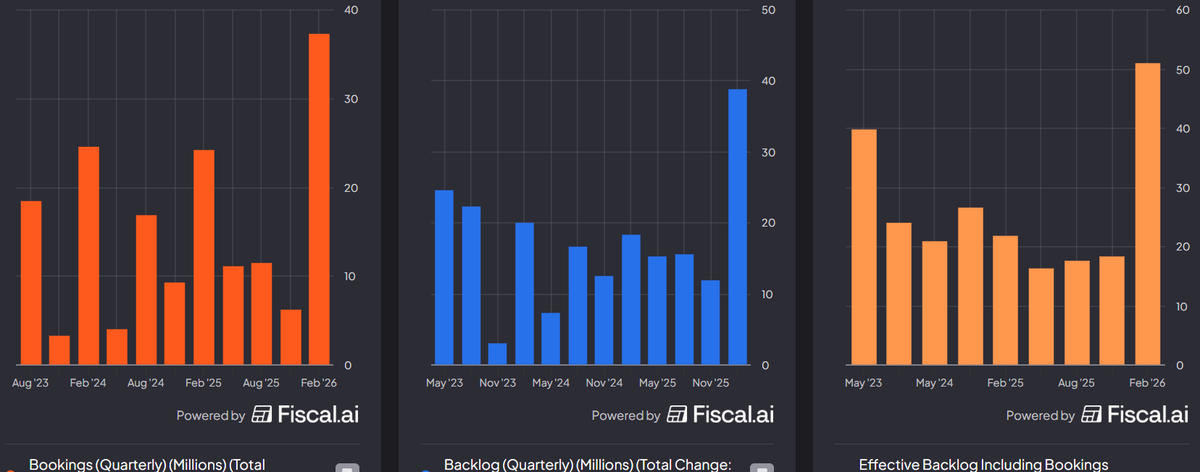

Last quarter, there was nothing exciting in the #'s. Literally nothing. Gayn said backlog (which was a paltry $6m) would increase to $60-$80m partly on the basis of the large Hyperscaler who uses their Sonoma units.

We saw a follow-on order (and 3 others) that indicated strong demand. And now, with the highest ever boookings/backlog/effective backlog + bookings (which shows the acceleration since the end of the prior quarter), it's not just speculation or hype.

It's coming.

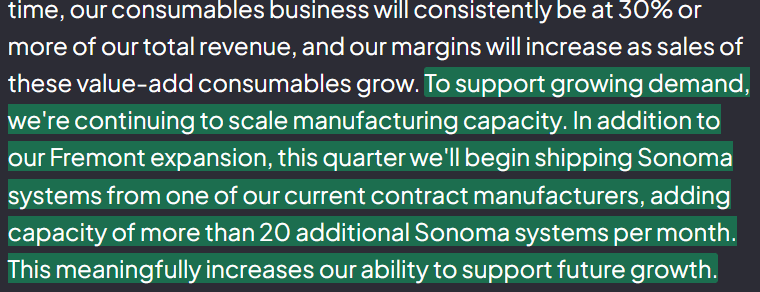

3⃣ CAPACITY

Last quarter, Gayn talked about conversations with customers who were wanting to confirm Aehr's manufacturing capacity. The reason? Outside of $TER and Advantest, most companies in the ATE space aren't good at scaling production.

Aehr is.

In fact, they acquired Incal in part due to that firm's inability to scale. Gayn indicated last quarter that Aehr could produce in their upgraded warehouse 20 units per month (blend of Fox-XP and Sonoma units). They currently produce ~1 unit per month (and even less in the last few quarters).

One would think 20 units per month would be sufficient, but apparently that's not the case. Gayn indicated Aehr has partnered with a contracting manufacturer for them to produce Sonoma units for Aehr of up to 20 per month. This is an expansion WITHOUT a CapEx requirement to 40 total units per month.

For a firm doing 1, that's a significant increase.

So why do it now? There's at least two reasons:

#1 - Overlapping orders.

Gayn talked about the lead hyperscaler who will have another follow-on order for the Sonoma units in the next few weeks and "are forecasting a substantial expansion of Sonoma systems purchases" in the 2nd half of this calendar year and continuing in '27. He thinks there's "overlapping ramps" between the current and next gen.

If that alone was the reason, it wouldn't be enough to contract out some manufacturing for the Sonoma units.

#2 - New Customers

The larger reason is the number of "lines in the water" so to speak. Those include at least two major memory manufacturers (and perhaps all of the triopoly), and at least 3 of the hyperscalers, as well as some smaller customers.

They also all but confirmed $AAIO is the newest customer who did what is usually never done last week: paid for engineering qualifications AND a unit right away, and there's more ramp comin.

They won't win every production order, but Aehr wants to ensure that future customers don't go another way simply because they're skeptical that Aehr can produce needed volumes.

Going from producing ~1 unit per month to 20, then saying that's not enough is either stupid or stupidly bullish. I'm confident in the latter, only because this detail was NOT hyped on the call. It's in the middle of the report, and Gayn mentions it casually (leading to an analyst's question).

4⃣ CONTINUED WINS

They've had a flurry of contracts and expansions this quarter, leading to those robust bookings numbers. But they also showcased some unknown new orders in addition to the silicon photonics win, and the forecasted demand is especially robust.

New customers often translate to future orders, and the recurring revenue from consumables and services is expected to be around 30%.

NEW

- "A major new silicon photonics customer."

- "A new customer in silicon carbide" focused on Asian / EV market.

- Engineering Qualification order 2 days ago from a new customer's AI processor.

FORECAST / FORECASTED

- "Multiple additional XP production systems over the next year as they ramp capacity to support next generation hyperscale data center deployments." Likely from $AAIO (Silicone Photonics).

- "A forecast for additional production systems as they ramp into next calendar year" from "our lead Silicone Photonics customer" (not $AAIO).

- "We see an uptick in activity and forecast from the silicon carbide players... Aehr is seen as the market leader."

--------

And beyond these, there's a lot of lines in the water (GaN, memory, HBM etc) that is generating significant attention.

FINAL THOUGHTS

Last quarter was speculative until it wasn't, and the follow-on orders came, leading to bookings ramping.

Revenue acceleration begins next quarter and looks like it has legs to continue for quite some time. The TAM is immense, and Aehr is extremely well-positioned to benefit from this AI arms race.

In Gayn's own words (on why they aren't doing $500m in revenue now):

"The answer is, we think that we have a very good opportunity to significantly grow our package level and wafer level business across the biggest segments that are driving burn-in. One of the reasons we're leading with putting infrastructure and capacity in place to be able to have the conversations we're having with these customers, they're throwing out some really big numbers. Somebody, they're going to warn me, you're getting carried away here, but it's an awesome place to be..."

I'll be banking some gains, but that price target of $70 I threw out when we were in the $20's? That's going to look small in a few years.

English

@ParadisLabs it's possible there will be another ATM on the way

English

Looks like the $AAOI $500M ATM is done now?

Timeline:

> By Mar 12, the first $250M was already done.

> The second $250M probably cleared during that late March period where the stock kept bouncing at the $90–$105 range.

Analysis:

> Between Mar 13 and Apr 7, total vol was >100M+ shares, with single days hitting 20M+. Selling the final ~2.5M shares into that kind of liquidity is an exit for the agents.

> Management dropped a $200M 1.6T order followed by $124M in 800G wins. These execution signals allowed Raymond James to offload the final tranche into a ripping market without tanking the price.

> Jane Street took a 5.3% stake on Mar 23. When big money steps in during a tactical secondary, the ATM is usually the source.

Pretty sure the supply overhang is gone now given the price surge over the last week.

English

@insane_analyst are you buying AAOI at this level or do you think there will be a significant pull back?

English

Trading account update.

I wana add aaoi and aehr but out of buying power.

English

@KairosPraxis hope you are right about the drop, i got shaken out a while ago and looking to re-enter

English

Sold (trimmed) most of my position in $LITE and $TSEM today. I don't usually turn things around within a month but up 60% on the former and 75% on the latter.

Optics will be a megatrend like no one is imagining, but plenty of ramps and drops along the way.

Kairos@KairosPraxis

New heuristic for selling. This past year, I sold a bunch of tailwind-riding stonks because of elevated multiples- $PNG.V, $FTG.TO, $LASR, $TTMI, $EOS.AX. Always regretted it. So new rule: Don't sell/trim a good business unless I can envision stock price falling 25% from here.

English

@aleabitoreddit you are amazing, unfortunately i got shaken out during the 2 consecutive days of downward volatility

English

Did you listen anon???

My high conviction long $AAOI is up extreme amounts.

Post from 2025 around hyperscalers:

“We’ll likely see investments pour to players like $COHR, Innolight, $LITE, and $AAOI as a theme in 2026.”

Thesis. Validation. Live.

Serenity@aleabitoreddit

$AAOI is up 24% and $LITE is 5% since my thesis today. From BOM analysis, LITE ($27B) is levered toward TPU Ironwood due to OCS but benefits from NVDA + all ASICs. AAOI ($2.5B), is levered toward MSFT MAIA ramp and Amazon Trainium. InP like HBM, will be a bottleneck for 2026 as they’re the foundational materials used for lasers in these deployments. Similar to memory bottlenecks with Micron and SK Hynix, we’ll likely see attention drawn to InP fabs, such as $AAOI, which happens to be one of the sole ones in America (COHR,Macom) But compared to $LITE that is up 362% YTD due to the success of Google’s TPU (from Meta and Anthropic purchase orders), $AAOI is only up 7% YTD. We’re largely seeing this because there’s a lack of retail or media attention on the $AMZN Trainium or $MSFT Maia deployments, which are largely expected to ramp up in 2026-2027. However they’re all likely to succeed due to each hyperscaler wanting to lower costs of inference for their own cloud platform. If we see other hyperscalers adopt OCS for optimized performance that the TPU achieved, expect $LITE to re-rate more than they have now given their monopoly in that specific segment. However, if we see $MSFT Maia ramp up (given $AAOI is likely developing a new architecture for them), and $AMZN Trainium ramp up ($4B warrant + purchase orders), expect $AAOI to rerate. Photonics and InP will be the new bottleneck like memory. We’ll likely see investments pour down stream to players like $COHR, Innolight, $LITE, and hidden levered plays on specific hyperscaler ASICs like $AAOI as a theme in 2026. The market is currently rewarding the Google TPU supply chain but might be missing other hyperscaler ASIC ramps.

English

@aleabitoreddit where is the financials posted? I couldn't find any on their website

English

$AEHR earnings:

- Current Backlog: $38.7 million as of the end of the quarter, with an "effective backlog" of $50.9 million

-H2 FY26 Guidance: Reiterated expectations for $25 million to $30 million in revenue for the second half of the year

Thoughts on earnings:

Can just ignore current earnings, main indicators are around hyperscaler volume ramp H2.

Volume ramp indication confirmations:

1. "We are seeing significant forecasts from our lead hyperscale customer for our Sonoma systems for high-volume production burn-in of their custom AI processor ASICs"

2. "We expect a significant near-term follow-on production order from this customer for a large number of systems to be shipped during Aehr's fiscal year 2027"

This is what is expected with $AEHR transitioning from qualification to mass volume like $AAOI and we got that confirmation.

H2 is probably more confirmation around siph customer volume ramp into 2027.

English

I have spent the last 8 years building a list of 200+ business ideas.

Sweaty, low risk, great businesses.

Comment "Ideas" and I'll DM you the list.

English

@marcorubio well, trump speech will not be pretty just based on this video

English

@aleabitoreddit hi guys, any insight on recent $AAOI's weakness? I mean, it didn't bounce back violently like the others in photonic space and it fades quickly too

English

$AEHR looks extremely promising at ~$1.1B MC.

Aehr is starting to remind me of an early $TER, mixed with pre-earnings $AAOI.

If we look at the timeline and speculated customers:

Feb 11th: Sonoma production win for Hyperscaler's AI ASIC processors. (likely $GOOGL, $AMZN, $META).

- Probably Google? Aehr bought Incal, who was speculated to be used by Google for their TPUs.

Feb 26th: $14 million from AI lead customer (likely $AMD, $NVDA)

- Probably $AMD here for Instinct MI300/MI400.

March 3rd: Lead silicon photonics customer for one FOX-XP system (likely $INTC siph)

- Very likely $INTC has been their lead customer.

March 31st: Initial order from major new silicon photonics customer (likely $AVGO, $MRVL, $CSCO )

- New customer (rules out Intel), prob one of these transitioning to 800G/1.6T silicon photonics transceivers

(All speculative, very confidential BOM)

Regardless. This timeline is just bottling up for $AEHR.

Could be next earnings. Or two quarters from now.

But feels like a matter of time before we see mass orders.

English

I’ll give you a hint.. this is one of those moments where everything looks crowded… but it isn’t.

AI infra isn’t slowing, it’s shifting layers. $NVDA just told you with CMX, Groq, CPO: the bottleneck is no longer compute, it’s memory + data movement + orchestration.

The market is still stuck on GPUs. The money is moving elsewhere..

KV cache becoming a category isn’t noise, it’s signal. That pulls in names like $VRT $ANET $CIEN $APH on the infra side, not just compute.

Again the “TurboQuant kills memory” take? I’m not buying it. compression lowers cost > usage explodes > total demand still rises. That still feeds $MU $WDC $STX over time.

Photonics is even cleaner. Demand is locked, supply is tight. That’s $LITE $COHR $MTSI $TSEM $AAOI $FN.

..and compute doesn’t disappear, it just gets repriced. $NVDA $AMD still win, but they’re no longer the only game.

The real rotation is happening in plain sight:

compute > memory > interconnect > orchestration.

Most portfolios are still stuck in step one.

English

@aleabitoreddit Nobody is taking a bid on $AAOI today, are you concerned?

English

$AEHR new qualification orders from a leading optical transicever company.

It’s in the early $AAOI stage where it’s getting tested by major hyperscaler supply chains for optical transceivers/silicon photonics.

Before the mass volume inflection point that may be at any time.

$AEHR up 12.73% premarket.

English