MS Rojento

2.7K posts

MS Rojento

@KRojento

You think she is funny ⚡️ Ordinals will change the world.

Japan Osaka Katılım Temmuz 2022

1.4K Takip Edilen695 Takipçiler

มีหุ้นตัวนึงที่ AI ต้องพึ่ง

ไม่ใช่คนสร้างโมเดล ไม่ใช่คนขายชิป

แต่เป็น “คนสร้างบ้าน” ให้ Data และ GPU

- รับเหมาสร้าง Data Center

- ลูกค้าคือบริษัท Tech ใหญ่ระดับโลก

- หุ้นเล็ก แต่โตเงียบๆ + ได้แรงผลักจากยุค AI แบบเต็มๆ

หุ้นโครงสร้างพื้นฐานแบบนี้อาจจะไม่โตแบบหลายๆเด้ง แต่การันตีได้ว่ามันจะโตไปพร้อมเทรนด์ AI แน่นอน

ไทย

MS Rojento retweetledi

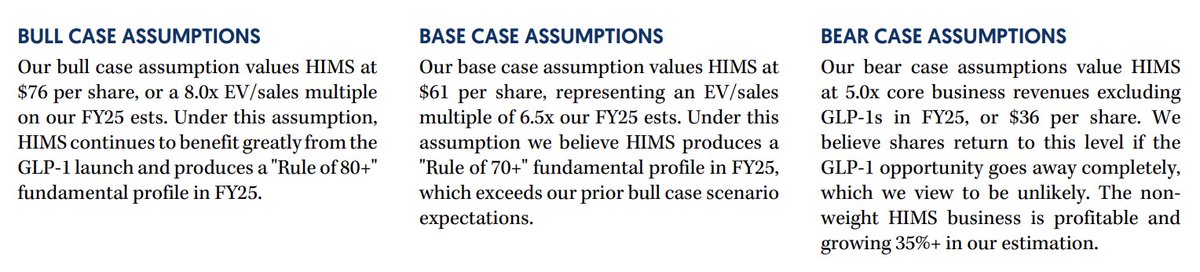

🚨 NEEDHAM $HIMS SCENARIOS

Bull: $76 PT

Base: $61 PT

Bear: $36 PT

English

MS Rojento retweetledi

WILL WE GET ANOTHER 2011 CORRECTION?

Moody’s just downgraded the U.S. credit rating… and the market dropped 1% AH. While that might sound like 2011 all over again, it’s not.

Here’s what’s different this time, using the market as a metaphor:

Think of the U.S. government like $AAPL.

Back in 2011, S&P downgraded U.S. debt from AAA to AA+. That triggered a major sell-off.

Why? Because at the time, many funds and contracts could only hold “AAA-rated” assets.

It was like a fund being forced to dump Apple after a downgrade… not because Apple changed fundamentally, but because the rules said it had to. The downgrade broke the eligibility.

After that, the system adapted.

Contracts were rewritten. The market evolved.

Instead of requiring “AAA,” funds started allowing “U.S. government securities,” regardless of the letter grade… just like if an ETF updated its rules to allow the largest and most liquid companies, not just the technically “top-rated” ones.

By 2023, when Fitch downgraded the U.S. again, there was no panic.

The market had a small pullback initially.

Because even if $AAPL isn’t rated “perfect,” it’s still Apple. Still dominant. Still trusted.

Now it’s 2025, and Moody’s $MCO is just catching up… making the AA+ rating unanimous. But the U.S. was already split-rated AA+. This didn’t downgrade it further, it just matched what was already true.

No new selling rules get triggered. No collateral issues. No forced moves.

Because the “portfolio” has already adjusted.

So here’s the takeaway:

The U.S. might not be rated AAA anymore, but it’s still “Apple.”

Still the most trusted issuer. Still the most liquid debt market in the world.

Still the asset everyone runs to when things get rough.

This isn’t 2011.

And this downgrade doesn’t change a thing.

A sell can happen… or, the melt up could continue.

You pick.

English

MS Rojento retweetledi

MY THREE BIGGEST MISTAKES SINCE TAKING MY PORTFOLIO PUBLIC IN 2023

Since taking my portfolio public in 2023, my growth portfolio has risen 293%, but I've made plenty of mistakes along the way. Going public added a new layer of scrutiny to my investing decisions. When every move is out in the open, there’s nowhere to hide from mistakes -- and I made some big ones. Not necessarily in picking bad companies, but in failing to act decisively when I saw warning signs or opportunities that, in hindsight, were obvious. Looking back, my three biggest mistakes all stem from the same problem: hesitation at critical moments -- whether failing to cut a name when I saw the writing on the wall or not pulling the trigger on a rotation I knew made sense.

At the core of it, these mistakes weren’t just about hesitation -- they were about emotional attachment. I held onto $U because I wanted to believe it would turn around under new leadership, despite seeing better opportunities elsewhere. I stuck with $JMIA longer than I should have because I was invested in the idea of an African e-commerce winner, even after management showed they couldn’t be trusted. And I dismissed $HOOD for too long because I had convinced myself fintech wasn’t my play, even as the company evolved beyond what I originally thought it was.

1. Holding Unity Too Long Instead of Rotating Into AppLovin

One of the clearest examples was Unity. Two years ago, I was vocal about the need for the CEO to be fired. The company had fundamental structural issues—not just execution missteps, but a complete misunderstanding of what made Unity valuable in the first place.

Unity's entire business was built on developers -- its success depended on empowering them, not squeezing them. But management lost sight of that, focusing on the wrong areas while neglecting the core ecosystem that made Unity a dominant force in game development. Instead of improving the core engine and tooling for developers, they prioritized aggressive monetization schemes and ad-tech expansion, betting on areas that weren’t their competitive advantage. The runtime fee fiasco was just the final straw -- it was a symptom of deeper issues that had been festering for years.

Under the hood, the problems were obvious: Unity was bloated, inefficient, and losing developer trust. The company spread itself thin with acquisitions that didn't integrate well, attempted to pivot into ad-tech instead of refining its core engine, and consistently made decisions that alienated the very people who built their ecosystem. By the time they tried to walk back their disastrous pricing decisions, the damage was done -- developers were already looking for alternatives, and Unity’s reputation had taken a massive hit.

I saw all of this happening, but I hesitated. Instead of selling when it became clear that leadership fundamentally misunderstood their own business, I held on, waiting for change. And eventually, the CEO was fired -- validating my concerns -- but by then, it was too late. The stock had already been wrecked, and the opportunity wasn’t in being right about Unity’s problems -- it was in selling early and rotating into a company that actually understood its core strengths.

That company was $APP. While Unity was losing developer trust, AppLovin was doing the opposite -- building AI-driven monetization tools that developers actually wanted. The market rewarded that execution, and Applovin has since gone up 40x. The difference was clear: one company was prioritizing the right things, while the other was actively destroying its own moat.

The mistake wasn’t just holding Unity -- it was underestimating just how much damage bad leadership and misplaced priorities could do to a company that once had a dominant position. The moment a management team forgets who their real customers are, the downfall begins. And when that happens, waiting for a turnaround is just wasted time.

2. Overlooking Robinhood as a Transformative Fintech Play

And then there’s Robinhood. If I had to pick one stock that completely changed my view on what I thought I knew, it’s this one. I ignored it for years because, fundamentally, I’m not a fintech investor. I focus on themes, on structural growth stories, on companies that build moats. And for a long time, Robinhood didn’t fit that framework for me. It was just a brokerage, dependent on transaction revenue and riding market cycles rather than controlling its own destiny. I wrote it off.

That was a mistake. Because Robinhood isn’t just a brokerage anymore -- it has transformed itself into a financial institution in the making. The numbers are staggering. Revenue soared 58% YoY to hit $2.5B in 2024-- a ridiculous growth rate for a fintech at this scale. But the real shift wasn’t just in the top-line numbers -- it was in how Robinhood makes money.

The most explosive growth came from crypto trading revenue -- which surged 100% YoY to $252M. This isn’t just about favorable market conditions -- it’s about engineering a monetization model that thrives regardless of cycles. Robinhood isn’t just reacting to crypto volatility -- it’s monetizing it with precision, extracting value at both the retail and institutional level.

Beyond crypto, the shift toward recurring revenue is where Robinhood is really cementing itself. Gold memberships are up 90% YoY, now at 3.2M users. That’s an inflection point. It means Robinhood isn’t just churning through users looking for free trades -- it’s converting them into long-term, high-LTV customers who are paying for access, liquidity, and premium features. It’s a total transformation from a transaction-driven business into a subscription-based, high-margin financial ecosystem.

And then there’s wealth management -- a segment I never saw Robinhood entering, but now, it’s making a serious move. The acquisition of TradePMR is Robinhood going after RIAs -- Registered Investment Advisors who control massive capital pools. This isn’t just a retail play anymore; Robinhood is positioning itself as a financial infrastructure provider.

And crypto? Robinhood just acquired Bitstamp, one of the oldest and most respected exchanges. That’s a move that legitimizes its role in institutional digital asset trading. While other fintechs are retreating, Robinhood is expanding into global crypto finance -- staking, institutional trading, liquidity provisioning.

I saw all of this happening, and I still didn’t pull the trigger early enough. Robinhood forced me to rethink my bias against fintech, because this company is no longer just a trading platform -- it’s embedding itself into the financial system in a way that few others can match.

3. Not Selling Jumia Immediately After Poor Corporate Governance

The moment Jumia’s management lied and abused investor trust, I should have been out. No questions asked. But instead of following the principle that once trust is broken, it doesn’t get fixed, I convinced myself to give it time. That was a mistake.

Jumia’s botched offering right after an earnings miss wasn’t just a bad decision -- it was a betrayal of shareholders. That was the moment to exit. But I didn’t. I rationalized, I looked for operational improvements, and I waited for signs of progress that, frankly, weren’t enough.

Jumia’s latest earnings confirmed everything I already knew but had refused to act on: the company is still struggling. Yes, it’s burning less cash than before. Yes, total orders have returned to growth. Yes, they’ve made some smart operational shifts. But at the end of the day, this is still a survival story, not a growth story. A capital infusion is only as good as the results it delivers, and Jumia still hasn’t proven it can turn the corner.

And there’s another major problem -- FX headwinds could be a multi-year issue. Many African markets where Jumia operates have faced significant currency depreciation, and these macroeconomic headwinds aren’t something Jumia can control. A company struggling for profitability in the best conditions isn’t going to thrive in an environment where its revenue is constantly being eroded by FX. Even if Jumia improves operationally, these currency challenges could wipe out any financial progress for years.

At the same time, Starlink is accelerating the digitization of underserved areas like Africa -- which was one of my major long-term tailwinds for owning Jumia. Greater internet penetration should theoretically drive e-commerce adoption, improving the overall market Jumia operates in. But the problem is, opportunity cost is a real thing. The African e-commerce growth story is a slow burn, and there are companies executing at a much higher level right now.

I stayed in Jumia because I wanted to believe in the long-term story, but belief doesn’t make a stock go up -- execution does. And in small-caps, execution starts with management. The moment leadership shows they can’t be trusted -- or worse, that they don’t know how to scale their own company -- the stock is a ticking time bomb.

Final Thoughts

The reality is, the market doesn’t care about your personal attachment to a stock -- it only rewards execution. The companies I hesitated on weren’t just tickers in my portfolio -- they were stories I wanted to believe in, and that attachment clouded my judgment. The best investors know when to detach from the narrative and act on reality. Moving forward, that’s my focus. Because in this game, the moment you start getting sentimental about your holdings is the moment you start leaving money on the table.

English

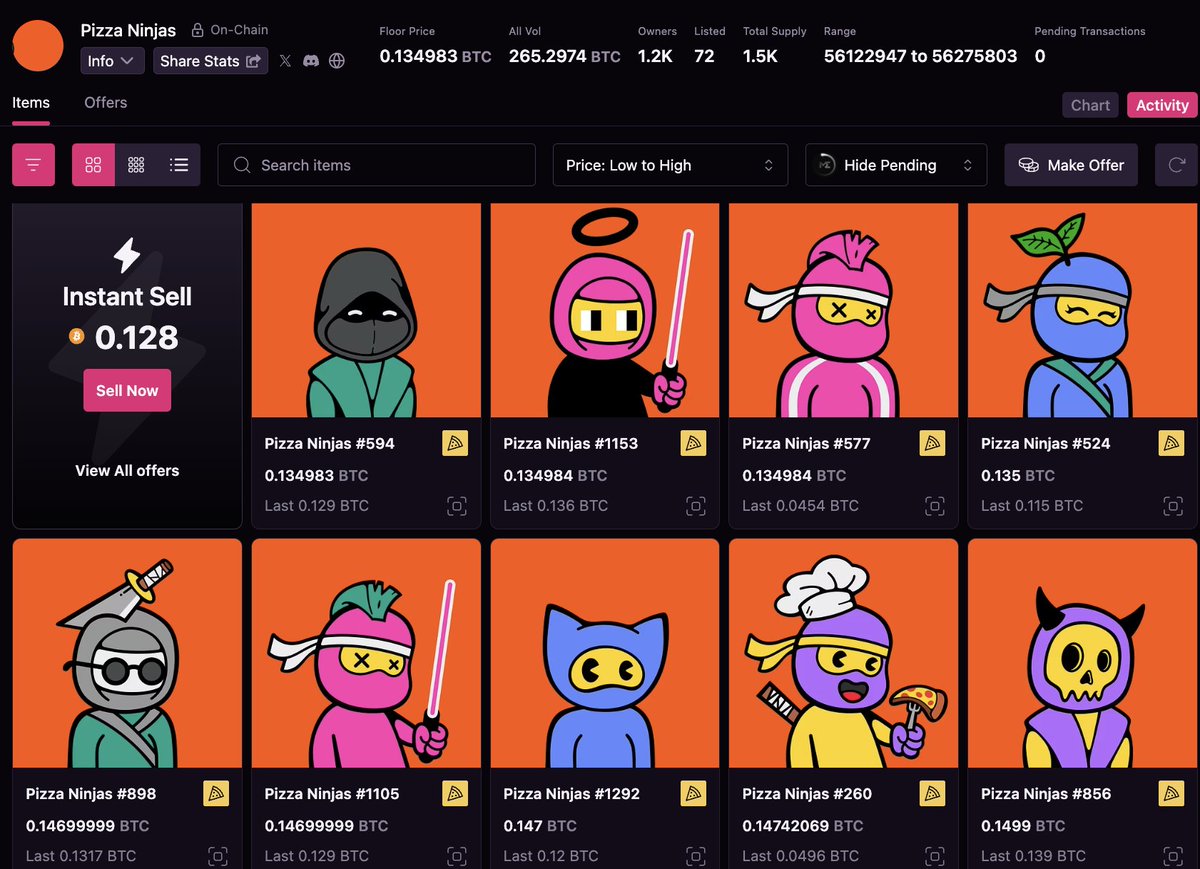

@RAF_BTC Buy back the @DogePunksBTC punks with this amount please RAF just make it alive again sir !

English

MS Rojento retweetledi

English

MS Rojento retweetledi

@mvcinvesting I hope it’s gonna be good soon, rooting for you dude. God bless you 🤞💙

English

I’m sorry for not being active here right now.

It’s been a rough time due to some family health issues, but I hope to be back at 100% as soon as possible.

Thank you for understanding.

English

MS Rojento retweetledi

Eminem becoming a grandpa? Now I really feel old. 🥺😅

Daily Loud@DailyLoud

Eminem’s daughter Hailie announces that she is now pregnant 🎉❤️

English

MS Rojento retweetledi

@KRojento Not worried, I’m pretty happy with my cost basis in each of my positions.

English