Sabitlenmiş Tweet

Portfolio 2026 May 4th week Update & Holdings:

Bought: - no changes -

Sold: - no changes -

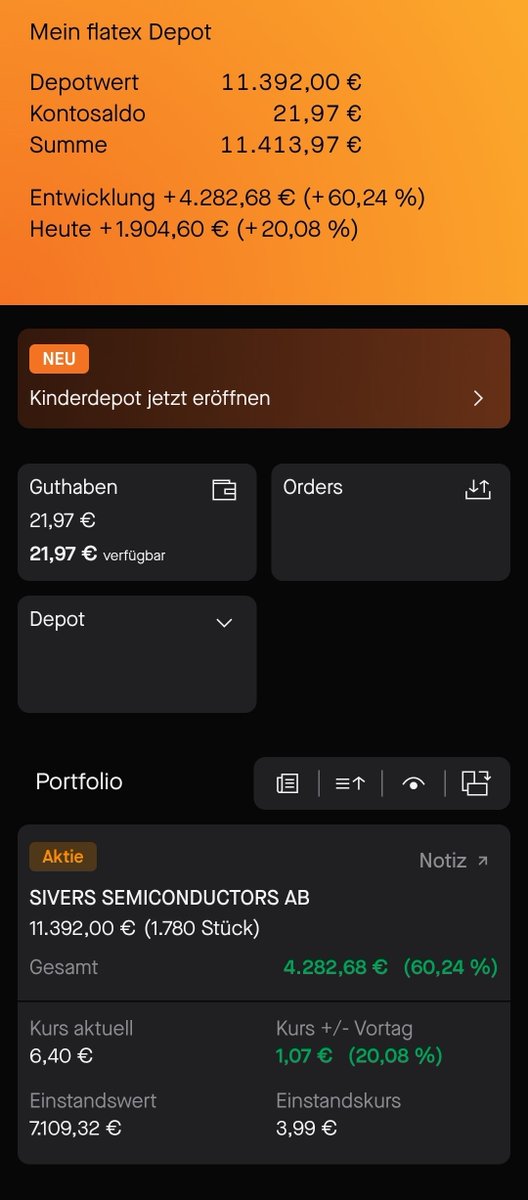

$ASTS $RKLB $SOI $SIVE $MEMS $SMOP $WYFI

$PENG $FCEL

English

LazyCompounder

1.2K posts

@LazyCompounder

I invest slowly so I can sleep well. Sharing my insights AND portfolio. Not financial advice/edu only - just my own compounding journey.

don't fade me if i go all in $SIVE next

" $SIVE can reach $80b because $LITE is $80b" has to be the dumbest and most dangerous investment thesis ever. People will lose their savings listening to all this misinformation. It's sad and needs to stop (I am starting an anti $SIVE crusade). 1. $SIVE is not a bottleneck (despite it being the poster child of the photonics bottleneck craze). A bottleneck, by definition, must be the company that constrains the production of a massive downstream industry. To constrain production, you must both own hard physical assets and hold a dominant market share position. Sivers has neither. Sivers is a fabless design company that relies on WIN for Foundry services, and with revenues of ~$30 million, they hold near zero market share in the massive datacom laser industry. 2. Supply chain analysis is misleading. In semiconductors (or any industry producing a durable manufactured good) switching costs are near zero while process power, cornered resources, and scale dominate. Therefore, "who has a superior product" is far more important than "who supplies what to whom." CPO external light sources require quality lasers meeting noise (linewidth and RIN) and power (400mW+) specs. $SIVE lasers are far inferior to that of larger peers like $LITE. 3. $SIVE valuation is comically detached from reality. On NTM metrics, $LITE trades at 14x EV/Revenue and 32x EV/EBITDA while $SIVE trades at 50x and 650x (!!) those same metrics. As a permanent AI infra bull, I fully agree that consensus is too conservative; however, they are not off by two orders of magnitude. The misinformation needs to stop. Let's help actually help retail understand what they own.

Your thread misses the actual nuances in CPO photonics supply chains and architectures. Let me dismantle your points with facts: 1. $SIVE IS a real (time-bound) chokepoint You say a bottleneck requires owning a fab + dominant share. That misses how this market actually works. WIN Semi is the foundry, but $SIVE controls the allocated capacity and holds the design wins as sole/primary source for the next 2-3 years. Ayar Labs (Supernova 1.6T+), Celestial AI, Lightmatter, Lightelligence, POET, Jabil 1.6T LRO, O-Net/Enablence, these players have locked in $SIVE for their external light source roadmaps. Remove $SIVE and their timelines slip years. This is exactly how fabless Sandisk became the bottleneck on Kioxia NAND output. CW lasers are already supply-constrained industry-wide (see $LITE earnings). $SIVE controls the merchant supply window for non-NVIDIA hyperscalers. That’s the chokepoint. 2. Switching costs are high and $SIVE lasers are not “far inferior” You’re comparing apples to oranges: $LITE’s single-emitter high-power CW lasers vs. $SIVE’s 8-channel DFB laser arrays (InP100 platform). The CPO designs from Ayar, POET, Celestial etc. need WDM aggregation: 8 x ~65 mW = ~520 mW total per fiber, not one 400 mW emitter. $SIVE’s e-beam lithography DFB gratings deliver tighter linewidth, better RIN, superior thermal performance, and array integration exactly for these architectures. They already meet stricter specs in FMCW LiDAR. Once a customer’s entire optical engine is built around $SIVE’s array (as Jabil publicly confirmed), switching means full redesign + re-qualification. That’s not “near zero”, it’s a multi-year nightmare. That’s why these players chose $SIVE over $LITE. 3. Valuation is not disconnected, you’re using the wrong metrics Quoting ~50x NTM EV/Revenue on a company still in qualification/development-contract phase is misleading. 2024-2025 = design wins and quals. The volume ramp starts 2027. Pipeline is already $453 M. $SIVE is executing the exact same playbook $LITE did: start as laser-die supplier, then move downstream into optical engines and modules via M&A. Comparing today’s multiples to $LITE’s mature business ignores the ramp timing and the massive TAM expansion in AI CPO. Your “CW lasers are dumb interchangeable” take is the real oversimplification. $SIVE has structural, architecture-specific advantages as a time-limited chokepoint with asymmetric upside.The “$80 B because $LITE is $80 B” strawman isn’t what the bull case is built on, it’s capacity lock-in + design wins + ramp timing.

To be honest I do believe $SIVE can reach 80b market cap. It's in an exploding market and its peers have done it.... So what prevents them?