Sabitlenmiş Tweet

THREE WAYS TO DO P2P

(Especially in INDIA, Without getting your bank account frozen or begging a Telegram admin)

Everyone’s trying to move USDT to INR or back, but the options are either sus, overregulated, or straight-up bank-risky.

Here’s what I’ve tried, what worked (for a while), what broke, and what might actually be heading in the right direction.

1. Traditional P2P (aka “bro, send UPI”)

➜ You send USDT to someone you know

➜ They send you INR via UPI or bank

Sounds simple. And it is, when you trust the other person.

No platform, no fees, no drama… until the drama starts.

➜ Works well with friends/mutuals

➜ Super quick

➜ No exchange middleman

But...

➜ Very limited liquidity

➜ If they ghost, it’s game over

➜ No dispute support

➜ Repeated unknown INR credits = bank’s favorite red flag

I used this after the 1% TDS rules kicked in, not hoping to dodge tax... But headaches from it (I file tax regularly 💪).

Worked… until Kotak said “nah” and locked my account.

Took mild heart attack to unfreeze it.

2. CEX P2P (Binance, WazirX, etc.)

➜ You post an offer

➜ Buyer or seller matches

➜ INR is paid manually, USDT released via escrow

This one feels safe. And for the most part, it is.

➜ Escrow protects both sides

➜ Good liquidity

➜ Ratings help avoid shady traders

But...

➜ Full KYC, your entire identity’s out there

➜ Every transaction is traceable

➜ Banks still freeze accounts

➜ 1% TDS, PAN uploads, Form 26QE… this isn’t crypto anymore, it’s clerical work

Used to be smooth back in the no-tax days. I’d withdraw straight from WazirX and sleep peacefully.

Now it’s like doing a GST filing just to sell $200 worth of coins.

3. P2P(.)me

(The new model that isn’t pretending to be Coinbase Lite)

This one’s... different. Not another exchange or app.

➜ It’s a decentralized protocol

➜ Smart contracts handle the crypto leg (USDC)

➜ Fiat leg (INR) is handled by liquidity providers (LPs) off-chain

➜ You stay anonymous but verified using ZK-KYC (zero-knowledge identity proof)

➜ LPs are rated, and reputation actually matters

You create your own smart wallet → place a trade → an LP accepts → INR/USDC flows happen

The crypto side is trustless, the INR side is peer-to-peer, but with actual filters and safety nets.

➜ You never touch INR from random wallets

➜ No one sees your PAN, Aadhaar, etc

➜ RP system rewards good actors (both LPs and users)

Let’s be real though.. it’s not some utopian fix:

➜ Liquidity still depends on LPs

➜ You need to know how smart wallets work (or at least follow instructions)

➜ It's early, not something your uncle is gonna use yet

My friend used it to pay a restaurant bill via UPI after sending USDC on Base.

No CEX, no Telegram guy, no “bro sent?” screenshots. Looked smooth, but yeah... niche for now.

Where I Stand:

➜ Started with CEX P2P — worked great before tax rules nuked it

➜ Switched to traditional P2P — got my account frozen, 0/10 experience

➜ Went back to CEXs like CoinDCX — safe but annoying

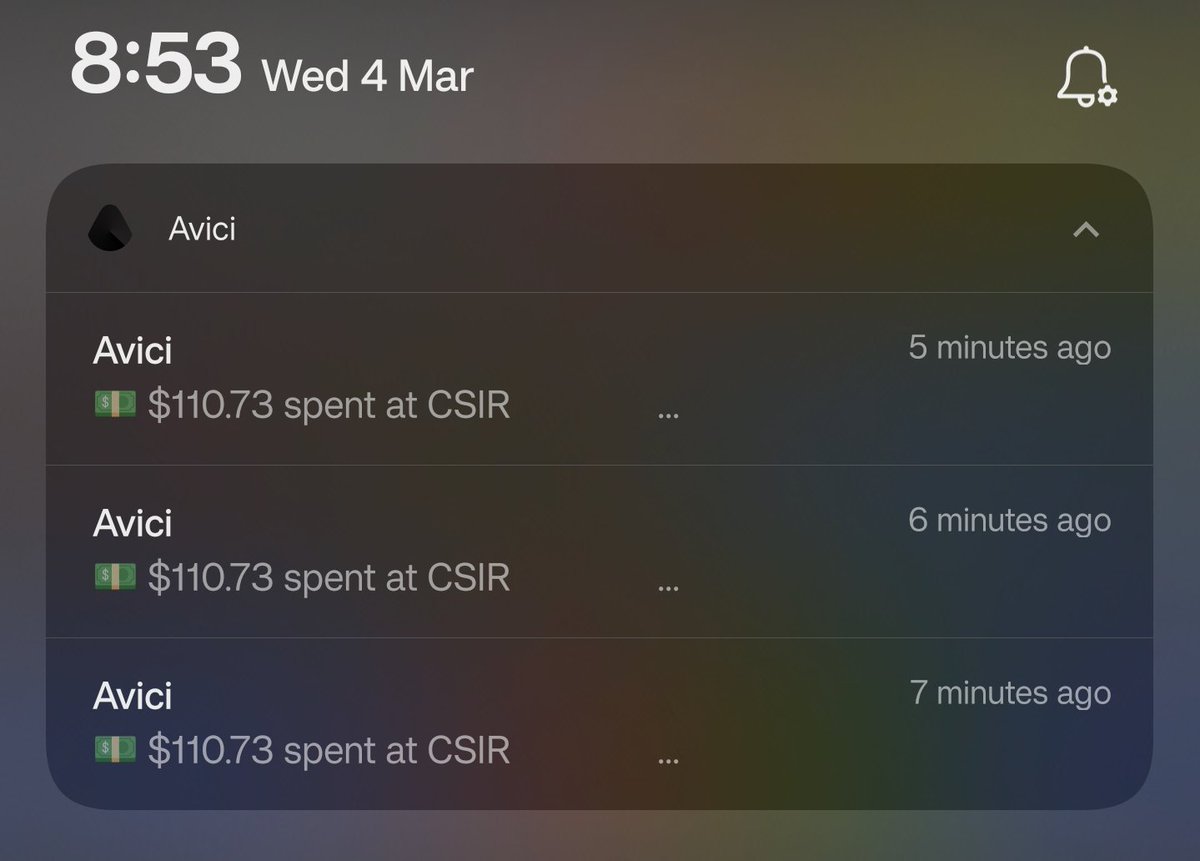

➜ Watching @P2Pdotme now — haven’t used it yet since my @AviciMoney AVICI card handles INR<>crypto for now, but keeping an eye on it

It’s not perfect. Still rough at the edges.

Most P2P flows in India either risk your bank, your data, or your sanity.

Only a few are trying to actually fix the root problem, and P2P(.)me might be one of them...

English