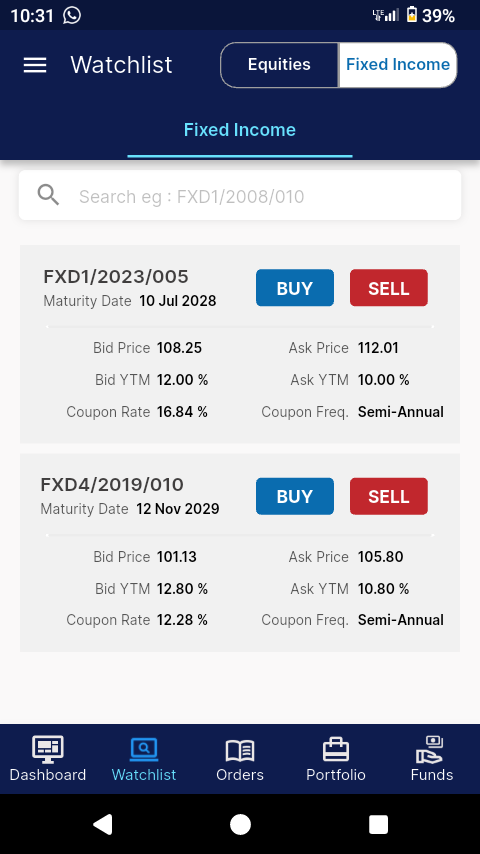

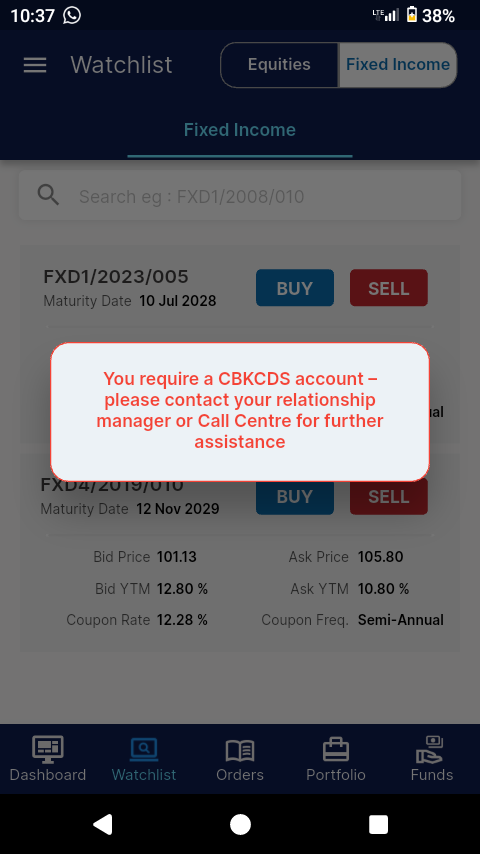

@Peter_Thuita001 This should be secondary Market. Why use AIB when you can go direct to CBK Dshow?

English

LevelQue

2.3K posts

@LevelQue

Interests In Finance & Investments

Nimelipa Ksh 500 for a two piecer pale KFC nikakumbuka I paid Ksh 700 for half a chicken, a plate of chips, a serving of ugali and greans. Tumus should open Nairobi branch.

Centum $CTUM currently @ 10.95/- "exited"🤓 my buyback range but extension means we watch PA till 31st March...

@WaruhiuFranklin $NSE Monthly for context...