@Austin_Federa @TheStalwart Tom Gallagher is a resident of Montgomery. So that makes sense

English

MATAC

55 posts

Thoma Bravo turned in the key on Medallia. $6.4B of equity wiped. It now carries $3B in debt against $200M of EBITDA. Blackstone had $1.5b of the debt across their nearly identical retail facing credit funds marked it most recently at 60.3c. It's now a zero. Credit @JulianKlymochko here. In Dec, BDCs had the following marks on their books: Apollo: 73¢ Monroe ( $MRCC): 77.57¢ Blackstone ( $XSL + $BCRED): 77.75¢ HPS: 77.99¢ FS KKR ( $FSK): 78.73¢ Onex: 79.20¢ Antares: 82.86¢ Blended BDC consensus: 77.80¢ on $1.97B of par. I had it at 55-60c. It's now equity. AND I'm generously giving it 5x EBITDA. Over 8 Billion was wiped. Poof. "And it's gone." If that is on Athene's balance sheet for 100M and rated BBB, the reserve just went from ~$1.6M to $30M. Medallia had no FCF (clearly). Still has EBITDA. ALL of this underwriting is done on adj. EBITDA coverage. There's MAYBE 200M liquidation value here. Of course, the 3B in debt was unrated by the S&P, Fitch, or Moodys. ------------------------- The following is possibly tangential but definitely relevant: 1/ $BCRED runs a separate middle-market private credit CLO series — the Delaware-only "MML" deals: BCRED CLO 2023-1, 2024-1, 2024-2, 2025-1 LLC. Those pools hold unitranche / direct lending paper. One of those is the likely home of Medallia paper BCRED has securitized. The $1.5 number I said they have exposure to may be low. Reminder, although Blackstone and chief salesman Jon Gray say that they only have 25-26% exposure to software, that's underreported. Most of business services and Healthcare IT is also software. When you include leverage that converts to 55-60%. % of NAV is the key. ^some of business services that is not software, but is still threatened by AI like accounting roll-ups. 2/ Thoma Bravo Credit ABS, is rated AAA/AA/A/BBB/BB by KBRA, 32 obligations, my audit sample includes Aprimo, Command Alkon, QAD -- all Thoma Bravo portfolio companies. The same firm originating the equity, the debt, the ABS, and the collateral management. Rated investment grade. Get ready for more.

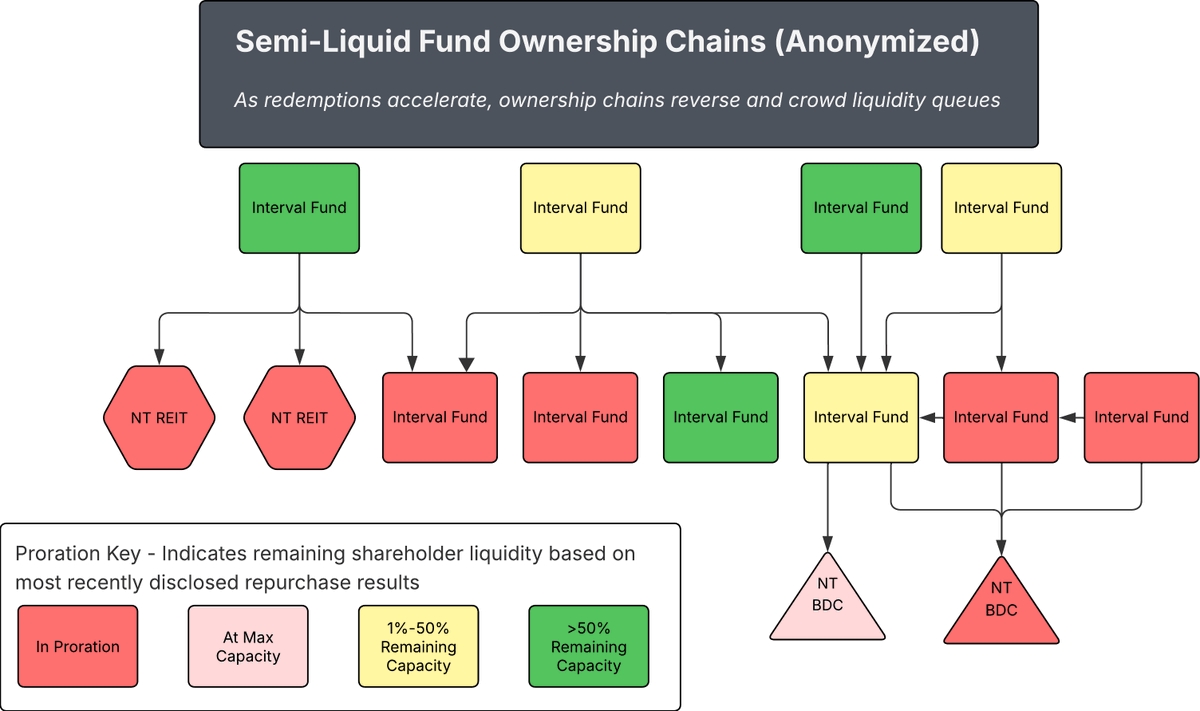

Something to consider as we head into 2026... Today’s alternative investment products represent large and heavily diversified portfolios. The risk/reward tradeoffs of that diversification are well understood. The structural liquidity implications are not. In prior cycles, NT-BDCs, REITs, and tender offer funds began prorating redemptions because individual investors tendered shares back en masse. This time, the funds will also be tendering their shares to each other. Today, we already see: • Interval funds in proration owning other interval funds in proration • Gated interval funds owning gated non-traded BDCs & REITs • Redemption requests increasing sharply in QoQ for widely held names In the retail alts market, liquidity stress cascades*. When it does, volume from these new institutional ownership chains will exacerbate the impact on shareholder liquidity. Curious how others are thinking about second-order liquidity risk in retail alts as we head into the next cycle. * pun intended #intervalfunds #nontraded

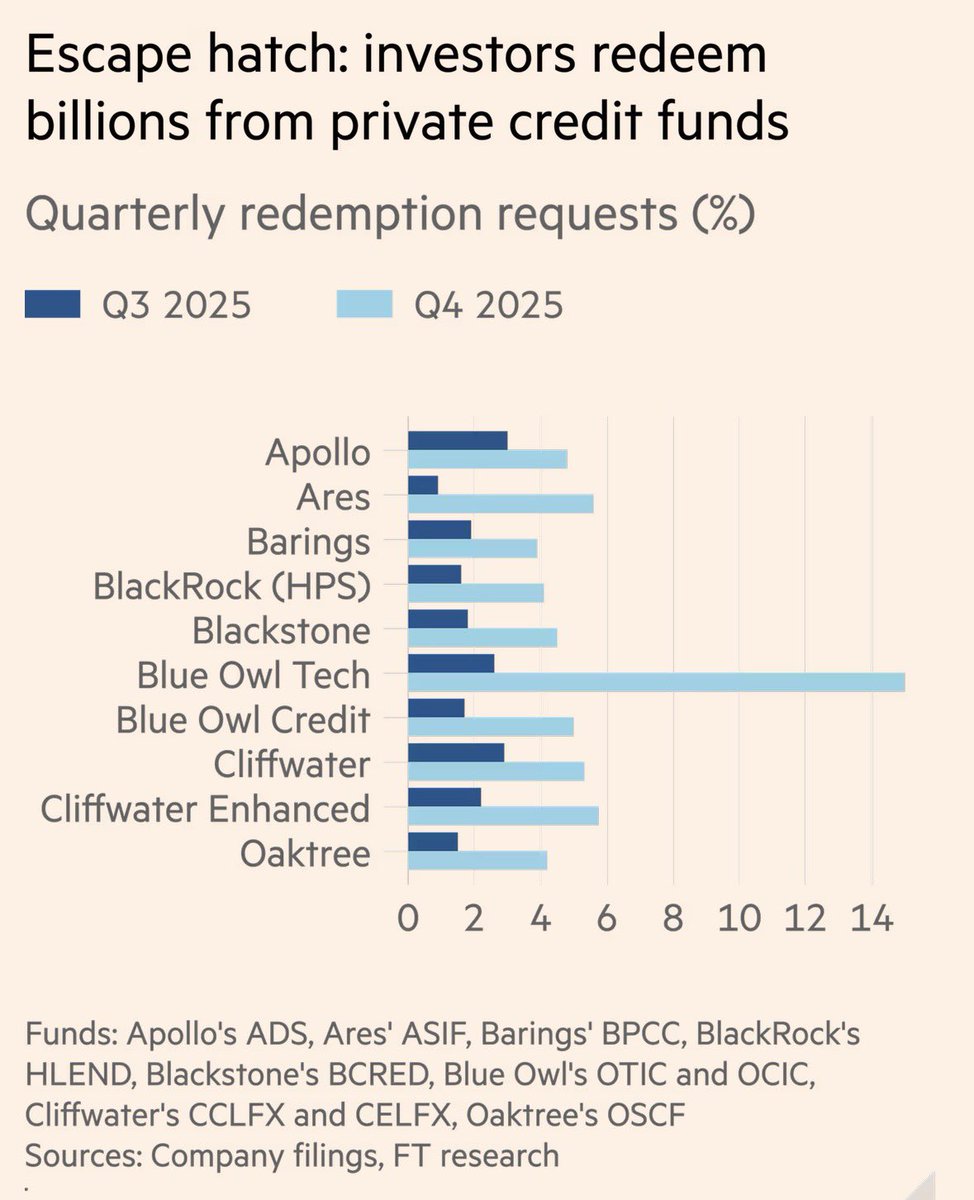

Rubric Capital, a hedge fund founded by a former Point72 manager David Rosen, wrote a private letter to their LPs effectively saying private credit is a fraudulent bubble. "Our key takeaway from this behavior is that distribution cuts are so worrisome that some bad actors are playing Enron-like accounting games" per the letter Letter called out Cliffwater, the biggest operator of interval funds and an aggressive player in selling private credit to individual investors. Cliffwater’s largest fund, started in June 2019, has since reported a total of just three negative months of investment performance. It now manages $33 billion. The first opportunity this year for investors to ask for their money back is next week. The note surmised that Cliffwater could be “a canary in a coal mine.” and the first domino of many The bubble might blow soon reuters.com/sustainability…

Boaz Weinstein Is Hunting Blue Owl’s Funds "buyout offer to shareholders at prices between 65% and 80% of net asset value" wsj.com/finance/invest…

*BLACKROCK PRIVATE DEBT FUND EXPECTS 19% NET ASSET VALUE CUT Now that’s what I call a Friday Night Dirty @Seawolfcap