@srir54 @ChintanParikh10 I am DM'ing you about the same, will be happy to help you out.

English

Manaswa Singh

184 posts

@ManaswaS

@aftermarketsin 丨 Ex-@binance 丨IIM Indore '23

If you ask ChatGPT or Claude about an Indian stock right now, the data is usually wrong or outdated. That was one of the problems I wanted to solve. I've been trading for close to a decade. Every day I'd have screens open in one tab, chatbots in another, NSE site for filings, Telegram groups for alerts, some dashboard for FII/DII data, and a spreadsheet tying it all together. At some point I just started building the thing I actually wanted. aftermarkets.in - stock research platform for Indian markets. Filing alerts hit your WhatsApp or Telegram the moment they're published, with AI summaries so you don't need to read through 40-page PDFs. Live screener with 50+ filters, earnings calendar, FII/DII flows, bulk/block deals, insider trading, & much more. It also plugs into Claude, ChatGPT, and Gemini using MCP - so your AI actually has access to real Indian market data. Everything is free right now. Have a look and let me know what you think. -> aftermarkets.in <-

Big milestone for us at Raise 🚀 We’ve raised our Series B of $120 Million led by Hornbill Capital, with participation from MUFG and BEENEXT. This investment marks the next phase in our journey to build a truly best-in-class financial services platform for India. 🇮🇳

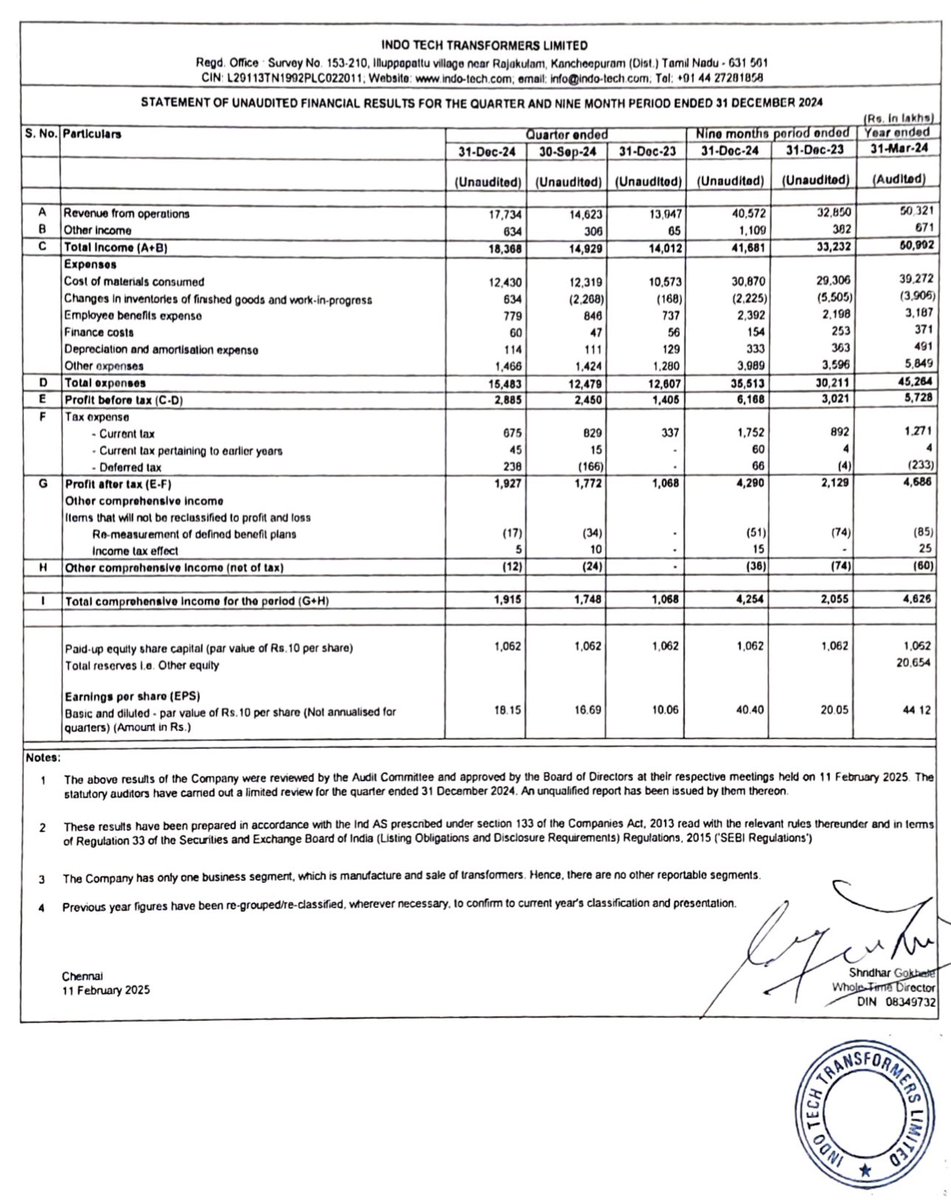

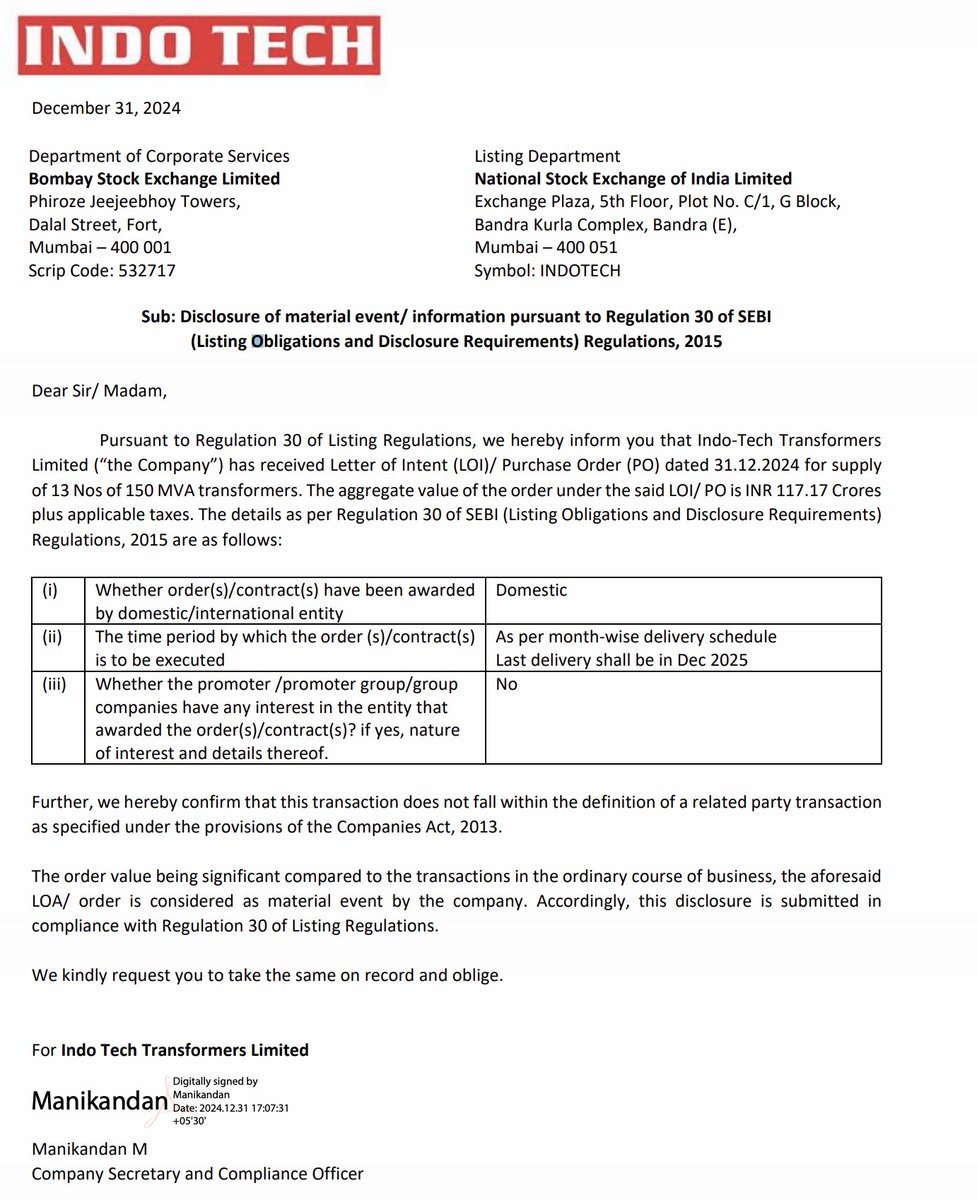

#IndoTech is my only holding at the moment and it has yielded significant returns. Relative Strength of Indo Tech Transformers has been high due to excellent quarterly results. Still available at a lower P/E than its peers. Will continue to observe depending on the market conditions.

#INDOTECH moved from 972 -->2875,200% returns so far - Came out of Range - Given good monthly closing - Potential to deliver great returns - Keep monitoring #investing #multibagger To find out this type of multibaggers early, check out my multibagger strategy. snehassr.graphy.com/courses/Multib… To findout this type of Swing Trades early, checkout my Swing Trading Strategy. snehassr.graphy.com/courses/Swing-… The strategies available on 20% discount. Grab this opportunity now