Sabitlenmiş Tweet

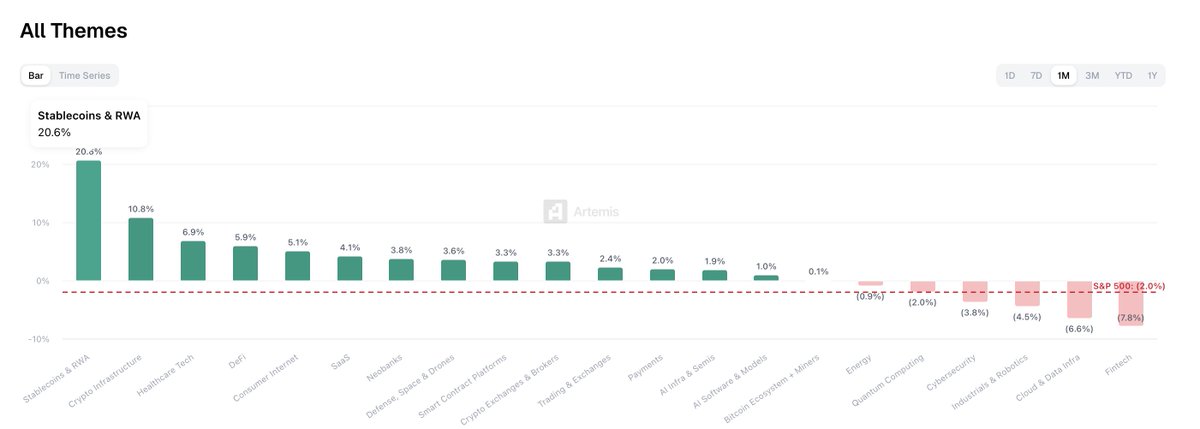

The most important crypto news of the latest days didn't come from a blockchain foundation. It came from @MorganStanley.

The launch of the MSNXX government money market fund, designed specifically to hold reserves for stablecoin issuers in compliance with the GENIUS Act, is a watershed moment.

It mirrors the post-2008 financial crisis, where money market funds became the de facto safe harbor for institutional capital.

We are watching the institutionalization of stablecoin infrastructure in real-time. This marks the beginning of the utility era. The infrastructure layer is maturing rapidly. There has never been a better time to build compliant, next-gen financial systems.

English