Sabitlenmiş Tweet

Portfolio Update – 05/10/2026👇🏻👀

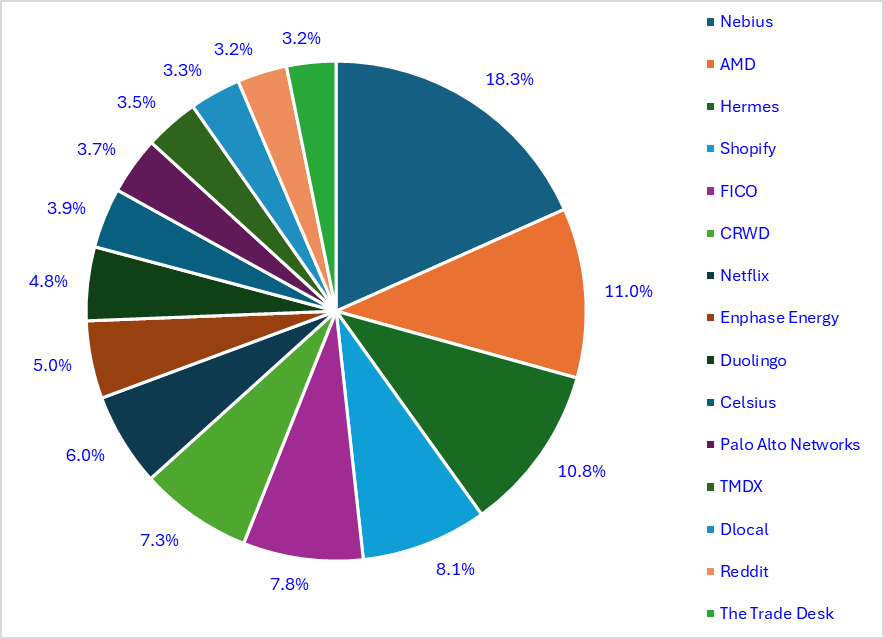

• $NBIS– 18.3% ($27.41)🧑💻// Up 472%🟢

• $AMD – 11.0% ($112.6) 💻// Up 252%🟢

• $RMS – 10.8% (€1,698.06)📺// Down 2%🔴

• $SHOP – 8.1% ($57.98)📦// Up 90%🟢

• $FICO – 7.8% ($1,021.58)📒// Up 8%🟢

• $CRWD – 7.3% ($221.27)🔏// Up 121%🟢

• $NFLX – 6.0% ($17.25)📺// Up 346%🟢

• $ENPH – 5.0% ($32.35) 🌞// Up 10%🟢

• $DUOL – 4.8% ($173.33) 🧑🎓// Down 37%🔴

• $CELH – 3.9% ($21.98)🧃// Up 29%🟢

• $PALO – 3.7% ($145.09)🔏// Up 31% 🟢

• $TMDX – 3.5% ($56.97)💟// Up 4%🟢

• $DLO – 3.3% ($10.03)💳// Up 20%🟢

• $RDDT – 3.2% ($130.10)💻// Up 20%🟢

• $TTD – 3.2% ($31.31)💻// Down 26%🔴

• YTD Performance: +1.5%🟢

• YTD Nasdaq Comp Performance: +12.9%🟢

• Market Updates:

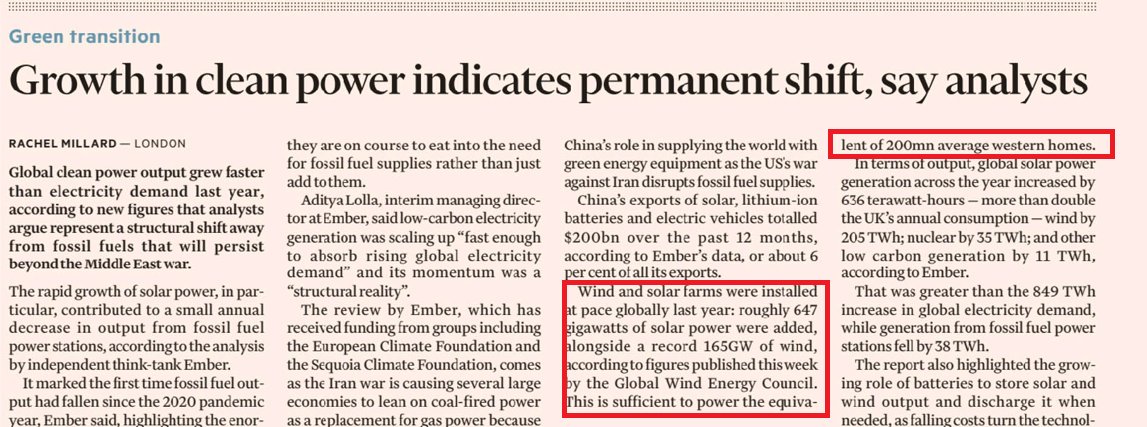

- So far in 2026, investors are rewarding Three Big structural narratives: AI Infrastructure & Compute (i), Power, Energy & Electrification (ii), and Strategic Sovereignty (iii).

- Investors increasingly believe AI is not a cycle anymore but a utility like backbone for the economy.

- Multiple research reports now frame energy as the second derivative winner of AI.

- Investors are rotating toward utilities and energy infrastructure because they benefit regardless of which AI model wins.

- Finally, Equity Markets are heavily rewarding companies tied to national security, industrial policy, and supply-chain sovereignty.

• Our view:

- In 1999–2000, investors correctly identified that internet would transform the economy.

- But they incorrectly identified which companies would capture the durable value, where margins would settle, and which parts would become commoditized.

- Today’s equity market believes AI compute is scarce, power is scarce, and Data Centers are scarce.

- But if supply catches up, returns compress, pricing power weakens, and capex becomes excessive.

- Investors may currently be extrapolating scarcity too far into the future.

- However, the largest long term value creation often migrates from infrastructure to applications, ecosystems, and business model transformation.

- The eventual Multi Trillion Dollar Winners may not even exist yet.

- Consequently, we are really cautious on these themes and are reasonably exposed.

- This cautious approach explains why we are underperforming so far in 2026.

• Recent Moves:

1. $UNH > $RMS

- We fully liquidated our stake in $UNH to initiate a position in $RMS (~10% of our portfolio).

- $UNH has partially recovered from recent lows but we think $RMS would offer much more upside potential at current level.

- Recently market sentiment has turned negative on Luxury businesses due to the conflict in the Middle East.

- However, we think $RMS is an exceptional business with high desirability of its products and strong pricing power.

- Consequently we believe current valuation multiples are attractive, considering $RMS is trading at 21.60x EV/2026E EBITDA vs 29.62x on average over the last 5 years (~38% discount).

2. Simplification: $CORT, $EFL, $RBLX > $FICO

- We simplified the portfolio by selling some positions, in which we had less conviction such as $CORT, $ELF, $RBLX, and building a new position in $FICO (~8% of our portfolio).

- We believe $FICO is well positioned in the credit scoring market (~90% market share), and the business will be able to defend its market share.

- Besides, in the future revenue might be less driven by prices considering the ongoing regulatory scrutiny but the credit scoring market is dynamic, and $FICO could continue to grow with more Scoring Volume.

• Other Opportunities:

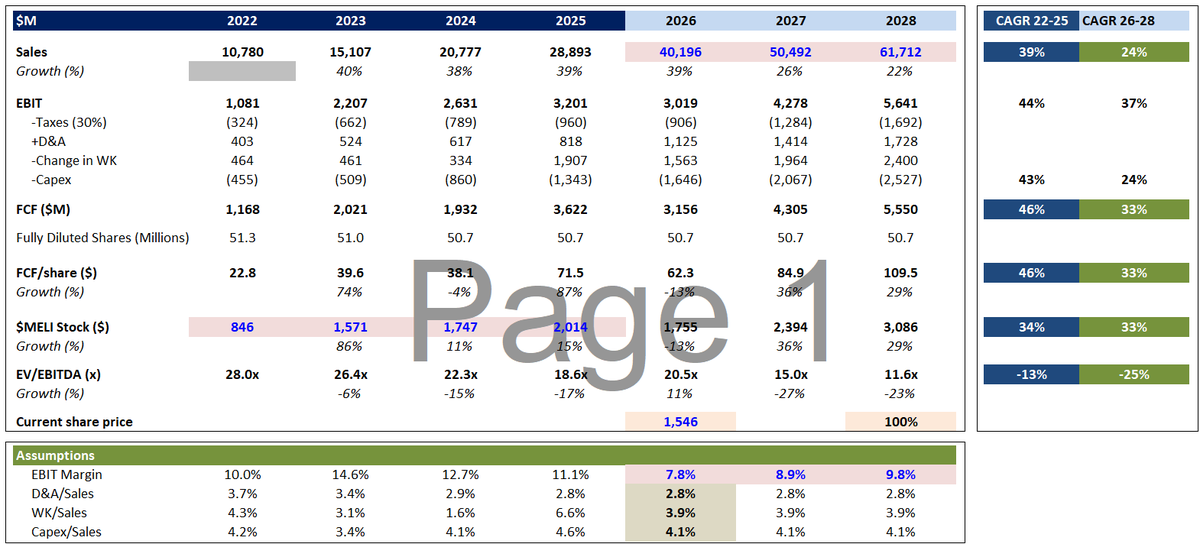

- 🇺🇾 $MELI: Over the last few years investors have seriously rerated the stock from 27.90x EV/EBITDA in 2023 to 19.73x EV/EBITDA in 2026. This is one of the reason why $MELI Stock has barely appreciated over the same period while operating and cash flow metrics have improved. Today, we believe valuation has reset enough, and the stock is attractive for long-term investors.

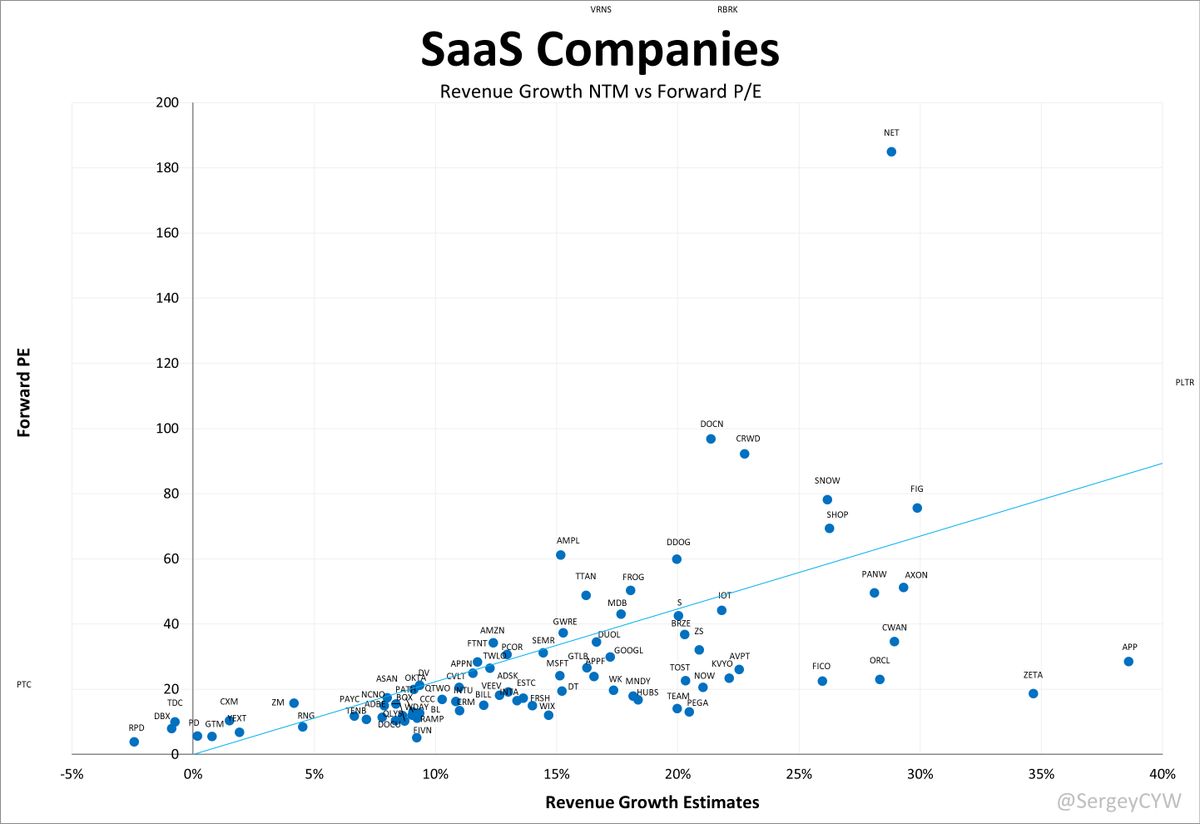

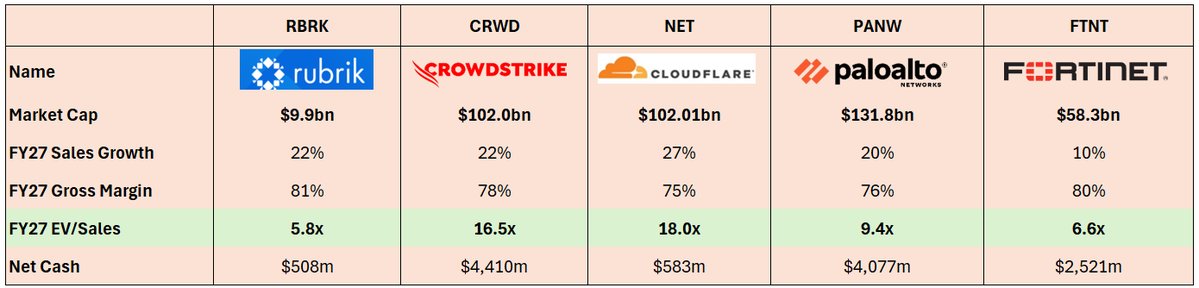

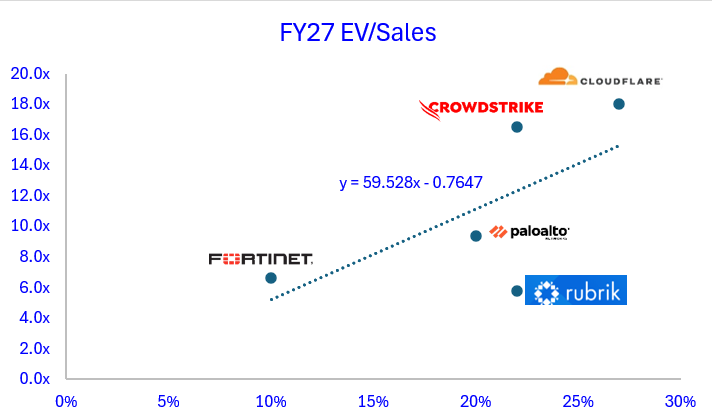

- 🇺🇸 $RBRK: Investors are back into Cybersecurity stocks following $FTNT's strong Earning Report. Rubrik stock is currently trading at 7.67x EV/2027 Sales with 22.09% revenue growth compared to 9.38x EV/2027 Sales with 10.66% revenue growth for $FTNT.

Rubrik grows two times faster that $FTNT and could benefit from a rerating over the next few months.

- 🇺🇸 $META: Today, market participants are expressing concerns about $META's capital expenditures, particularly its spending on AI infrastructure. Similarly in 2022 investors were selling $META stock due to massive investments made in the Meta Universe (at some point the stock was traded at $90). Over the following years $META Stock went up 6-7 fold. It has been a costly mistake to doubt Mark Zuckerberg. We believe the same thing is happening Today.

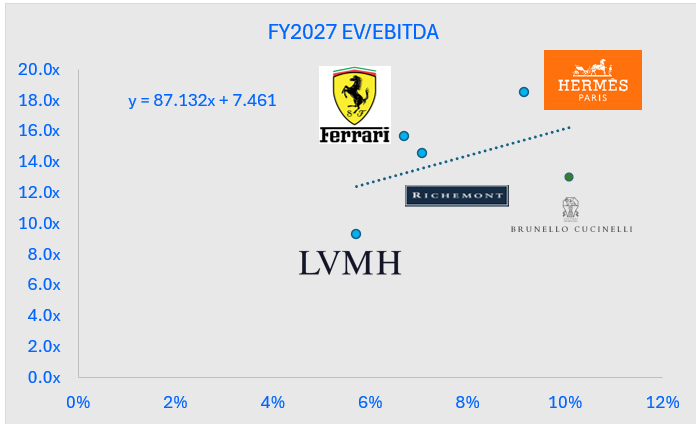

- 🇮🇹 $RACE: Investors are overthinking about the ongoing war in the Middle East. In the short-term sales might be affected by the conflict but the demand for these iconic cars will be restored over the long-term.

$RACE Stock is trading almost at a 5Y-Low in term of EV/EBITDA (Today at 17.2x vs 5Y-Low at 16.56x). Consequently, we believe the stock is attractive for long-term investors.

How your portfolio is performing? 🤔

English