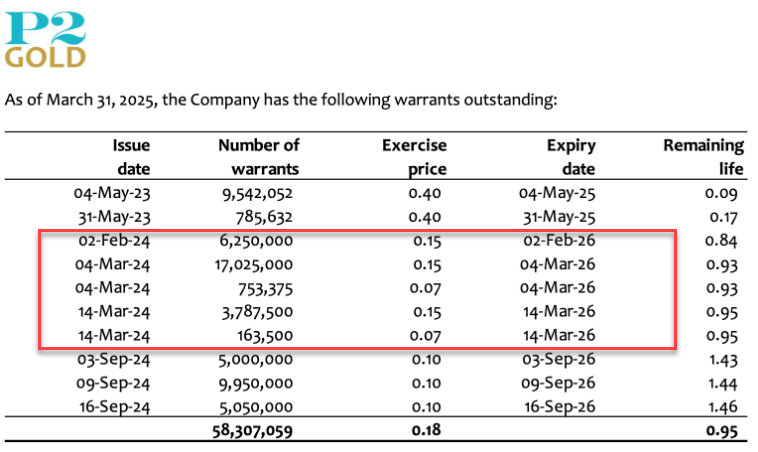

Current drilling will focus on increasing M&I resources. Any larger step out or deeper hole will just have potential to add inferred ounces. For FS you are only allowed to use M&I (PEA is ok to use Inferred resources) so that’s why they’re going after M&I now.

In the future I’m sure they will put in a couple of deep holes to find out if there is anything significant below. Including current financing P2 has + C$20mm on the bank.

English