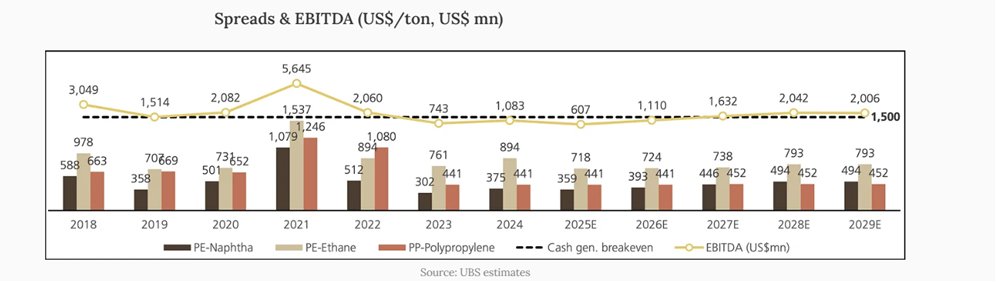

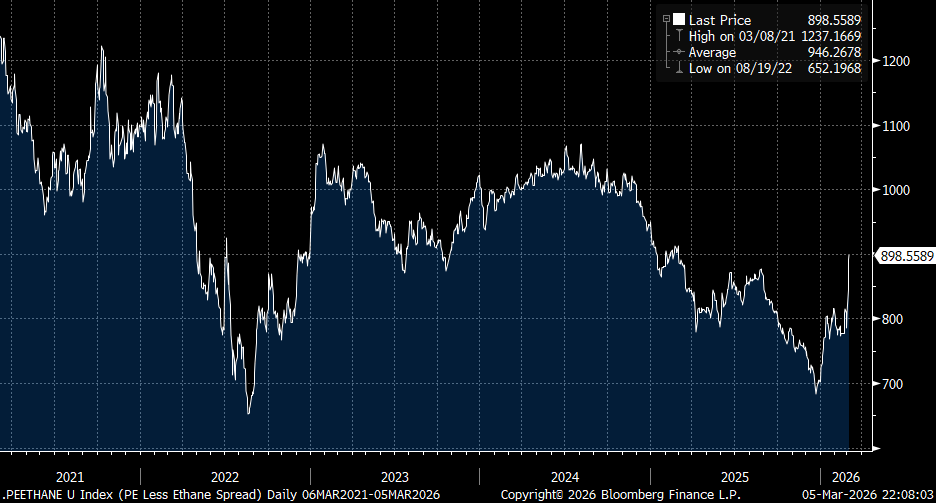

$BAK quick and dirty. $BAK uses North American natural gas-linked feed stocks to produce plastic resins and other chemical base products. US/N. Am. Ethane is a primary feedstock and their end products are generally priced with a rough oil (brent) price linkage. The PE-Ethane spread, a good indicator of $BAK profitability has blown out following the war outbreak in Iran. The spread was in the $700/mt range pre-conflict, and is now ~$915/mt, with momentum accelerating to the upside given a cascade of chemical plant force majeures in the ME and Asia over the past few days. A lot of petchem supply offline in the Middle East and Asia and obviously oil prices are up, while US natural gas/ethane prices have remained largely flat. $BAK is a spread business and recent developments have been good for margins. In 2018, the $BAK PE-Ethane spread was $978 for the year according to the chart below from US. The company did $3B of EBITDA in 2018. Consensus is looking for ~$1.1B of EBITDA in 2026 (Second chart below from UBS). That's a big delta... Enterprise Value as of right now is ~$12BN, so that’s a ~12x multiple on consensus EBITDA for 2026. Call it 10x just to be conservative. 10x * $3bn = $30bn EV. Less ~$11B net debt is ~$19Bn implied market cap. Market cap today is…$1.5Bn That's a big delta... Spreads obviuously need to stay at current levels for a while and the company needs to operate well (certainly no guarantee), but $BAK capital structure is 90% debt and obviously it has a huge fixed cost base. So big financial leverage+big operating leverage+unexpected positive inflection in pet chem margins. Market just has to believe this thing is not going BK…which, don’t get me wrong, it very well still might…but even the prospect of no BK could result in a 2-3x from current prices…let alone the 10x+ scenario I just laid out above… No material debt maturities until 2028 and Brazil elections in October (slim possibility of a swing to the right...), so likely have some time regardless until a restructuring is a forced requirement. Probably the highest beta oil bet in the market today and the stock really hasn't begun to reflect the prospects of a protracted war in Iran and structurally higher oil/petchem prices. $BAK charts courtesy of UBS. @calvinfroedge @contrarian8888 @hkuppy