Mmmg

28 posts

@jbulltard1 this is my vibe coded dashboard that i use for myself.

i guess the notional really wasn't that big so easy to miss it.

English

wonder if these guys knew.

another name that rarely see action until recently...

@jbulltard1

Stock Talk@stocktalkweekly

Lumen $LUMN is up +18% this morning. As usual, we were ahead of the herd. This is the thesis I shared with our members on April 15th...

English

@Pablo01618 I hope this happens. Bought $gfs recently... of course it is the weakest among your picks.

English

Elon needs access to bigger chips.. not bleeding edge like $intc makes IMO as it has been for almost a year now there is one logical choice $gfs $TSM has exited the GaN business and gave it back to $GFS I believe this is a critical error on $TSM part and will cost them billions of dollars.. while margins will be depressed an inkind play that should be intermingled here is $NVTS these are all things we have talked about at length in our substack.. so I will say it today again I believe $gfs will partner with Elon… just my two cents I’m long as fuck all of the above except for $tsm

English

$VIAV - i added some as planned. my stop remains the same; daily close below $50 and im out..

Nir@NirAoo7

$VIAV - getting tight above 5ema. would not be surprised, if tomorrow it tags/U&R's 5ema and goes.. have a position from 4/30, will look to add as long as $50 holds on closing basis.

English

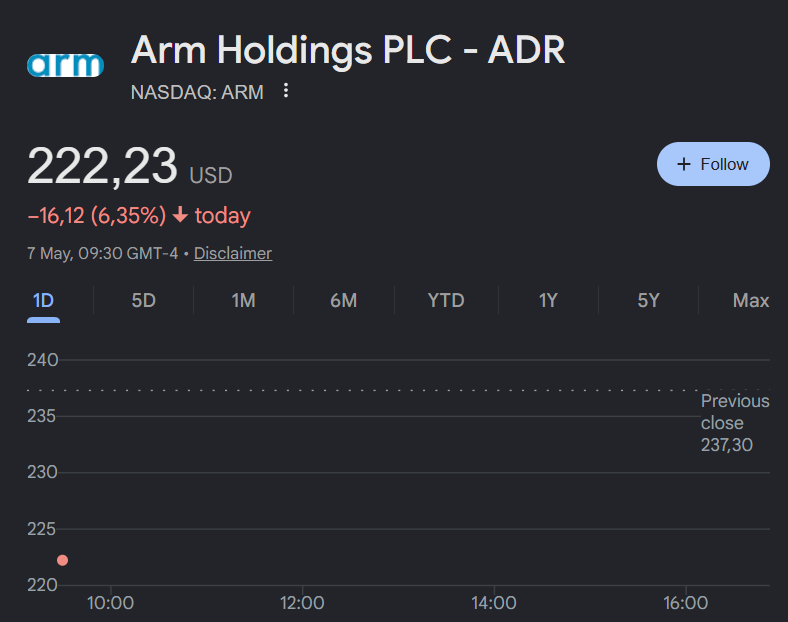

@ShakePryzby1 Sold all of my stocks today, $arm $glw and $amkr. Feeling like I sold the bottom but I just don't want my gains to evaporate in case more downside.

English

Have been absolutely slinging it but feel it’s time to take that foot off the gas pedal and brace for some impact.

Over past two days took exposure levels from ~120% down to ~25% core positions, trimming or outright selling the collective of $ARM $DOCN $NAVN $GLW $APLD $CRML $QCOM $NBIS

Ready to reload on any decent pullback, feels silly to have the boat loaded with open PnL up here as we’re finally starting to see the parabolic activity slow. A pullback to the 10 day will feel like the world is ending in momo-land. I want to have the flexibility to buy the puke rather than be the one doing said puking.

Time will tell whether this is the right or wrong decision. But until then, this cutie & I will be working on our jumpers. 🏀

English

$ARM is down for a simple reason.

The company it is being hit by the same constraints as its peers as it transitions to manufacturing, notably $ANET. Components are in short supply.

$ARM confirmed accelerating demand - up to $2B for its new AGI CPU, but shared that it has secured enough components to meet ~50% of it, only.

This doesn't mean they won't fulfill it, but that they might have to accept higher prices and a potential hit on margins to meet accelerating demand.

Fundamentals remain extremely strong. Management expects a ~4x increase in CPU demand by 2030, but that also means a ~4x increase in component needs. And at today's valuation... That's a hard pill to swallow.

Now let's see if the market choses to rewards the actual trend and massive demand, even at today's valuation, over the shortage and margins issues. I'd know the answer to that question for any sector in the markets today, but this is AI hardware.

Today's going to be interesting.

The Few Bets That Matter@WealthyReadings

Market seems wrong on $ANET They don't do scale-up. Scale-out is without competition and scale across is growing rapidly despites some narrative on competition and alternatives. The numbers are strong in their key sectors and demand follows. Yes margins are a bit hurt on prices due to memory shortage. Okay. Fair. But that's about it. Revenue growth and guidance beat expectations, their core business is strong and cash generation still is growing as revenues acceleration on slightly lower margins - which is temporary, means more cash. Doesn't feel like it deserves this reaction.

English

@ParadisLabs Do you see $amkr as one of the best stocks to own for your advanced packaging thesis? Thanks

English

MEC Company (4971) up a steady 22% following my thesis:

Clean play on the advanced packaging bottleneck imo, at just $1.3B MC + very strong balance sheet:

-> MEC has 90% mkt share in the chemicals needed for FC-BGA substrate production = structural monopoly.

= huge pricing power for MEC.

There's massive Packaging demand, e.g. CoWoS, ABF substrates for NVIDIA/AMD accelerators rn.

So every new Blackwell/Rubin rack needs more adv. substrates = more MEC chemicals.

Then they also have tailwinds from substrate makers themselves:

- Ibiden just announced ¥500B capex (FY26-28) for IC substrates

- SEMCO and others are raising FC-BGA prices + say demand exceeds production capacity by 50%+.

MEC's chemicals are a tiny % of BOM but non-substitutable after qualification:

- meaning they upgraded FY2027 op. margin to 30%.

- and have moved away from a cost-plus model toward one that captures a premium.

Nearest catalyst is Q1 earnings on May 12th.

Market seems to pricing in continued margin expansion + further guidance raise.

Paradis Labs@ParadisLabs

Trade idea: MEC Company (TYO: 4971) at just $1B MC: (I’ve had a position since last year, but now synthesizing + sharing my latest research) > A sole provider of molecular bonding chemistry that facilitates metal-to-substrate interface > Mkt share >90% in Flip-Chip Ball Grid Array (FC-BGA) substrates needed for AI accelerators > The only ones that provide the chemical solution to stop organic substrates from cracking under high thermal loads in modern GPUs > Able to leverage its structural monopoly to raise prices MEC is effectively a single point of failure for the entire semis industry. If their chemicals aren’t applied, a $40k GPU may as well be used as a paperweight since it’ll just become obsolete = huge pricing power. > MEC’s monopoly is even more obvious in their control over the back-end packaging stage which is a huge bottleneck They have super-roughening chemistry that forms tiny topography on copper surfaces to ensure resin adheres permanently. MEC’s competition (e.g. MKS Atotech & JCU) other solutions, but they lack MEC’s laser-focus on high-end interfacial roughening. Substrate makers like SEMCO, Ibiden, and Shinko are fundamentally dependent on MEC: The cost of MEC’s chemicals is a rounding error of the total module value. Yet its performance is the only thing standing between a high-yield production run and a multi-billion $ catastrophe. The impact is huge pricing power for MEC… MEC’s Phase 2 Medium-Term Management Plan (Feb 2026) aggressively upgraded FY2027 op. margin to 30% (from 20%) - they’ve moved away from a traditional cost-plus model toward one that captures a premium for its crucial role in the industry. Major customers like SEMCO have stated that demand for AI-grade substrates exceeds production capacity by 50%+, forcing them to raise their own selling prices by ~10%. And since MEC’s chemicals are "designed-in" to the R&D roadmaps of Ibiden and Shinko yrs before mass production, switching to a competitor is basically impossible during a chip’s lifecycle. That structural advantage is now accelerating as the industry enters the "Glass Age" in mid-2026: As $INTC and Samsung move to glass substrates for 1.4nm-class nodes, traditional physical roughening becomes obsolete due to signal integrity loss at 1.6T speeds. On financials: 0 debt and $51.3M cash - they’re self-funding their new Kitakyushu plant that’ll add 30,000 tons of annual capacity by Dec 2026. Perfect timing for peak growth of glass-core adoption in 2027. And confirmed by their CEO in Feb 2026: "Today, increasing demand for generative AI is driving increased need for semiconductor mounting technology that achieves higher performance and lower energy consumption. We provide global markets with the chemical product processes that are essential to such advancements in leading-edge technology". This essentiality is mirrored in Digitimes' report: "FC-BGA has been selling out since the second half of last year... negotiations for additional price increases appear to be proceeding in a favorable direction." And on top, an industry exec said: "With FC-BGA demand continuing to grow, led by global Big Tech, supply from existing corporations is not enough…” In terms of supply chain standings: 1/ Specialty raw materials & Feedstocks: - Japanese chemical names like Mitsubishi Gas Chemical & Adeka providing acids that MEC optimizes into concentrates + Nittobo for T-glass fiver cloth 2/ MEC Co - 90%+ monopoly in FC-BGA adhesion promoters 3/ Substrate fabs - Ibiden, Shinko and SEMCO - all tethered to MEC due to their chemicals being designed-in during 18-24 mth certification cycles = makes switching rivals impossible without risking yield crashes. 4/ Advanced packaging & foundries - TSMC (CoWoS), Intel (Foveros), and Samsung depend on MEC’s process to facilitate transition to glass-core substrates - as MEC provides the only qualified molecular interface capable of maintaining 1.6T integrity for 1.4nm nodes 5/ Hyperscaler - $NVDA (Blackwell/Rubin), $AMD, and custom silicon designers at $AMZN and $GOOGL Big fan of the company given huge power over the supply chain rn, but understand why they may be too far upstream for some w/ a less diversified port.

English

@crux_capital_ Read this at 6:50 am and added again once 7am hit. Thank you!

English

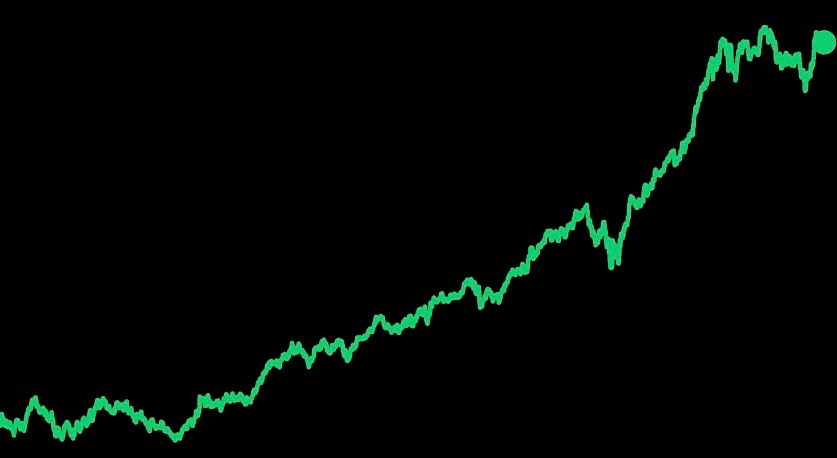

$LITE and $NOK earnings are giving a major signal for $GLW.

GLW grows when AI networks need more fiber density.

> More buildings connected.

> More data centers linked.

> More campus-scale networks.

> More parallel optical paths.

> More fiber packed into the same conduit.

LITE said scale-across is accelerating and now a major growth engine for them

So reinforcing that AI compute is spreading across buildings and data centers, which requires more high-capacity optical links.

NOK last week said the industry is scaling from hundreds to thousands of fibers between data centers.

Confirming that this is also becoming a physical fiber-density problem.

GLW already told us how they benefit.

> Their hyperscaler LTAs are driving expansion across Optical operations, including fiber.

> Their GenAI fiber/cable system can fit 2–4x more fiber into existing conduit.

> Their Optical Communications sales grew 36% YoY, with carrier growth coming largely from data center interconnects.

So.

> Scale-across creates more links.

> Multi-rail creates more parallel paths.

> More parallel paths create more fiber-density demand.

This is why I like Corning. If you believe in the continued growth of the entire optics trade and AI data center buildout, you believe in Corning.

NFA of course.

Gaetano@crux_capital_

$GLW Just finished up the call Some notes >2 new hyperscaler deals (similar in size + duration as Meta) > Lots of excitement around next week's event > Will be discussing new products + springboard updates > Sees robust demand across solar + optical > Some solar drag in Q2 due to facility shutdown/transfer Full report coming later

English

It literally took reading comprehension paired with the weekly and daily chart to see $GLW but go ahead chase it up for me now

English

this is my horse $GLW

Connor Bates@ConnorJBates_

$GLW Tightening up on the right side of this base. Investor day on Wednesday.

English

My hopes are up $GLW

Is anyone else heavy in here going into tomorrow?

Gaetano@crux_capital_

$GLW Do we think they hit ATH after Wednesday? I am expecting a significant TAM expansion

English

@steve2bacon It will probably test $72 again before breaking out! Keep it on your watchlist. :)

English

@Mmmg3147 charted that sunday but didn’t take a position. shame

English

@AdityaInvests90 @Remzztrades Yes, that's why I sold at $103. But it did go down to $90 when he said he wouldn't touch it. So good call

English

@Remzztrades Not offense but wasn’t it you who said u won’t be touching circle cause of the news that came out

English

$CRCL

This was a top focus for me coming into today and it paid very well.

150% and 85% on calls in a single session.

I liked it for two main reasons:

$BTC has been trying to break toward $80,000 this entire rally, yet it’s been a clear laggard versus the broader market.

I noticed some solid relative strength in last night’s overnight session, which immediately caught my attention.

($MSTR is starting to look interesting as well. $COIN has been trying, but it’s been a bit tougher to trade in this range.)

The $100 level on $CRCL was a clear psychological level. I was looking for a backtest at the open but it never came.

Had a second trigger mapped out at $109. Once that broke, it opened the door to $120 which hit today.

Next level is $136.

Keep in mind earnings are this month, so a move toward $170–180 is definitely in play.

Keep it simple.

English

@StockKrypto88 @aleabitoreddit Yes, curios to know your thoughts on $amkr.

English

@aleabitoreddit Great run for the $SIVE ! Any thoughts on $AMKR ? If its a added value if i made an entry now since there is a packaging bottleneck. From what i researched TSM gonna be sending AMKR in the form of chiplets rather then full packaged AI chip. AMKR becomes important in this process.

English

It's pretty insane to see $SIVE become a Tier 1 laser supplier for CPO.

This is my prediction/guess with est. mapping:

$NVDA ate up all the capacity with $COHR, $LITE after their new $2B+ spending spree.

Same playbook with EML early 2025, causing the bottleneck seen today.

Now, $AMD / hyperscalers are scambling for upstream laser suppliers.

Hence why $SIVE + Win / $GFS became likely primary route to go down.

You can see this with:

-> $MVL CPO through Celestial (Nvidia signed a deal, but they don't have lasers)

-> $AMD CPO

-> Ayar

-> $POET

-> Lightmatter

-> and other programs (eg. Jabil 1.6T)

As a result, Sivers/Win emerged as the Tier 1 bleeding edge + critical independent laser supplier.

And there's hints for this when:

1. $GFS listed $SIVE / $LITE as the two only public laser suppliers in their ecosystem.

2. Ayar removed $LITE / $MTSI off their website and elevated $SIVE to their primary laser supplier.

So everyone else ended up going with Sivers since $COHR / $LITE are fully allocated.

My guess is that a lot of the secondary suppliers also capture overflow as architectures standardize.

But scramble for this chokepoint will be insane early next year given $NVDA bottleneck.

And a small $1.2B Swedish company in $SIVE will be in the center of it.

English

8.25 year CAGR of low 40%.

Bright spots: Strong Risk management $TWST

~90% YTD, $GOOGL at 390's represents >200% gain on largest ever investment, $AMZN rebound.

However, most success came in trading account w/ likes of $UAMY $ARM $FLY $RKLB etc.

Not so good: Many core top 10 positions lagging such as

$BABA $SE $MSFT etc. Plus couple of small realised L's. Could have defended gains better w/ trailing stops. Looking forward to the rest of the year!

English

Monthly Portfolio and Performance Update

(post will be out in few days)

Performance since Inception of SSC:

'23: +94%

'24: +61%

'25: +57%

'26 YTD: +8.3% Combined LT and Dedicated Trading Account (~10% the size, up >45%)

TWR is +431.07% vs SPX 89.07%.

English

The $GLW weekly looks like a tree shake to the 10ema that has held since May 2025

About as low risk as it gets imo, yeah I know it was down today cry me a river

English