@UpslopeCapital Costco is an elite business and probably one of the best in the world but it is not cheap under any circumstance. In fact, if you buy it today at these prices, don’t expect to make a serious ROI

English

Nandan Moza

1.6K posts

JUST IN: Berkshire Hathaway increases its stake in Google by 200%

$NU has quietly built the largest SME customer base in Brazil. They now have over 5M SME accounts. They built this base with a customer acquisition cost of nearly zero. They achieved this by cross-selling to their existing 110M individual users who also run small businesses. Now, they are pushing new secured and unsecured credit lines to these businesses and moving upmarket to target companies with 10 to 15 employees. Management views this as a massive, unpriced advantage. Analysts questioned why Nu heavily increased their cash provisions for bad loans. Management clarified that this is not a prediction of a crashing economy. They explicitly stated that their underwriting models always assume the future will be worse than the past. They also keep their loan durations intentionally shorter than the market average. This short duration allows them to pivot immediately if loans start failing. Their internal models do not even account for two massive upcoming tailwinds of a new Brazilian income tax exemption for workers making up to 7.4K reais a month, and a new government debt renegotiation program. Competitors are aggressively pushing private payroll loans because they are supposed to be safe and secured. Nu is intentionally moving slow in this market. They found hidden risks in the system, noting an incredibly high 10% to 15% first-payment default rate for a supposedly secure product. Nu is also refusing to charge high interest rates on these loans because they expect the government will eventually cap the rates. They are letting their competitors absorb the regulatory risk while they wait. Nu posted a record-low efficiency ratio of 17.6% in the first quarter. Investors should not expect this exact metric to last. Management admitted that roughly two-thirds of this beat was just caused by timing. They pushed certain real estate and marketing expenses into later quarters. The true efficiency ratio for the full year 2026 will rise back up to roughly 20%. However, the remaining one-third of the efficiency gain is structural and permanent, driven directly by replacing human operations with AI. 👏

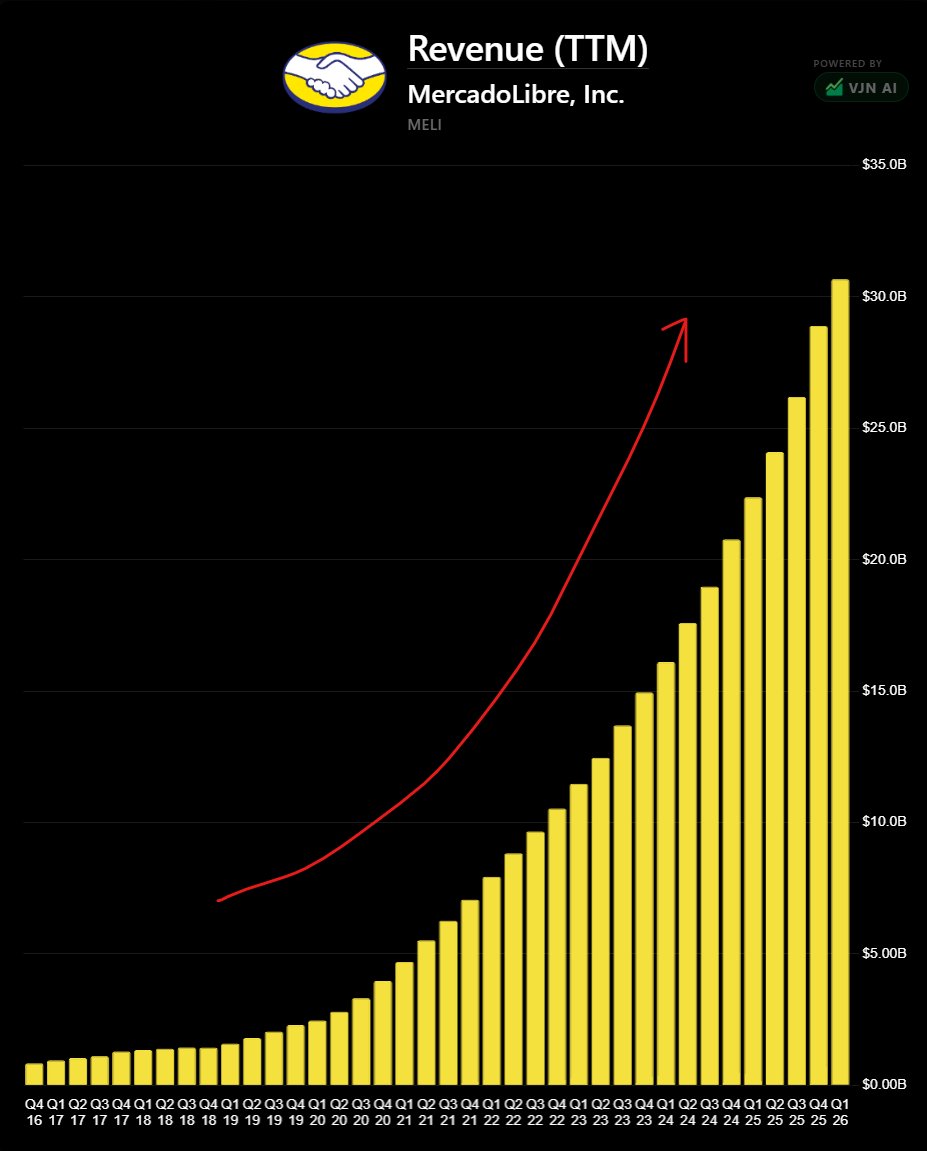

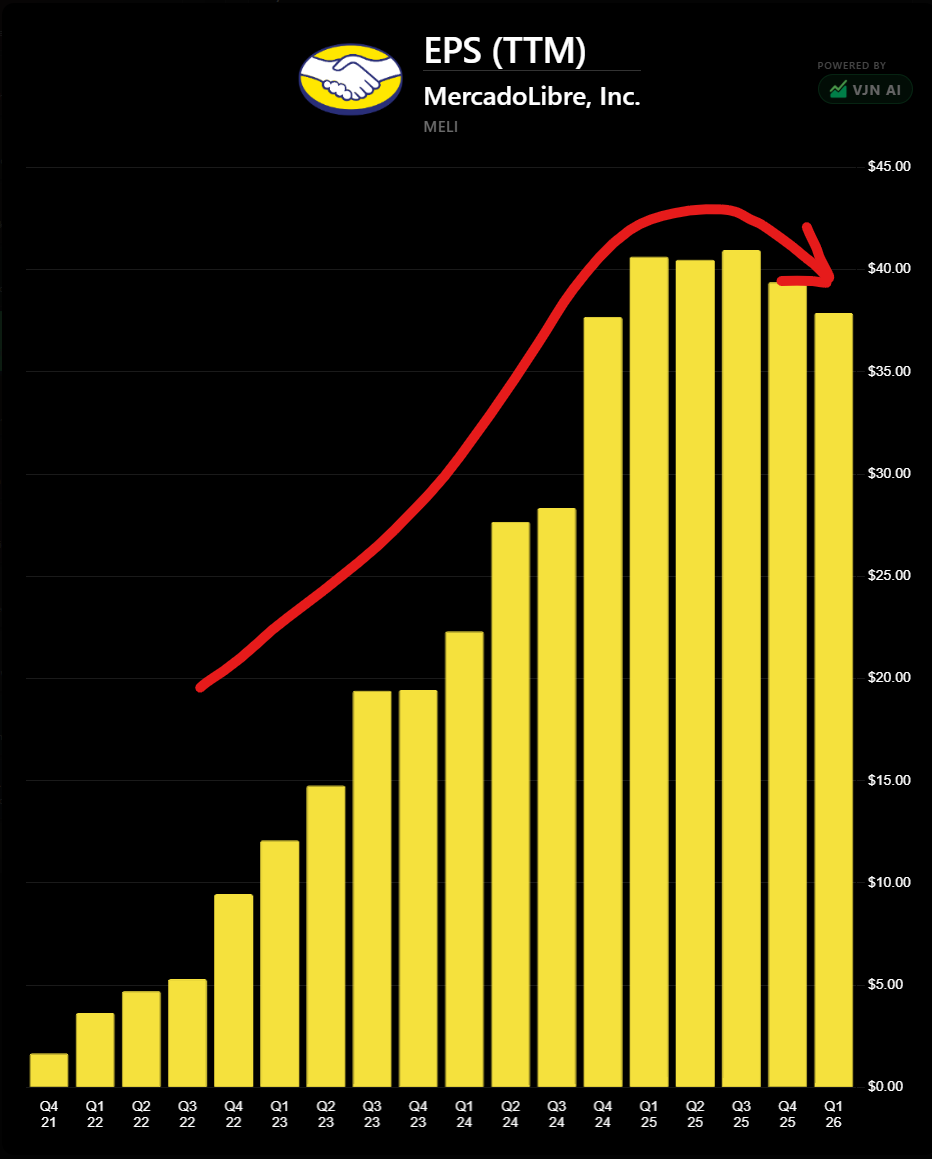

Bumping this piece up on $MELI I am seeing a lot of comparisons being thrown around to stocks that performed well in the past but are now out of favor. As if the market is just magic and price follows vibes. I admit MELI is out of favor from the institutional view but not because deterioration, competition or even just compressed margins. Its out of favor because management has made it clear that they are focused on building a new TAM. Why do institutions not like this? A few reasons. Short-term it is costly. The growth of the credit card portfolio is crushing margins upfront. Ignore the ecosystem lock-in and stickiness. Its crushing margins upfront. Then there is the risk-factor. And no bull can ignore this. The credit business is growing much faster than the rest of the business. This changes the risk-profile regardless of how well management executes. So despite, the opportunity ahead it is objectively riskier to loan out more and to riskier cohorts. However, this is the secret weapon behind killing competition. Management sees what credit is doing to their user behavior. Capturing the downmarket credit users strengthens their position where the biggest ecom competition exists. Its a customer acquisition/retention tool written off as pure systemic risk. Then there is the question of whether they can manage this much sub prime credit. Well they kind of are already demonstrating how they mitigate risk. The portfolio showed little sign degradation despite rapidly expanding and Argentina’s credit stress. This is a clear indicator that they are managing the risk well. They also mentioned on the call how they tightened their lending standards specifically in Argentina because of the risk. There is plenty of evidence that the strategy is working and only going to get better as their models improve with tech and data. Bears may celebrate the next couple of quarters but their reasoning is dead wrong.

$MELI when stocks shift their ownership base its always going to be painful. E-com has been like that for some time. Shareholder base shifts from growth to quality and then finally… value! And thats the nail in the coffin ⚰️ Do yourself a favour ignore and look elsewhere! ✌🏼

I see an insane amount of brain damage on my feed regarding $MELI Its hilarious to me, and a complete waste of time. This stock has just consistently failed to properly break new convincing highs since the ecommerce top in ‘21 (same with $CPNG and $SE) people