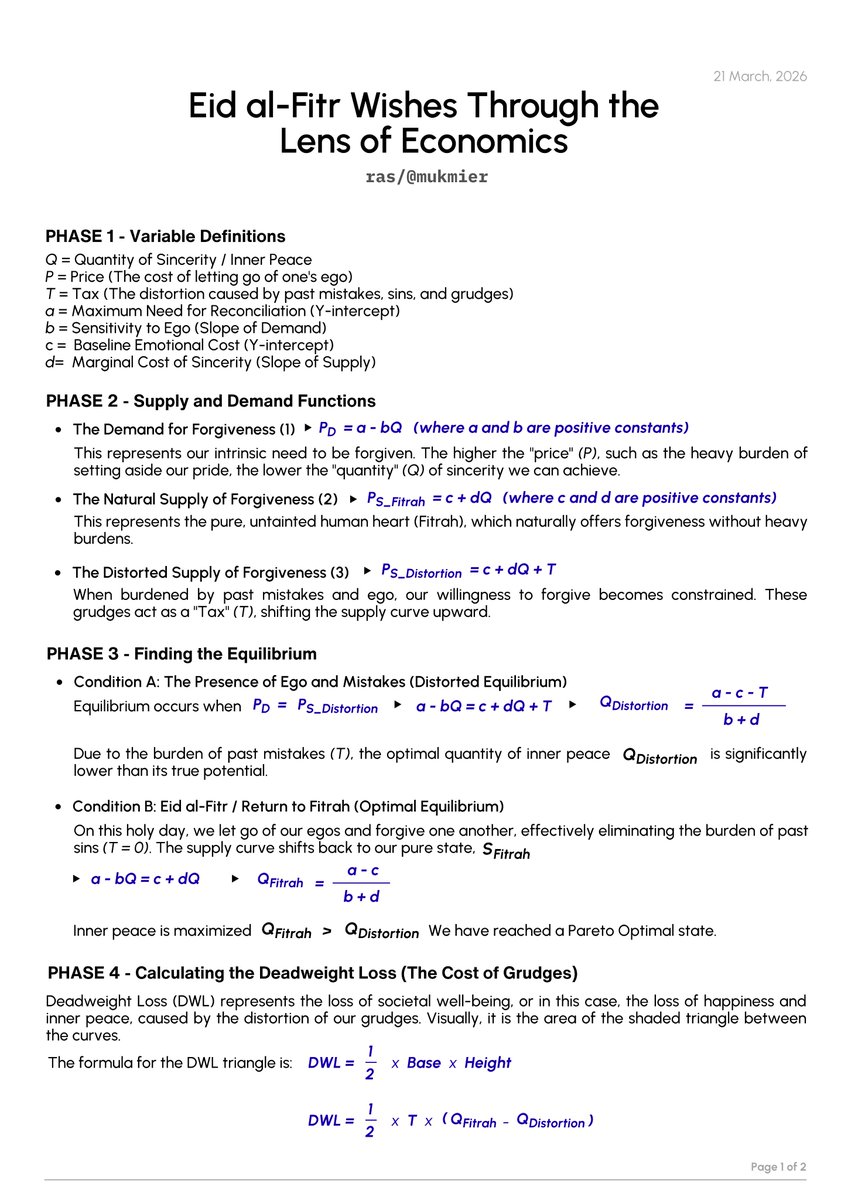

Happy Eid Al-Fitr to everyone celebrating! On a whim, I created a little illustration mapping the concept of 'returning to fitrah' to DWL and Market Distortion in Welfare Economics. It’s definitely been a minute since I last delved into micro! :D

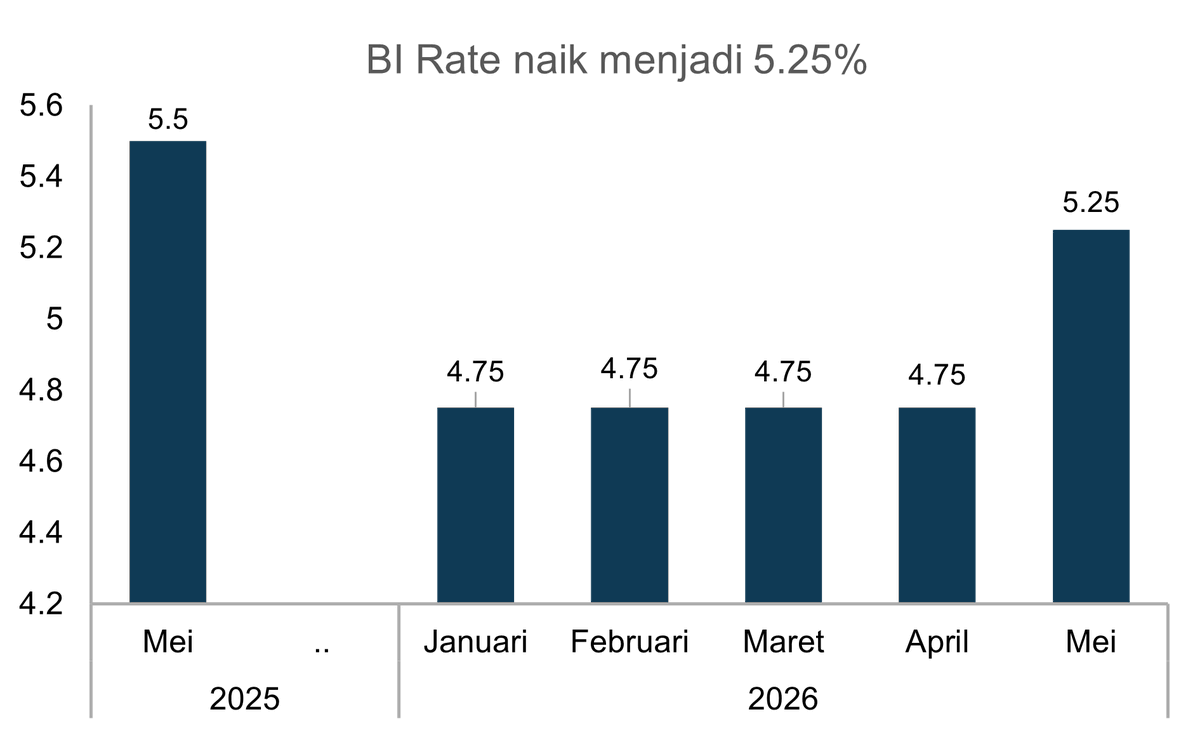

@thinkorseek wkwk I still remember our chat back in March about how BI 'seemed' late to hike rates. At least our discussion 2 months ago basically pointed to 2 rate hikes in the end anyway 🤣

@notintofinance lagi cari Report Designer nih

Job descnya simpel, cuma design analysis yang udah kita bikin jadi report yg rapih & engaging:

1. Diutamakan mahasiswa

2. Fully paid & remote working

3. Kalo bisa asik, krn kita kerja sambil ngelantur wkwkwk

Bisa langsung dm gue aja ya dan lgsg kirim portfolio / cv 🧙♂️

#infoloker#infomagang

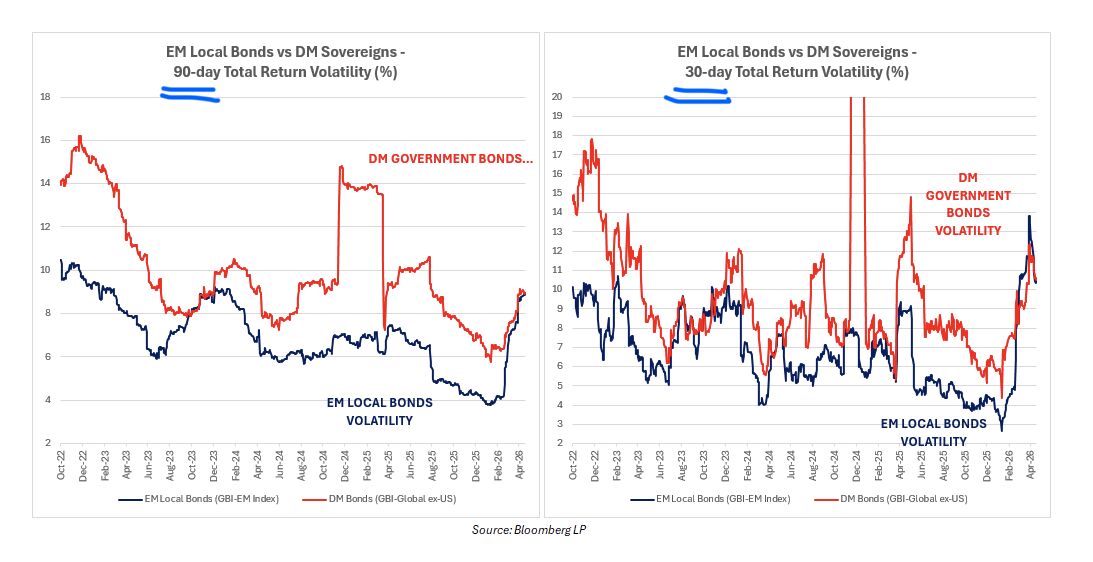

US Treasury 30-year yields are now above 5%, sitting around 5.06%, and that is globally consequential especially when it is happening alongside rising JGB yields in Japan.

The issue is not simply that developed market yields are moving higher. The real issue is that the global risk-free rate itself is repricing upward at the same time fiscal deficits, geopolitical risks, and inflation uncertainty remain elevated.

For emerging markets, this matters enormously. If you are an economy running a current account deficit, you structurally require capital account inflows to help fund that imbalance. In other words, you need foreign capital to keep coming in consistently. Once US long-end yields move above 5% while Japan also begins offering higher domestic yields, global capital suddenly has more attractive lower-risk alternatives.

That naturally raises the question: what level of compensation are emerging markets offering investors for taking additional currency risk, governance risk, liquidity risk, and policy risk? This is fundamentally a risk premium discussion.

When global liquidity was abundant and developed market yields were near zero, investors were forced further out along the risk curve into EM equities, EM bonds, private markets, and frontier assets. But once the US Treasury market itself begins offering historically attractive nominal yields again, the hurdle rate for EM capital allocation rises materially.

Countries with strong institutions, credible policy frameworks, current account surpluses, stable currencies, and predictable regulation can still attract capital. But weaker macro structures become increasingly exposed because global investors no longer need to stretch for yield the way they did during the zero-rate era.

This is also why several EM currencies continue struggling despite officially solid growth numbers. Capital ultimately flows toward the best risk-adjusted returns, not simply the highest headline growth rates.

In Indonesia’s case, the situation becomes more sensitive because the economy still relies meaningfully on foreign participation across bonds, equities, and strategic investment flows. At the same time, markets are increasingly questioning policy consistency, regulatory predictability, fiscal transparency, and the broader investment climate following recent developments around commodity policies, DHE rules, downstream regulations, and institutional governance concerns.

That does not mean Indonesia lacks long-term potential. Structurally, the country still possesses major advantages through demographics, natural resources, industrialization ambitions, and strategic positioning within global supply chains. But in a higher global yield environment, investors become significantly more selective.

The spread between Indonesian assets and developed market risk-free yields must now compensate investors adequately for: 1) currency volatility, 2) policy uncertainty, 3) governance concerns, 4) liquidity risk, and 5) external funding dependence. If that compensation becomes insufficient, capital outflows and rupiah pressure can intensify even if headline domestic growth remains relatively solid.

This is ultimately why credibility matters so much. In a world where the US Treasury itself yields above 5%, emerging markets can no longer rely purely on growth narratives. They increasingly need institutional credibility, predictable policy frameworks, and investor confidence to compete for global capital.

The broader implication is that the world may be entering a structurally higher cost-of-capital regime. In that environment, risk premiums matter more, policy credibility matters more, and institutional quality matters more.

Cheap global liquidity is no longer there to hide structural weaknesses.

Hopefully, this sheds some light on why the Malaysian Ringgit remains quite resilient amidst the current conditions.. (Why is this relevant? Because Indonesian netizens frequently benchmark our currency against neighboring countries)

Hard to believe it’s been 10 years since AlphaGo! It was wonderful to catch up with Lee Sae Dol last week in Korea and join Shin Jin-seo for a special Go match. Great to reminisce about AlphaGo & super interesting to hear how it changed the way players approach the game of Go!

This formula perfectly captures the current dynamics of Indonesia's GDP. It really brings to mind the classic debates between the Austrian School and the Monetarists regarding this 'G' variable..

@PeterMcCormack I think this combination is perfect for opines on economics and its impact on investment instruments, especially bonds. Feel free to add if you have any other suggestions..

What's the point of improving a country's fiscal posture and maintaining central bank credibility? One of which is sovereign bonds. Conservative investors are quite sensitive to volatility :D

When asked about the ongoing IDR weakness, it certainly stems from both sentiment and fundamental factors. Yet, fundamentally, the primary anchor remains the same, the state budget (APBN) deficit. And make no mistake, this is a real risk for the Indonesian economy..

Are Thai bonds attractive? Per Eastspring's W16 report, the long-end is intriguing. A >40bps yield surge feels overdone in a deflationary economy. Charting the 10Y here. Is this a worthwhile entry point in such an unpredictable market?

Welcome to Q2! Just before wrapping up Q1, I finally tried Tuku's Kopi Susu Tetangga and Fore's Berry Manuka Americano, and they actually live up to the hype wkwkwk. Yep, that's it.. Back to monitoring macro and bonds! :)