ND

240 posts

ND retweetledi

@0xDeployer @apex_ether How do you have time to be permanently online here replying to everyone and ship at the highest level?

English

There is some absolute larp pretending to be me….

No the bankr team has no paid me because I do not work there 😂😂😂

Stay safu

English

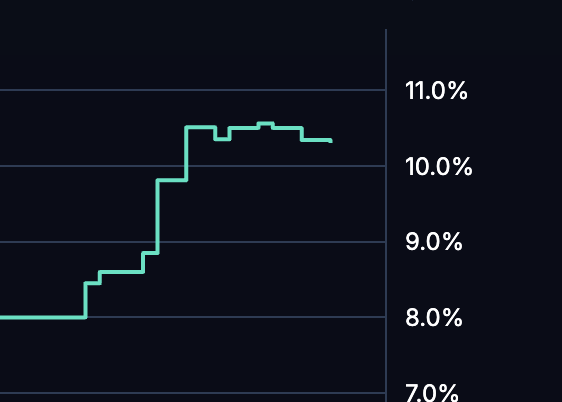

Markets don't lie - everyone does what is best for them

In the 24hrs after our ICO and Stabledrop announcement, our Pendle APR has increased 30% and cUSD supply increased $30M

This is a clear sign that the market agrees with our direction for Cap. Thank you for you confidence - more to come 🧢

English

Top 10 Open Interest back to healthier levels than 10/10

Great start to the year already 🐎

McKenna@Crypto_McKenna

Hyperliquid back above $10Bn open interest the first time since October 10th.

English

We are solving liquidity on Day Zero.

You know we don't like risky bridges, we solved this with cBTC for BTC. Now, we're solving it for Citrea's second core asset.

No bridges, no fragmentation.

Regulated reserves that belong to holders.

Welcome to Bitcoin Capital Markets.

English

Bitcoin is the world's best capital, but it lacks compliant rails for true global access.

Meet ctUSD, powered by @MoonPay & @M0.

Native, regulated, and aligned with forthcoming GENIUS guidelines. On-ramps will be available in the U.S. (excl. NY) & 160+ countries.

Citrea | Mainnet Live 🍊🍋@citrea_xyz

Introducing Citrea USD (ctUSD), the native stablecoin for Bitcoin. Issued by @moonpay and powered by @m0's stablecoin platform. ctUSD aims to set a native liquidity standard for the Bitcoin ecosystem and offer banking rails between on-chain BTC collateral and fiat systems. 🧵

English

ND retweetledi

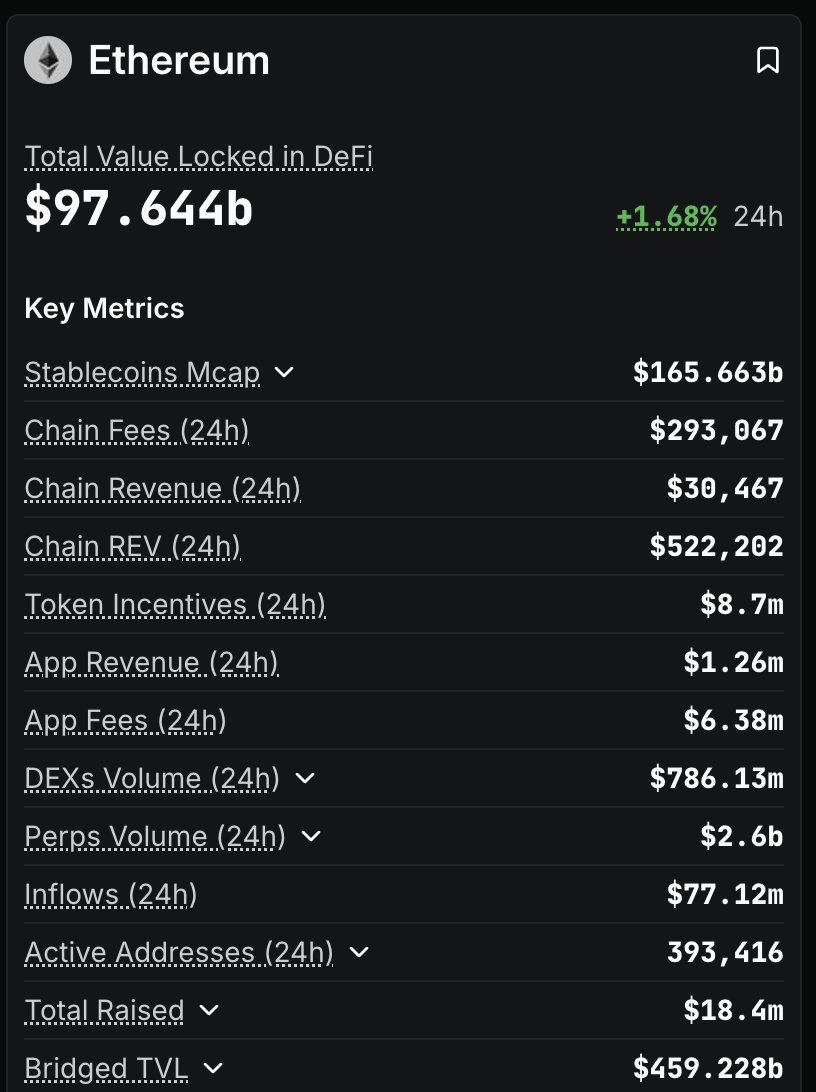

ethereum

raised $18.3m

built before crypto was even an industry

shipped real decentralization

100% uptime

despite dozens of upgrades, it has been running non-stop for 10 years, 4 months, and 15 days

tvl: $97b

total value secured on l2s: $37.8b

home to the most used, real defi applications in crypto

hosts over 50% of all circulating stablecoins

on the l2 side, it has already reached ~32k tps,

with a 100k tps mainnet roadmap ready

the true home of tokenization

the place where long-term plans are made instead of chasing temporary hypes and narratives

the only truly neutral, high-economic-activity blockchain

unlike foundations that dumped unknown amounts of tokens on retail and likely burned through their treasuries, ethereum has been transparent about its treasury for over a decade

hosts over 80% of all rwas

its etf became the 3rd fastest in history to reach $10b in assets

institutions are building on ethereum

and people like tom lee continue to accumulate eth

the global settlement layer

the world computer

it’s sitting at a $377b fdv, roughly the same amount of capital that was wasted and burned by all the so-called competing l1s over the years

so yes, it deserves far more

moon that

hantengri@hantengri

stable raised $28m since probably everyone already agrees this thing is going straight to zero, there’s no point in writing a long breakdown and wasting anyone’s time for now it’s still sitting at $1.5b fdv zero

English

@chainyoda ~40b casually added to ETH mc, more than 50% of the mc of SOL, 10x the mc of Western Union. Keep them coming Santi 🍿

English

$ETH bearishness lasted for years but $ETH actually looks good:

- EF reformed & ships fast: Two major forks in 2025

- Fusaka increases blob fees for L2s

- BitMine continues to stack $ETH

- Noticeable whale accumulation onchain

- Blackrock files for staked ETF

- Strong ETF outflows seem subdued

- Solutions like zkSync Atlas bring technical solutions to solving L1/L2 liquidity fragmentation

- Quantum resistance on the roadmap (vs uncertain BTC)

- SEC & Blackrock pushing tokenization (even within 2 years)

- ETH/BTC chart unaffected by 10/10 and following dumps

Anything else I missed?

English

@santiagoroel You keep referencing Peter Thiel as an inspiration of yours on many podcasts. Guess who is an investor in $BMNR? 9% of the company if I'm correct. Do you think he's also on opium and delusional with $ETH?

English

@hosseeb Can you bring Bezos to debate this? Thank you. @notthreadguy moderates

English

The problem with this analysis is that "revenue" is a tricky word when you are applying it to a L1.

"Revenue" is price x quantity sold. It ignores expenses. On the other hand, profit subtracts expenses to get your actual net income.

So if you look at transaction fees on Ethereum, the naive view is that this is the revenue. In this view, the revenue is embarrassingly low, especially compared to something like Amazon. This is Santi's view.

Another way to understand the transaction fees is that these are not the revenue, but the profit of Ethereum, because Ethereum has no expenses. Amazon grew their revenue dramatically, but not their profit. Amazon continually kept their profit low to reinvest in growth. In 2013, Amazon had a P/E ratio of over 600x—this was because they didn't care about capturing profits yet.

Transaction fees that users would be willing to pay but are not charged are counterfactual profit that Ethereum has elected not to charge. By not charging these fees (by, for example, limiting block space, or even just raising the minimum gas fee a la EIP-7918), Ethereum has chosen to forgo profit in favor of future growth.

This is a weird way to explain it, which is why I think it's better to analogize Ethereum as a city. If you consider Ethereum is a city has a low tax rate on commerce, it becomes immediately unmysterious what it's doing.

Ethereum could raise those taxes if it so chose. Tron has decided to raise its taxes, jacking up fees on the L1 (perhaps detecting that the days of its Tether monopoly are numbered, being threatened by Plasma, Tempo, Arc, etc.), and so monetizing whatever you can now is the rational response. But this aggressive monetization will accelerate the end of the Tron Tether monopoly. One recalls Bezos's maxim: your margin is my opportunity.

It also explains why Tron is trading at a lower P/E multiple than Ethereum. The market agrees on weaker prospects of future growth. It's the same reason why Western Union trades at a low P/E multiple in the face of challenges by stablecoin remittance companies.

If Ethereum were to raise taxes today, it'd do so at the expense of future growth. And Ethereans—and the market—believe that future growth is coming.

Santiago R Santos@santiagoroel

Amazon is a network and arguably one of the most successful networks ever built. Which is why comparisons are uncomfortable: when you line Ethereum up next to real, scaled networks like Amazon or Facebook, the valuation gap becomes impossible to ignore. Ethereum at a ~$380B valuation generates roughly ~$1B in annual revenue → 380x sales. When Amazon carried a similar valuation, it produced $136B in revenue and $2.4B in net income → 2.6x sales. That means ETH holders today are paying ~146x more per dollar of revenue than Amazon investors did. The claim that “Amazon is a company, Ethereum is a network” doesn’t resolve the discrepancy: Networks are priced on the economics they produce: revenue and cash flows. Amazon’s network effects were real, scaled, and monetizable. And the market valued them on fundamentals, not hypotheticals. TVL and “assets secured” are not revenue. Settlement volume is not revenue. TAM is not revenue. At some point, you have to put up numbers on the dashboard to support the big narrative talk

English

@santiagoroel Who cares? ETH is a commodity, not a company. It's the revolution of money that's unfolding, how much is that worth? You can't buy neutrality, decentralization, trust. It takes years and lots of coordination to reach this level. 100% uptime. That's the magnet of liquidity $ETH

English

A very simple way to settle this debate:

Which outcome has a higher probability of happening this cycle?

English

Ethereum is increasingly fragmented across L2s

Your analogy of blockchains as cities is apt. I like it, so I’ll run with it

Ethereum collects city taxes to fund the equivalent of federal-level services (security). I’m not disputing that Ethereum has a meaningful lead. Insert Dune dashboard of choice. But the value capture simply isn’t there. It’s leaking

What’s the point of building moats if you can’t actually monetize them?

English

Ironically the way to express this trade (that major L1s don't have moats) is a pair trade: long emerging L1s, short the majors.

That's what not having a moat actually looks like—easy encroachment by new entrants, and valuation compression among all the competitors. Even if you're bearish L1s on the whole, the pair trade will capture that.

To be clear, I don't agree with this. L1s demonstrably have very strong moats—that's what we see in practice. It's on the naysayers to theorize why the future will be different from the past. Because what Qiao is describing here is what I (and many others) believed back in 2018-2019, and we have 7 years of data showing us how wrong we were.

L1 moats are very deep. That's where my cities analogy came from. San Francisco, NYC are dysfunctional cities in so many ways, but their moats are seemingly uncontestable.

qw@QwQiao

i have a hard time convincing myself to own l1 tokens long term not because the p/e ratios r high, but because they have no moat. without a moat, they become commoditized and can’t capture meaningful value. - users can bridge from one chain to another easily these days. - most app devs can move from one chain to another fairly quickly too (aside from a handful of complex smart contracts). - and it’s never been easier to launch a new chain. their switching cost of blockchains is nowhere near something like aws. the only way as far as i can see for chains to strengthen their moat is to verticalize and own the app layer. my perception is chains solana, base, and hyperliquid have come to this conclusion and r actively working on it. and ofc so do the up and coming corp chains like tempo. its a no brainer to believe in the exponential, but the best expression of this view is to bet on the app layer.

English

In Defense of Exponentials

I used to tell founders, the reaction you are going to get to your launch is not hate, it’s indifference. By default, nobody cares about your new chain.

I have to stop telling them that now. Monad just launched this week, and I’ve never seen so much hate about a blockchain that just launched. I’ve been investing into crypto professionally for 7+ years now. Before 2023, almost every chain I’ve ever seen that launched was mostly met with enthusiasm or indifference.

But now, new chains are born into a chorus of hate. The amount of haters I’ve seen for projects like Monad, Tempo, MegaETH—before they even hit mainnet—is a genuinely new phenomenon.

I’ve been trying to diagnose: why is this happening now, and what does it mean about the psychology of this market?

The Cure is Worse than the Disease

Forewarning: this is going to be the vaguest blockchain valuation post you ever read. I don’t have any fancy metrics or charts to sell you on. Instead, I’ll be arguing against the zeitgeist of Crypto Twitter, which for the last couple of years, I’ve been constantly on the opposite side of.

In 2024, I felt like what I was arguing against was financial nihilism. Financial nihilism is the belief that none of these assets matter, it’s all memes at the end of the day, and everything we’ve built is inherently worthless.

Thankfully, that’s no longer the vibe. We have broken out of that spell.

But the zeitgeist now is what I’d call financial cynicism: OK, maybe some of this stuff has value, maybe it’s not all memes, but it’s grossly overvalued and it’s only a matter of time before Wall Street finds that out. Not that all chains are worthless. But these things are all maybe worth 1/5th-1/10th of what they’re currently trading at (have you seen these PE ratios?), and so you’d better pray like hell Wall Street doesn’t call us on our bluff, because once they do it’s all getting wiped out.

You’ve got many bullish analysts now trying to conjure up optimistic L1 valuation models, inflating PE ratios, gross margins, DCFs, trying to fight against this mood.

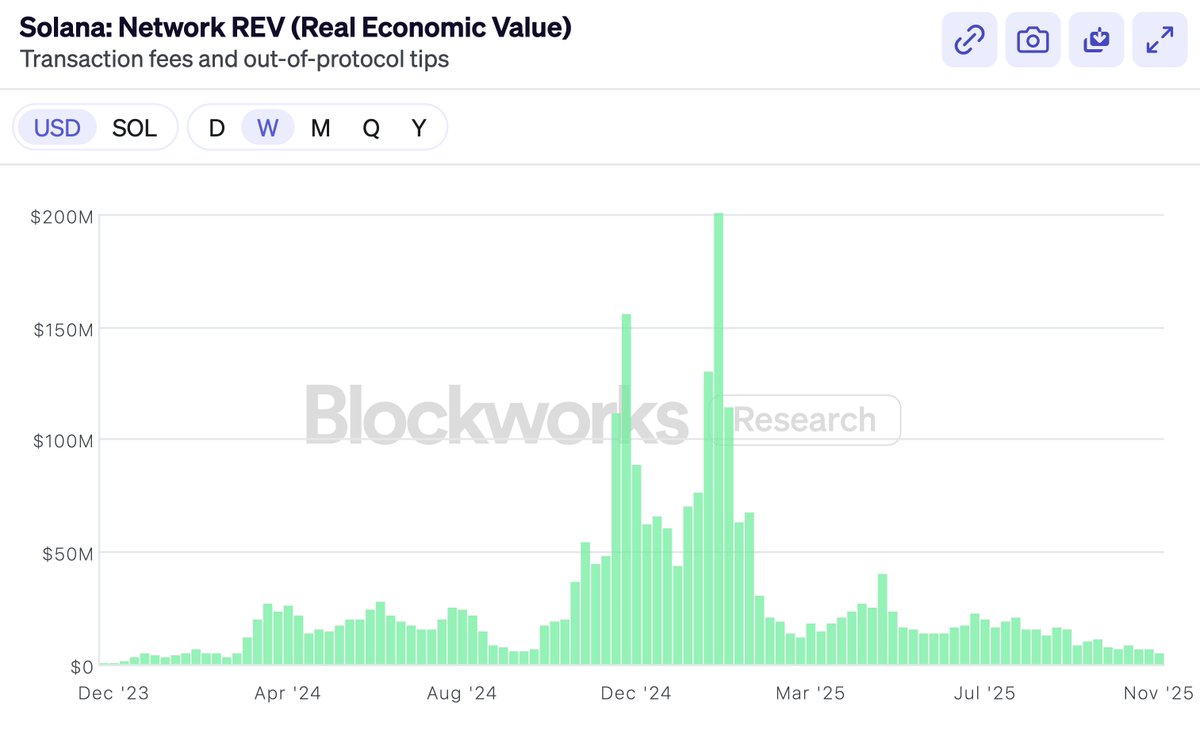

Late last year, Solana very proudly embraced REV as a metric that could finally justify their valuation. They proudly announced: we—and only we—are no longer bluffing to Wall Street!

And, of course, almost immediately after REV was embraced, it fell off a cliff (though $SOL, tellingly, did better than REV did).

Not that there’s anything wrong with REV. REV is a very clever metric. But the point of this post is not metric selection.

Then came the launch of Hyperliquid. A DEX that had real revenue and buybacks and PE multiples. And the chorus said—look, look I told you! Finally, for the first time ever, a token that has some real profits and a proper PE multiple. (Nevermind BNB, we don’t talk about that.) Hyperliquid will eat everything because obviously Ethereum and Solana don’t make any real money, we can stop pretending to value them now.

Hyperliquid, Pump, Sky, these buyback-heavy tokens are all great. But the market always had the ability to invest into exchanges. You could always buy Coinbase, or BNB, or whatever. We own $HYPE, and I agree that it’s a fantastic product.

But that’s not why people were investing in ETH and SOL. The fact that L1s don't have exchange-like profit margins is not why people were buying them—if they wanted that, they could’ve bought Coinbase stock.

So if I’m not critiquing blockchain financial metrics, maybe you think this post is going to be chiding the sinfulness of the token-industrial complex.

Obviously, everyone has lost money on tokens in the last year, VCs included. Alts are down bad this year. And so the other half of the zeitgeist on CT is arguing about who's to blame. Who’s become greedy? Are the VCs greedy? Is Wintermute greedy? Is Binance greedy? Are the farmers greedy? Are the founders greedy?

The answer, of course, is the same as it’s ever been.

Everyone is greedy. Everyone. The VCs, Wintermute, the farmers, Binance, the KOLs, they're all greedy, and you are greedy too. But it doesn't matter. Because no functioning market has ever required anyone to act against their self-interest. If we're right about crypto, we can all be greedy and the investments will still work out. Trying to analyze a market that has gone down by figuring out “who’s greedy” is going to be about as fruitful as commissioning witch trials. I guarantee you, nobody just started being greedy in 2025.

So this, too, is not what I’m going to be writing about.

Many people want me to write a post about why $MON should be valued at X or $MEGA at Y. I’m not interested in writing this post, or advocating that you buy anything in particular. In fact, you probably shouldn’t buy any of them if you don’t already believe in them.

Will any new challenger chain win? Who knows. But if it has a material chance of winning, it's going to be priced on that basis. If Ethereum is worth $300B or Solana is worth $80B, a project that has a 1-5% chance of becoming the next Ethereum or Solana will be priced according to those probabilities.

Somehow CT is scandalized by this, but it’s no different than Biotech. A drug that has less than a 10% chance of curing Alzheimer's is priced by the market as worth billions of dollars, even if 90% chance it won’t pass stage 3 trials and will go to 0. That's how the math works—and turns out, markets are pretty good at doing math. Binary outcomes are priced on probabilities, not on run rates or moral turpitude. It’s the “shut up and calculate” school of valuation.

I really don’t think that’s an interesting question to write about. “5% chance to win? No way, that’s clearly a 10% chance!” Markets, not articles, are the best way to assess that for any individual token.

So here’s what I am going to write about: CT doesn't seem to believe anymore that chains are valuable.

I don’t think this is because they don’t believe new chains can win market share. We just saw Solana dominate market share after emerging from the ashes less than 2 years ago. It’s not easy, but of course it’s possible.

It’s more that people have come to believe that even if a new chain wins, there’s no prize worth winning. If $ETH is just a meme, if it’ll never generate real revenue, then even if you win, you won’t be worth $300B. The contest is not worth winning, because these valuations are all bunk and it’ll all come crashing down before you go to claim your prize.

Being optimistic about chain valuations has become passé. Not that nobody is optimistic—obviously there must be optimists out there. For every seller there’s a buyer, and as much as CT cool kids love to drag L1s, people are comfortable buying SOL at $140, ETH at $3000.

But there’s a perception now that all the smartest people are over buying smart contract chains. Smart people know the jig is up. If not now, then soon. The only people buying here are suckers—Uber drivers, Tom Lee, and KOLs who say stuff like “trillions.” And maybe the US Treasury. But not the smart money.

This is bullshit. I don’t believe it, and you shouldn’t either.

So I felt like I had to write a smart person’s manifesto on why general purpose chains are valuable. This post is not about Monad or MegaETH. It’s really in defense of ETH and SOL. Because if you believe ETH and SOL are valuable, the rest is straight downstream.

Defending ETH and SOL valuations is generally not my job as a VC, but fuck it, if nobody else is willing to do it, then I’ll write it.

Feeling the Exponential

My partner Bo experienced the Chinese Internet boom first-hand as a VC. I’ve heard how “crypto is like the Internet” so many times now that it doesn’t even register for me anymore. But when I hear his stories, it always reminds me how costly it is to be wrong about these things.

A story he often tells is about when all the early e-commerce VCs (it was a small group back then) got together for coffee in the early 2000s. They debated: how big is the market for e-commerce going to be?

Is it going to be mostly electronics (maybe only techies will use PCs)? Could it ever work for women (perhaps they’re too tactile)? What about food (maybe impossible to manage perishables)? These were deeply important questions for early VCs to decide what to invest in and what prices to pay.

The answer, of course, was that literally every single one of them was devastatingly wrong. E-commerce would sell everything, and the target audience was the whole fucking world. But nobody at the time actually believed it. And even if they did, it would be too absurd to say out loud.

You just had to wait long enough for the exponential to show you. Even among the believers, very few thought e-commerce would become as big as it became. And those few who did, almost all of them became billionaires from just not selling. Every other VC—as Bo tells me, since he was one of them—sold too early.

It has become passé in crypto to believe in the exponential.

I believe in the crypto exponential. Because I’ve lived it.

When I started in crypto, nobody used this stuff. It was tiny and broken and awful. TVL on-chain was in the millions. We invested into the first generation of DeFi, MakerDAO, Compound, 1inch, back when they were science projects. I remember playing around on EtherDelta back when DEXes traded single digit millions a day, and that was considered to be a huge success. It was complete dogshit. Now we routinely trade in the tens of billions on-chain every day. I remember believing it was crazy that Tether hit a billion dollars in issuance and was being written up in the NYT as a ponzi scheme on the brink of shutdown. Now stablecoins are over $300B and regulated by the Federal Reserve.

I believe in the exponential because I’ve lived it. I’ve seen it over and over again.

But you might respond—well, stablecoin growth might be exponential, maybe DeFi volumes are exponential, but they don’t accrue to ETH or SOL. The value doesn’t get captured by the chains.

To which I answer: you still don’t believe in the exponential.

Because the exponential’s answer is always the same: it doesn’t matter. This stuff is going to be so much bigger than it is today. And when it’s absolutely enormous, you’ll make it up on scale.

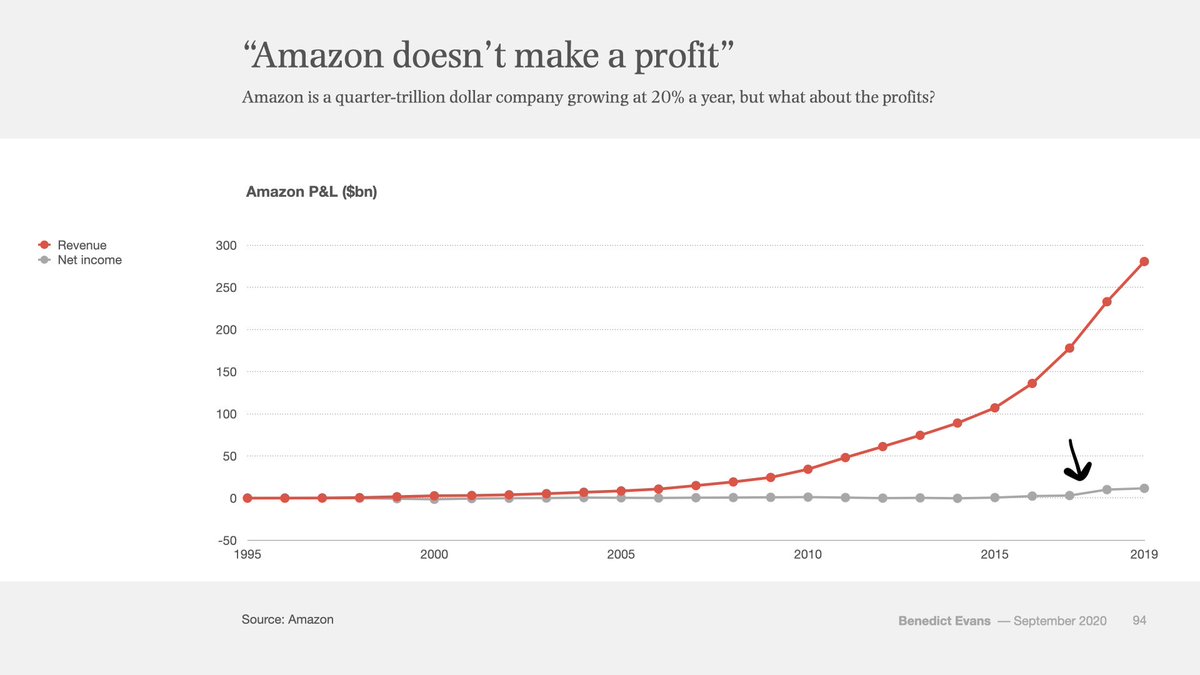

Study this chart.

This is Amazon’s P&L from 1995 to 2019. That’s 24 years. Red is revenue, gray is profit. You see that little blip on the end where the gray line goes up? That’s when, 22 years in, Amazon started actually making a profit.

Amazon was 22 years old when this little gray line of net income first peeled off of 0. Every single year before then, there were op eds and critics and short sellers claiming that Amazon was a ponzi scheme that would never make any money.

Ethereum just turned 10 years old. This is what the first 10 years of Amazon stock looked like:

10 years of chop. All along the way, Amazon was beset with doubters and non-believers. Is e-commerce a VC-subsidized charity? They’re selling underpriced cheap low-quality knick-knacks to bargain hunters, who cares? How are they ever going to make actual money, like Walmart or GE?

If you were arguing about Amazon’s P/E ratio, you were in the wrong regime. That’s the regime of linear growth. But e-commerce was not a linear trend, and so every single person for 22 years arguing about P/E ratios was devastatingly wrong. No matter what you paid, no matter when you bought, you were not bullish enough.

Because that’s what exponentials do. When it comes to truly exponential technologies, no matter how big you think it’s going to get, it just keeps getting even bigger.

This is the thing that Silicon Valley has always understood better than Wall Street. Silicon Valley was raised on exponentials, while Wall Street was raised on linearity. And over the last few years, crypto’s center of gravity has migrated from Silicon Valley to Wall Street. You can feel it.

Granted, crypto growth doesn’t look as smooth as e-commerce’s growth. It’s burstier, it goes in fits and starts. This is because crypto, being about money, is deeply tied to macro forces, and it also has more violent regulatory push and pull than e-commerce. Crypto strikes at the heart of the state—money—and so it’s more unnerving to governments than e-commerce ever was.

But the exponential is no less inevitable. It's a crude argument. But if crypto is exponential, then the crude argument is correct.

Zoom out.

Financial assets want to be free. They want to be open. They want to be interconnected. Crypto turns financial assets into file formats, makes it as easy to send a dollar or a stock as to send a PDF. Crypto makes it possible for everything to talk to everything. It makes it all 24/7, global, interconnected, and open.

That will win. Open always wins.

If there’s no other lesson I've learned from the Internet, it’s that. Incumbents will fight against it, governments will huff and puff, but eventually they will give up against the adoption, the generativeness, the sheer efficiency that this technology enables. It’s what the Internet did to every other industry. Blockchains are how that same trend will gobble up all of finance and money.

Yes—with enough time—all of it.

An old saying goes: people overestimate what can happen in two years, but they underestimate what can happen in ten.

If you believe in the exponential, if you zoom out enough, then it’s all still cheap. And it should humble you that every day, the holders outlast the sellers and naysayers. Big capital has a longer time horizon than CT swing traders might lead you to believe. Big capital has been trained through history not to fade big technologies. You know, the big gushy story that originally got you to buy $ETH or $SOL? Big capital believes that story and hasn't stopped.

So what exactly am I arguing?

I am arguing that applying P/E ratios to smart contract chains (the “revenue meta,” as it’s now called), is giving up on the exponential. It means you have consigned this industry to the regime of linear growth. It means you believe 30 million DAUs on-chain and <1% of M2 is it. Crypto is just one of the things in the world. A sideshow. It did not win. It was not inevitable.

More than anything, I’m arguing to be a believer. Not just a believer, but a long-term believer.

I’m arguing that this exponential will be bigger than anything else you’ve been a part of in your life. That this is your e-commerce. That you will look back when you’re old and tell your kids—I was there when it all happened. Not everyone believed it was possible, that whole societies could change, that all of money and finance would be transformed by programs running on decentralized computers that we collectively owned.

But it actually happened. It changed the world.

And you were a part of it.

Disclosure: These are my own views. Dragonfly is an investor in $MON, $MEGA, $ETH, $SOL, $HYPE, $SKY among many other tokens. Dragonfly believes in the exponential. This is not investment advice, but is advice of another kind.

English

@santiagoroel @hosseeb I feel like you're trying to predict the eventual black swan event originated from a tweet or something one person says or does. I think that's a very shortsighted vision comparing to the potential and growth we have ahead of us. Maybe there's a white swan coming 😊

English