@vkhosla Fake news! Waabi’s autonomous trucks aren’t here yet and still have a long way to go. They will be here when they can operate fully on the road and follow traffic rules without accidents.

English

Nelson Campos

1.6K posts

@NELS0NCC

Biografía en proceso desde 1994

Physical AI's moment is here and @Waabi_ai is leading the way Excited to share we have raised $1B USD of new capital to accelerate the commercial deployment of autonomous trucks and meaningfully expand to robotaxis! Partnering with Uber to deploy 25,000 or more Waabi Driver-powered robotaxis on the @Uber platform, substantially accelerating the adoption of robotaxis at scale. For the first time in the industry, we have created one shared brain to power the two largest self driving applications —trucks and robotaxis. This means any progress in one vertical directly improves the other. For example, our trucks, which have already mastered complex surface streets enabling an industry first direct-to-customer model, will be able to go all the way to urban centers as well. We have assembled a dream team of capital and strategic partners to accelerate our bold vision: this funding includes an oversubscribed $750M Series C round led by @khoslaventures and @G2VPLLC , as well as additional capital from @Uber tied to robotaxi development. Thank you to the incredible Waabi team and partners for making this all possible. This is a true inflection point and we’re looking forward to building the future of Physical AI, together.

The stock market always behaves the same way in one respect: when a stock is covered by various people, everyone jumps on it like sharks. The trick, however, is to recognize these gems years in advance, as I did with $ASTS, $RKLB, $SOFI, $QS, and many others in 2020/2021. Recognizing tomorrow's opportunities early has become my life's work, and today I'd like to introduce you to some stocks that could also become tenbaggers in a few years (of course, never guaranteed). A Multi Mega Thread. 🧵👇

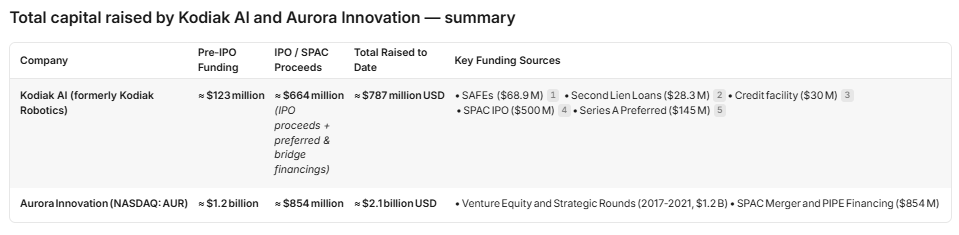

@AlexfromBabylon I have not done any DD on Kodiak yet, but why do you prefer this company over $AUR? They seem to be expanding rapidly, hitting key milestones and on the way to profitability as well. Any other reason besides the smaller marketcap and “owner mentality” from your previous post?

Some US visitors are seeing limited access to our website. • We are in the middle of a capital raising • Regulations restrict distribution of related materials in the US • The geoblock is a compliance requirement, not a lack of transparency We look forward to restoring full access once the process is complete.

$DTREF - last time they placed with institutions we ran from .14 to .46. I'll take that 300% move again all day.

$ASPI Renergen Acquisition Update Report sent to clients and substack. Breakdown on valuation updates, $100M Revenue path, and further outlook report now that the acquisition is complete. Closed earlier than the Jan. 30 deadline. Full Report: open.substack.com/pub/seqhcapita…

$PRME Nice to see gods technology back in the mid $3's but will be nicer when we're in the $30's :-)