Investors Compass@selvaprathee

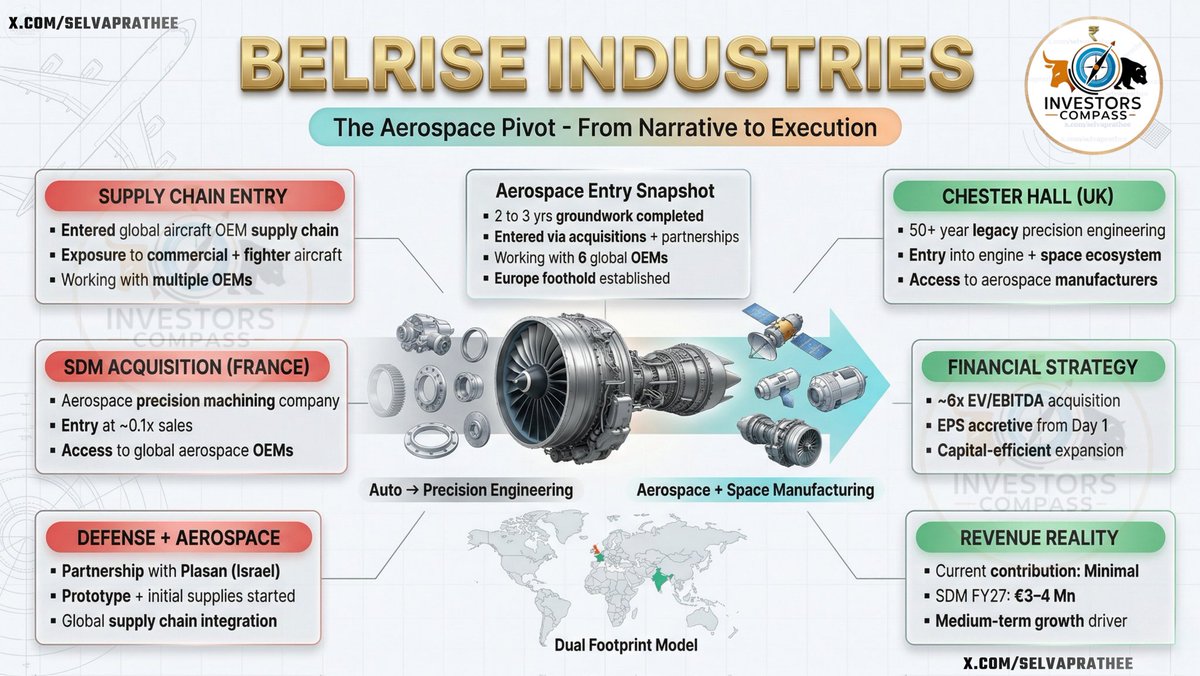

Belrise Industries – Structural Rerating Roadmap

- From a 2W component maker to a multi-segment system supplier,

- Belrise is engineering a structural rerating cycle built on execution, diversification, and capital efficiency

- Let’s decode the 4 year transformation playbook

1⃣ FY25 – Reset Phase: The Foundation

▪️FY25 focus – preparing for IPO-led deleveraging

▪️May 2025 – IPO proceeds used to repay ₹1,596 Cr debt

▪️Interest burden reduced, balance sheet deleveraged

▪️ROCE base built, financial flexibility restored

🗣️ "The IPO proceeds have strengthened our balance sheet, enabling us to fully repay ₹15,960 million debt in May 2025, giving us greater financial flexibility for future growth."

Impact:

✅ Debt-light foundation

✅ Cash flow strength

✅ Self-funded growth readiness

➡️ Belrise exits FY25 with a clean slate and growth runway.

2⃣ FY26 – Acceleration Phase: The Execution Year

▪️Q1 FY26 – Chennai facility commissioned (2W & CV OEMs)

▪️Q2 FY26 – Pune (M&HCV) & Bhiwadi (PV + 2W) to go live

▪️Exports scaled to 5.4%, luxury European OEM onboarded

▪️ Capex Plan: ₹800 Cr over FY26 - FY27

▪️2W content per vehicle rising from ₹12.5k → ₹17.3k

🗣️ "Chennai facility commenced supplies in Q1, and Pune and Bhiwadi will go live by Q2, driving our next growth phase."

Impact:

✅ Capacity expansion visibility

✅ Export diversification

✅ Value-added mix improvement

➡️ Belrise enters FY26 as an execution-led growth story

3⃣ FY27 – Diversification Phase: Broadening the Base

▪️Full-year benefit from 3 new plants

▪️M&HCV, 4W, defense segments scaling up

▪️H-One utilization >60% → operating leverage unlock

▪️ROCE trajectory improving toward high-teens

🗣️ "We expect significant revenue growth from FY27 as all new facilities contribute fully and utilization improves beyond 60%."

Impact:

✅ ₹400-₹500 Cr incremental turnover

✅ Diversified revenue mix

✅ ROCE uplift from operating leverage

➡️ FY27 becomes the scale & efficiency phase

4⃣ FY28 – Rerating Phase: Recognition & Repricing

▪️Revenue mix rebalanced – 2W share down, CV/4W/Exports up

▪️System supplier model entrenched (Tier 0.5)

▪️Sustained 12%+ EBITDA margin with double-digit growth

▪️Stronger OEM integration & export base

🗣️ "We are transitioning from a Tier-1 component supplier to a Tier-0.5 system supplier, which will strengthen margins and OEM partnerships."

Impact:

✅ Diversified, stable earnings

✅ Margin consistency

✅ Valuation multiple expansion

➡️ FY28 marks Belrise’s structural rerating as a compounder

🧭 Investor Compass View:

Belrise is building a rerating flywheel –

FY25: Reset foundation

FY26: Execute expansion

FY27: Diversify scale

FY28: Deliver rerating

➡️ A debt-light, execution-driven, multi-segment system supplier poised for FY26-28 valuation uplift

No Buy/Sell Recommendation

#StocksInFocus #StocksInFocus #Belrise