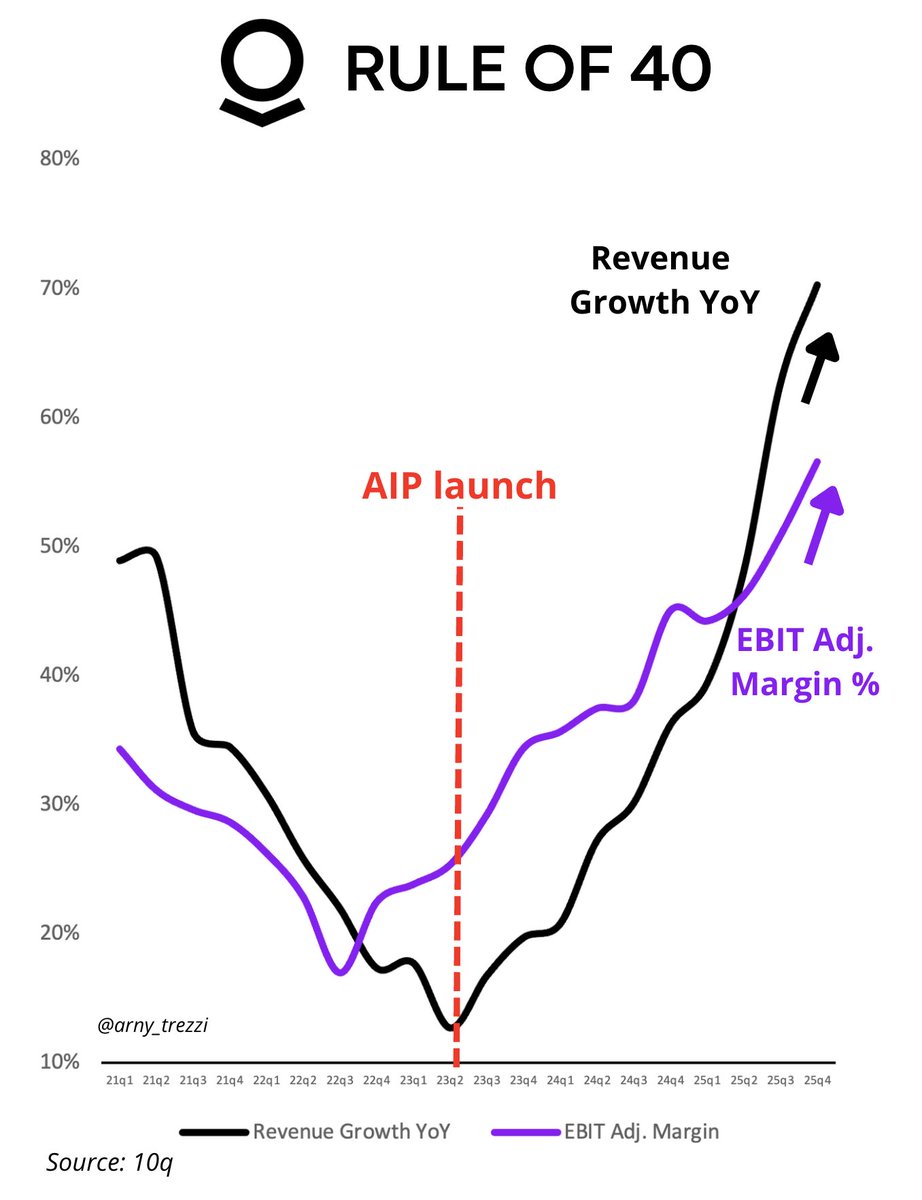

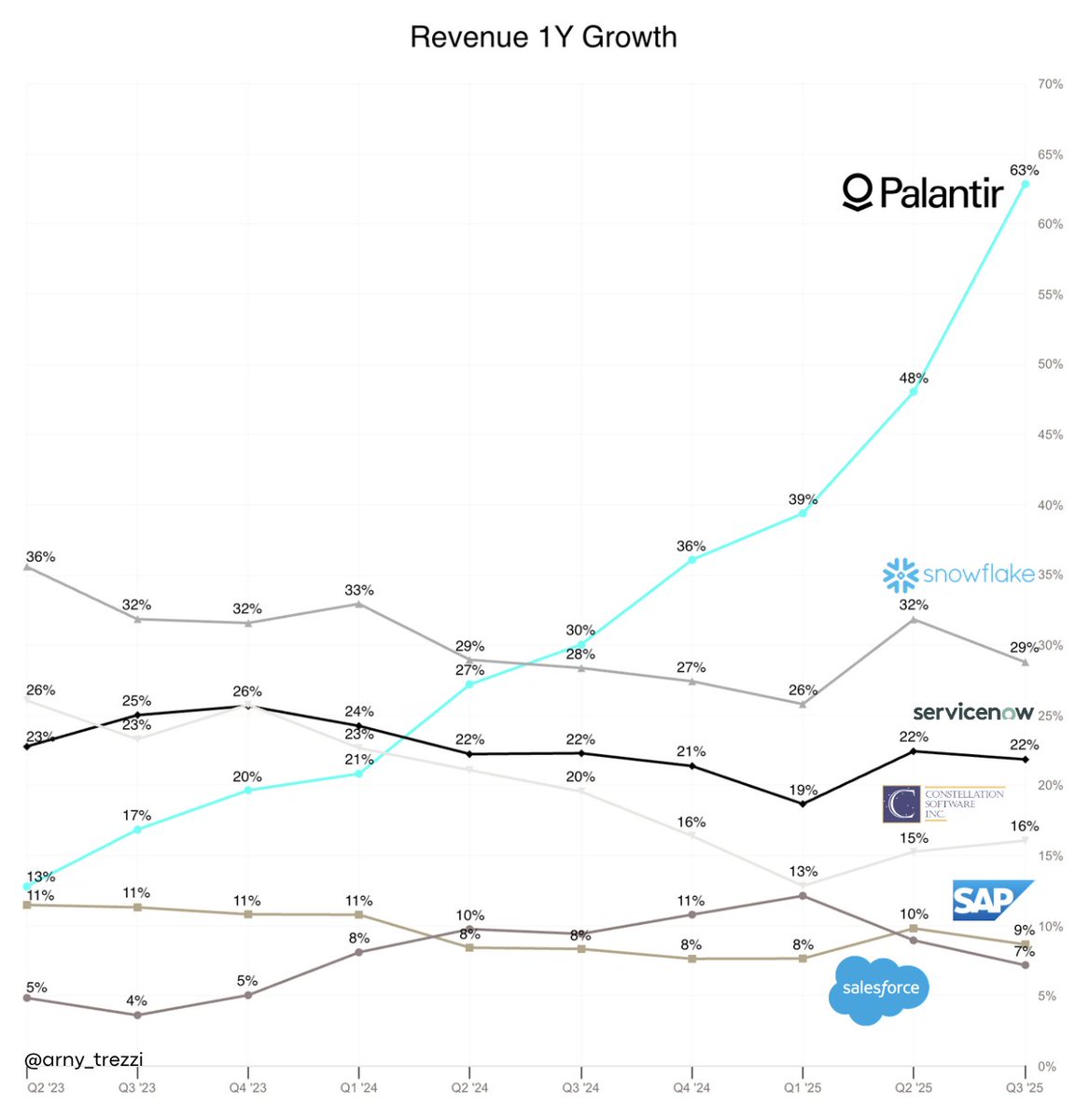

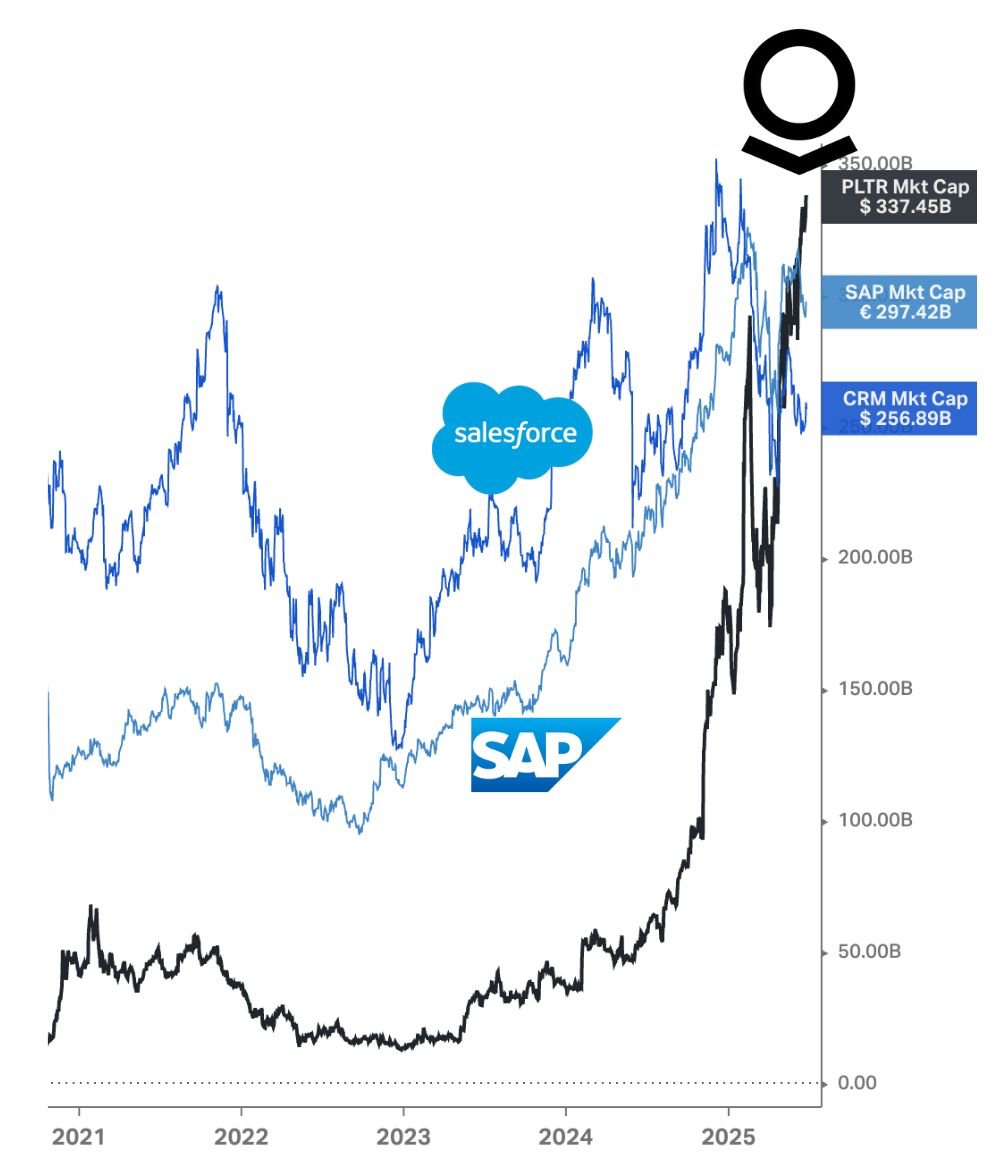

$PLTR I just read @michaeljburry's new short report. This is BURRYSH1T. +10,000 words. Here are the 10 worst takes: 1. "Palantir’s margins are not even SaaS-level, but when Palantir’s functionality succumbs to the commoditization of AI coding tools, they will fall further." 2. "The result is a Net Dollar Retention surge from 107% to 139%. 139 is extraordinary. It is also suspect. Such heights are rarely sustained and almost always associated with base effects. 3. "Not enough bandwidth? That sounds exactly like a consultancy. Not enough integration engineers, not enough Palantir people to customize the installations." 4. "So, after the company lost $4bn in almost 20 years as a private company, it has continued to give tons of stock to employees while losing money on bubble SPACs and growing to a remarkably petite $4.5bn revenue for 2025 – petite for being the U.S. government’s pet data enforcer AND an AI FOMO/Lucky Strike poster child." 5. "[Selling Gotham] was not too hard. Government software was terrible, and hence, low-hanging fruit. It took 3y, but after that, low hanging fruit." 6. "Foundry was produced in 8 weeks, AIP in a few weeks. Foundry is an integration layer for thin apps that require extensive customization. AIP is simply a wrapper. Putting the cost of its fleet of FDEs in R&D pumps up R&D artificially." 7. "Palantir moved to 'bootcamps' – short demos in lieu of full FDE deployments – as a way to onboard Foundry AIP customers faster and improve margins. As these boot camps are rehearsed scenarios built on curated data, for ease of use, they can fail in real life scenarios that vary from the curated ones." 8. "Palantir creates architectural overhead in a system, and now that LLMs are integrated into this overhead, the coming commoditization of LLMs should render Palantir a user interface provider of little value. 9. "Let’s spend some time on those money-losing years onas it was a very long time for a company full of supposed geniuses to not make any money." 10. "Calling his engineering consultants 'forward deployed' fit right into his desired noble, militaristic vibe. A righteous and right company." ------------------------------ I lost 10 QI points while reading the entire report, so you don't have to. Here are a few personal thoughts: 1. The report seems entirely written by GPT. 2. ~20% of the report is focused on how the company was at DPO in 2020. We are in 2026 😉 3. Doubts on the validity of the software are dismantled by customers themselves: • Airbus, client since 2015, just got a ~$1bn 10y expansion • Hyundai HD, client since 2021, just got a "hundreds of millions" expansion • $200mn Lumen expansion • $440mn deal with the US Navy to provide Ship OS; Are these clients nuts? 😆 4. Burry wildly misunderstand the Palantir's AI thesis. Burry just sees AI = LLM , but there is much more than that. Palantir doesn't build an AI model. Palantir bets that as LLMs converge toward commoditization, value will increasingly shift to the model-orchestration layer to deliver outcomes: call it AIP. The 20 years of building software in the most critical use cases put Palantir in a prime position to capitalize on this. 5. Burry wildly misunderstands Palantir's financials, as he believes growth and margins will decrease. Operating leverage + network effects = sustained growth with expanding margins 6. Trying to prove US Commercial is a scam by showing International Commerce does't grow is dumb. Palantir voluntarily pivoted the entire company on the success of US Commercial, the most important market, while it saw the Int market was not ready to capture the AI wave. US Commercial: +137% YoY Revenue Growth +145% YoY Remaining Deal Value +49 % clients 7. Seeing the low number of clients as a minus is dumb. The fact that Palantir has been able to generate ~$4bn with ~1,000 clients shows an abnormal earnings potential vs its similar size "competitors": • Databricks (17,000 clients), • Snowflake (12,000 clients), 8. Many concerns have dismantled infinite times: • "consultancy" • "SPACs" • "SBC" They are not concerns now. 9. Dilution is simply not an issue any longer. The truth is in the Earnings Per Share: • 8x YoY • 43% GAAP Margin. PLTR is diluting by 2% while growing revenue by ~70% at 57% EBIT adj margin. As an investor, I am only happy if we get only 2% dilution to get these results. 10. His $46 valuation uses dumb inputs: • 16% WACC is crazy. PLTR is no longer a money-burning startup. • 4% dilution vs 2% actual dilution • 50% growth for 5 years and 25% after: this is not that negative, but inferior to what the strength of the company can achieve. 11. Burrito is proving himself to be a bad influencer more than an investor. If he had properly analysed the situation (he could subscribe to @PalantirBullets for free), he could have focused on discussing valid points. Essentially, he wanted to short and asked GPT to help him draft the thesis, leveraging his "influencer status." If he wanted to provide a reasonable short report, he would have provided evidence like: • big customers churning; • product failing to deliver; • serious evidence of corporate misconduct. Why hasn't he done this? There is simply no ground. There was once an investor. Now there is only a substack grifter. Yours, @arny_trezzi