Teldar Paper

1.3K posts

Teldar Paper

@Paperboy2009

The two most common elements in the universe are hydrogen, and stupidity

NYC Katılım Mart 2009

1K Takip Edilen238 Takipçiler

@danprimack Hop-on / hop-off bus tours are a great way to see / get around the city while learning about the history

English

Taking 15 year-old daughter to Paris next month. Any and all ideas for fun activities (not an art museum kid)...

English

@HulkCapitalPro If you didnt see it, they upped the buyback by anoither $200MM, through financing with Blue Owl

English

@LogicalThesis Great rib cap, aka-best part of the whole side of beef

English

@BDC_Analyst I suspect a miracle cure will be coming for all of the $LQDA LT holders afflicted shortly.

(disclosure: I've been saying this for months)

English

$LQDA - Sad to announce that I have been diagnosed with a severe case of LDS. Liquidia Derangement Syndrome. Unfortunately, the doctors have told me it's terminal.

If you are a fellow LQDA shareholder, please get a check up asap, you're at an elevated risk if you've been holding it for over a year.

English

@3PeaksTrading I don't know what else they can do to get the mojo back into the stock. They're certainly outperforming, and not being rewarded for it $NVDA

English

Boost the tiny dividend and maybe a special divy would be cool

*Walter Bloomberg@DeItaone

$NVDA - NVIDIA: PLANNING TO USE 50% OF FREE CASH FOR INVESTOR RETURNS

English

@Mr_Derivatives G-d forbid they work on getting rid of the spam / bots. That would certainly be worthy of a tease like that

English

@unemon1 👀

He would certainly know what’s coming down the pike…

English

@HulkCapitalPro The will probably raise some cash soon. Current cash through Q1 2027 $CTMX

English

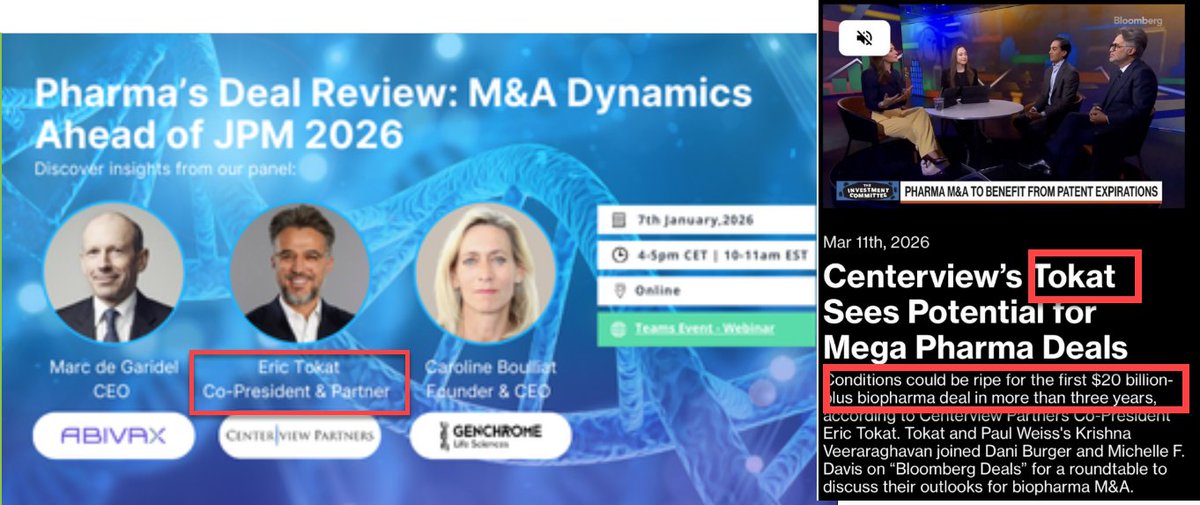

@princetongb @hannibalspeaks This process has been leaking more than a sieve. Lock things down and bring it across the finish line already! $ABVX

English

My interpretation from the $ABVX LaLettre is that they have details wrong -> all interested parties have exclusive access to the data room. My guess is that $AZN went for a follow-up visit reserving the calendar date, as may have others on different dates. There is likely a French iBanker staffer responsible for the leaks with a connection to the publication.

English

@Paperboy2009 @semodough Why is there such high volume on that ? Weird .

English

$TGTX not that anyone cares today- but believe anecdotal nuggets out there on Azer-cel is performing very well - heard from last call enrollment exceeding trial sites - now even better details - would be game changer for PPMS which affects 10-15 %of MS patients

dough@semodough

$TGTX nice to hear these 2 updates here Present preliminary Phase 1 azer-cel data in Progressive MS in the second half of 2026 ENROLLMENT is exceeding trial sites 👍 •Announce pivotal topline data for subcutaneous BRIUMVI (ublituximab) year-end SUBq could double peak estimates for $THTX

English

@seedy19tron @adamfeuerstein What ends first? The forever wait for the $LQDA decision, or the $ABVX drama and their back and forth battle with LaLettre?

English

Back to biotech so this is what the $abvx IR guy said in an email

“Abivax denies report in La Lettre that it has granted AstraZeneca exclusive access to confidential information until March 23 with a view to formalizing an offer, according to emailed statement from company’s head of investor relations.”

Wait what if the exclusivity is March 24th? Why the incredibly careful wording? They could’ve said no talks or reports of a sale are false. Just the very specific nature of denying the wording is very sus.

I just want this whirlwind to end. Buyout or no buyout. MDG announce a CCO or something.

English

Teldar Paper retweetledi

Teldar Paper retweetledi

Barclays reiterated Top Idea $BBIO Overweight; $157

$PFE $ALNY

Barclays said in its note—On Tuesday 3/10, the judge in the PFE (covered by Emily Field) US tafamidis IP trial issued a memorandum opinion denying the ANDA filers' motion to exclude PFE expert testimony.

We note from our prior work on taf IP, including a legal expert call (link) that the admissibility of PFE's expert testimony was flagged as a key swing factor in the case; the outcome now appears to be in PFE's favor in allowing the testimony (both Matzger's curve fitting & Raman mapping analyses).

We reiterate BBIO as a top idea and see the rare disease franchise alone as supporting upside, but we also view Attruby as a better drug than tafamidis and think this should lessen the impact around a generic taf vs investor concerns.

• Based on our legal expert call, our base case is we see a settlement and a Vyndamax generic in the ~'32-33 time frame in the US, and Vyndaqel generic late '28 in the US. For exUS, we note tafamidis EU ODE until Feb '30 in WT ATTR-CM; for Vyndamax, we see EP '406 polymorph patent (expires Aug '35) as currently not contested (for now), we note EP '993 polymorph patent oral opposition proceedings 3/12...

For BBIO shares, taf IP is a key question we get from investors ahead of the April trial - we see meaningful upside for BBIO on a potential settlement.

quantumup@Quantumup1

Raymond James⬆️ $BBIO's PT to $89 from $85, reiterated Outperform and said, Infigratinib efficacy comes in competitive with/slightly ahead of the CNP class. Infigratinib met its primary endpoint at Week 52, demonstrating an LS mean difference in annualized height velocity (AHV) vs. placebo of +1.74 cm/yr (p<0.0001); with all the caveats of cross-trial comparison, this comes in slightly ahead of the bar set by CNPs in Phase 3 (~+1.5 cm/yr vs. pbo), notably in a population with a slightly higher baseline AHV than CNP comps. The trial also achieved statistical significance on CFB in height Z-score (LS mean +0.32 SD vs. pbo, p<0.0001). Encouragingly, infigratinib showed favorable trends on proportionality in the full trial population (LS mean -0.02 vs. pbo, p =. 1849; similar to CNP data); a pre-specified exploratory subgroup analysis including children <8 y.o was stat-sig on proportionality. Taken together, we view these results as establishing a very competitive efficacy profile with CNPs (perhaps slightly ahead), though we expect debate will persist on the meaningfulness of AHV differentiation vs. the CNP class (particularly should CNP + HGH combo reach market, offering substantial incremental potential on catch-up growth). • Topline safety looks relatively clean; ACH regulatory filings planned for 2H 2026. Safety was in focus for PROPEL, with pre-data concerns around selectivity profile (FGFR1-3i); today's results provide some incremental comfort on this front, in our view: BBIO reported no d/cs related to AEs (total trial d/c rate was not disclosed), no observed AEs characteristic of FGFR1/2 inhibition (e.g. ocular), and 3 cases of mild, transient, asymptomatic hyperphosphatemia (a ~4% rate, lower than BBIO's self-set 10% bar). Encouraging to our eyes, longitudinal serum phosphate data suggest phos levels ~similar to placebo (or at most only slightly elevated) across the treatment period. With positive Phase 3 results in-hand, BBIO plans to submit regulatory filings (FDA and EMA) for infigratinib in ACH during 2H 2026; a detailed scientific presentation is also expected this year. • Increasing our target to $89 on Phase 3 de-risking. We increase our infigratinib program PoS from 65% to 90% on today's positive Phase 3 results, maintaining our long-term ~$1B peak sales estimate for infigratinib in ACH. We note longer-term approval in hypochondroplasia (a population potentially as large as ACH, with perhaps greater intent-to-treat in the U.S., in our view) represents upside to our model (not yet explicitly included). As a result of these updates, our target increases to $89. We reiterate Outperform.

English

No sellers today on $LQDA. Slow and steady rise on lower than avg volume

English

Pretty good vol on the March 27th exp 42 calls on $LQDA. Ppl expecting a decision this month, which would still be overdue

English

@cosmokramer313 @g_bhatia @jfais20 Is that typically 180 days from trial date or the post-trial briefing?

English

$LQDA- continuation, coiled spring ahead of judge decision vs $UTHR

English