ParaFi Capital retweetledi

ParaFi Capital

321 posts

ParaFi Capital

@paraficapital

Alternative asset management and technology firm that operates liquid and venture strategies focused on the digital asset ecosystem. https://t.co/VTCozTZoPu

Katılım Mayıs 2019

1 Takip Edilen44.4K Takipçiler

View the interactive chart and see other ParaFi Signals as well as important disclosures at parafi.com/signals.

English

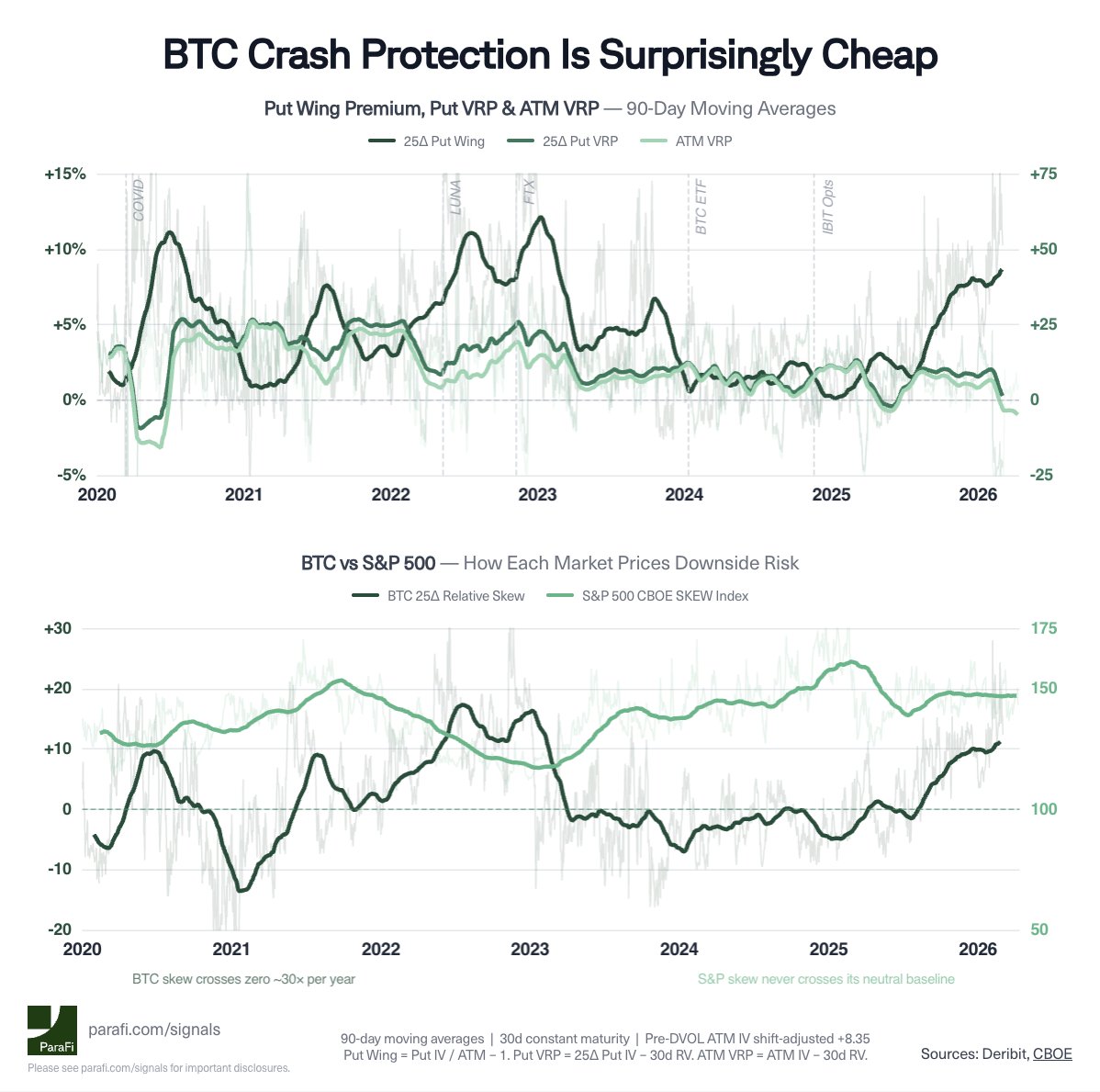

Why does BTC's crash protection appear cheap?

Despite multiple 50-80% drawdowns since 2020, BTC's 25-delta put wing, a standard measure of crash insurance cost, has averaged just ~5% above at-the-money (ATM) implied volatility (IV). On ~11% of all days, the premium disappears entirely. In 2024, that figure reached 29%.

One possible driver is persistent vol selling. Out-of-the-money (OTM) puts carry the richest IV on the surface, and Chart 1 shows that the 25δ put's vol risk premium consistently exceeds the ATM vol risk premium. That extra carry attracts systematic sellers, increasingly tied to ETF-related flows, whose supply compresses the put wing even as tail risk remains.

For context, Chart 2 shows S&P 500 crash protection virtually never gets this cheap, while BTC's skew crosses zero ~30 times per year.

From such low starting levels, it can be theorized that a major drawdown could trigger a meaningful repricing.

English

ParaFi Capital retweetledi

Last month, together with @ParaFiCapital, we hosted our first official institutional dinner in NYC. @MorganStanley, Apollo, @jump_ , Pantera , @Polymarket , @FalconXGlobal, @0xfluid, @PayPal and 40+ in the room.

What struck me was how much the conversation has evolved. It's no longer about whether onchain finance is real. The question now is which platform becomes the operating layer for global capital flows.

Many still know @JupiterExchange as a DEX aggregator. What we are building is much broader, a full-stack onchain superapp for trading, lending, payments and tokenized assets at scale. We hope the evening offered a broader perspective where Jupiter and onchain finance markets are heading

It is only the beginning.

English

View the interactive chart and see other ParaFi Signals as well as important disclosures at parafi.com/signals.

English

Is Bitcoin just a high-beta stock?

Generally, crypto's idiosyncratic returns are poorly explained by factor models. However, understanding investment factors can help construct risk-adjusted portfolios.

For example, Bitcoin's daily returns over the last year, proxied by the $IBIT spot Bitcoin ETF, show a sticky median correlation of +0.55 with the Beta style factor, suggesting that Bitcoin behaves like a high-beta stock more than any other factor.

More telling, however, is the Excess Beta factor. In July 2025, the Excess Beta style factor coincided with Bitcoin's jump from $99K to $120K, uniquely capturing a leverage-fueled short squeeze amid 2025 DAT euphoria that the Beta factor alone did not explain.

The takeaway? These observations suggest that Beta and Excess Beta may be useful historical factor lenses for distinguishing between periods when Bitcoin behaves more like a broad-market beta-correlated asset and periods when Bitcoin is more influenced by short covering, leverage, and momentum chasing.

English

View the interactive chart and see other ParaFi Signals at parafi.com/signals

English

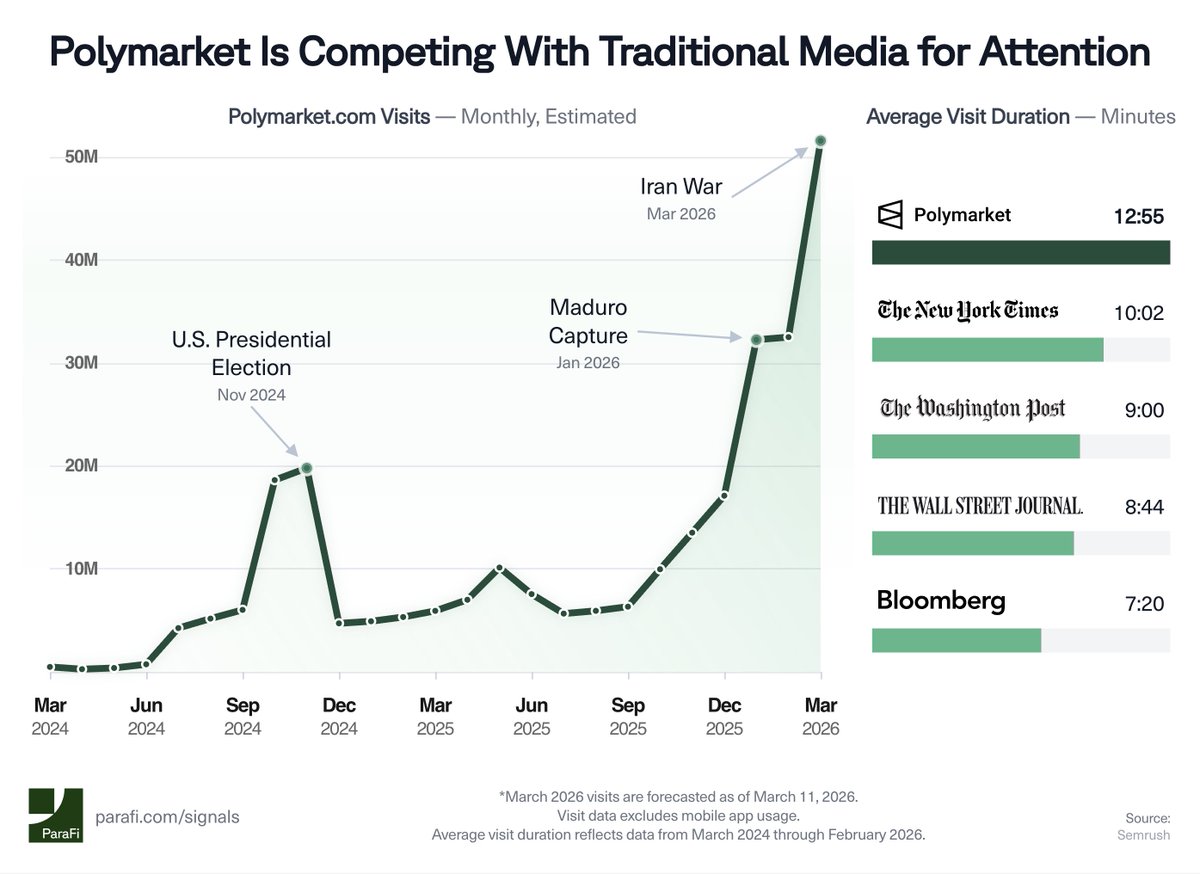

@Polymarket is increasingly competing with traditional media as a destination for real-time information.

Monthly website visits suggest a much broader audience using prediction markets to gauge major political and geopolitical developments. Visits are on track to exceed 50 million in March 2026, roughly 2.5x the levels seen during the 2024 U.S. presidential election. Users spend nearly 13 minutes per visit on average, longer than sessions on several major media sites including New York Times, Washington Post, Wall Street Journal, and Bloomberg.

English

View the interactive chart and see other ParaFi Signals at parafi.com/signals

English

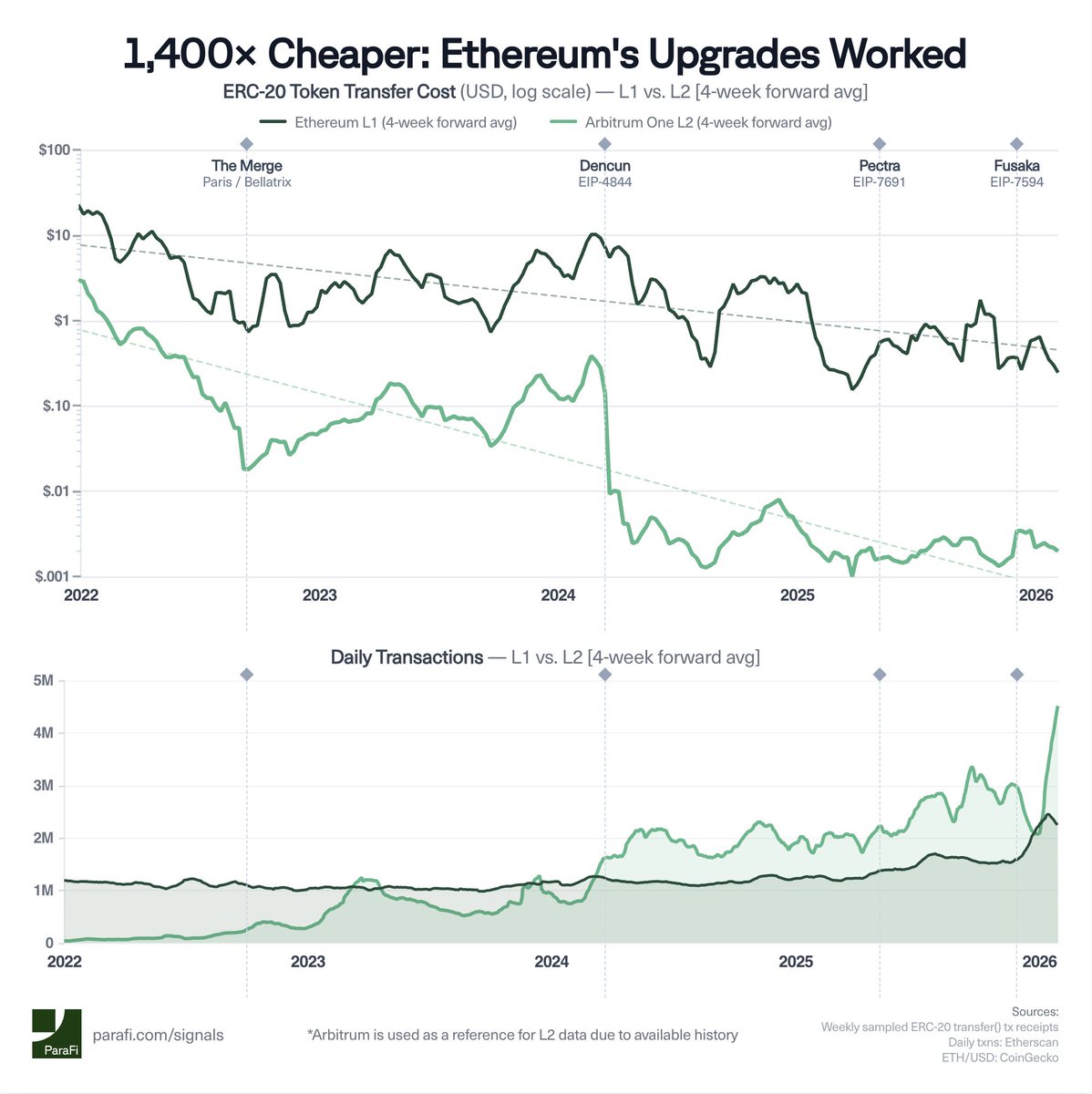

Amid ongoing debate about Ethereum's roadmap and the role of L2s, the rollup-centric model has materially reduced execution costs while expanding throughput.

L2 fees have collapsed. As of January 2026, a standard transfer on @Arbitrum costs ~$0.002 — down over 1,400x from 2022. Dencun (Mar '24) was the structural inflection, compressing L2 fees ~94% in subsequent months.

L1 fees have also declined. A USDC transfer on Ethereum mainnet now runs ~$0.25, with Fusaka (Dec '25) increasing gas limits and reaccelerating L1 activity (+47% in daily transactions post-upgrade).

Sub-cent fees on L2s unlock use cases that were previously uneconomical: micropayments via x402 protocol, day-to-day stablecoin payments, and AI agents transacting on behalf of users at machine speed.

English

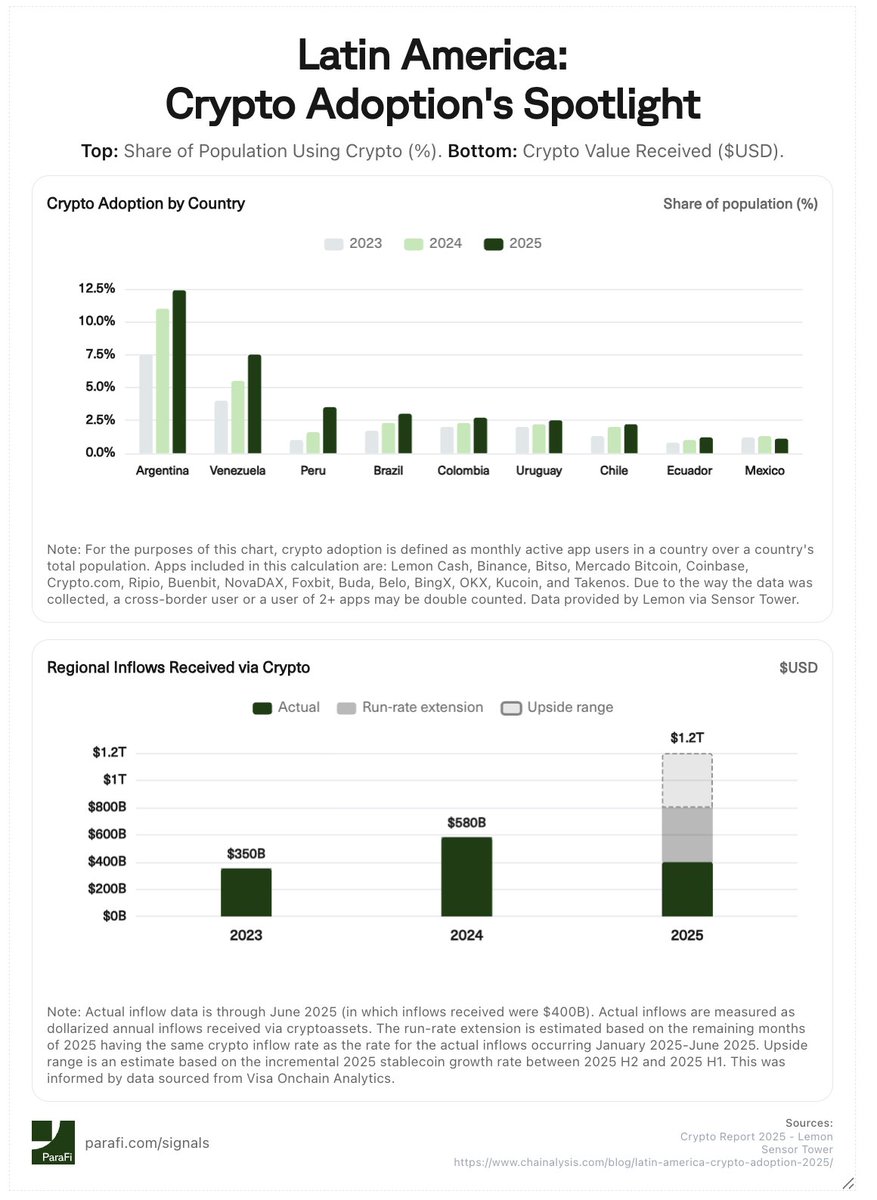

Latin America is one of the fastest growing regions for mainstream crypto adoption. Stablecoins lie at the center, establishing a low cost and accessible financial layer for USD savings, remittances, and payments. Regional crypto inflows are approximated at $800B-$1.2T in 2025 (+38-107% YoY).

Mobile-first fintech leaders such as @lemonapp_ar (5M+ accounts), Félix Pago (40k+ payout locations), and @MercadoBitcoin (4M+ accounts) are driving mainstream usage across key markets. In Argentina alone, 12.5% of the population is now interacting with crypto.

See more at ParaFi Signals (parafi.com/signals).

English

ParaFi Capital retweetledi

Birch Hill raises $2.5 million pre-seed round led by ParaFi Capital and Castle Island Ventures for institutional onchain credit infrastructure theblock.co/post/389399/bi…

English

Tokenized gold had a record year in adoption: supply grew +155% YoY and holders grew +65% YoY.

Nearly 700k oz of gold were newly tokenized across PAXG and XAUt, lifting total on-chain supply to 1.15M oz — about ~0.016% of above-ground gold — and market cap to $5.4B (+332% YoY), demonstrating demand for blockchain-native gold exposure beyond speculative price action and signaling a broader trend of hard-assets moving on-chain.

See more at ParaFi Signals (parafi.com/signals).

English

ParaFi Capital retweetledi

BREAKING:

Jupiter secures a $35M strategic investment into $JUP from ParaFi Capital to accelerate onchain financial infrastructure.

This deal - which will be settled entirely in $JupUSD - was closed at spot price with ParaFi committing to an extended token lockup.

English

ParaFi Capital retweetledi

2/ Led by @BainCapCrypto and Distributed Global, with participation from @HaunVentures, Brevan Howard Digital, @galaxyhq, Sentinel Global, @Bullish, @hypersphere_, @flowdesk_co, and Intersection, plus existing investors @1kxnetwork, @paraficapital, and @RoadCapMgmt.

English

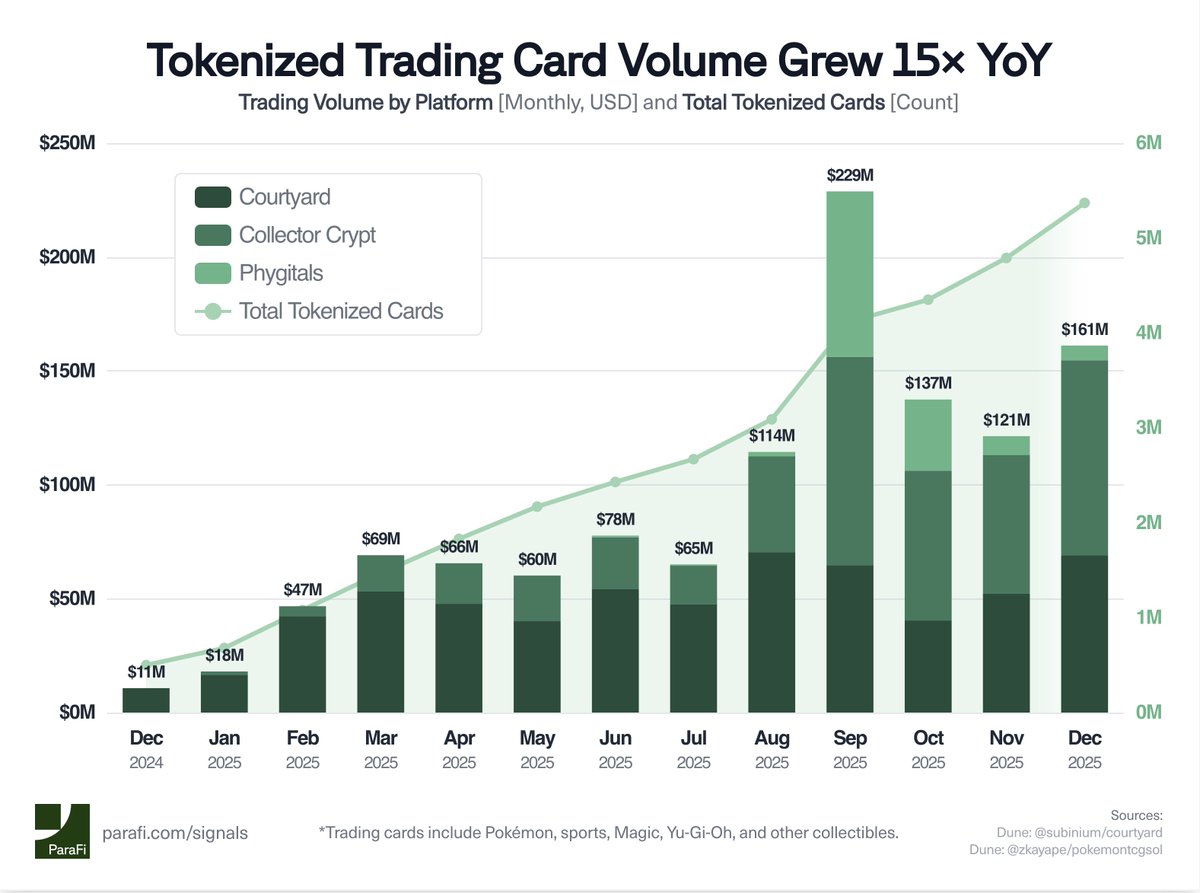

We're excited to launch ParaFi Signals, a recurring series of bite-sized insights on trends shaping digital assets.

Today's insight, courtesy of @JonoBSB:

Monthly trading card volume increased ~15x YoY in 2025 as tokenized Pokémon and sports cards gained mainstream traction across platforms like @Courtyard_io, @Collector_Crypt, and @Phygitals.

Today, over 5M cards are tokenized and traded on chain

English

ParaFi Capital retweetledi

Today we released the beta for Ample, a new savings protocol we built at Layer3.

Ample is inspired by the UK’s Premium Bond system and rebuilt using onchain financial infrastructure. Users deposit supported assets, retain full ownership of principal, and the yield generated across all deposits is pooled to fund recurring, randomized payouts. In each period, a small number of participants receive outsized outcomes, funded by the same underlying yield that would otherwise be distributed evenly.

As I’ve written about before, there are several structural reasons why I believe this product is well timed.

For most of the post-2008 period, savings products built around pooled yield faced a core limitation of insufficient and unstable yield. In low-rate environments, it was difficult to fund meaningful upside without introducing leverage, principal risk, or opaque balance sheet mechanics. Today, onchain money markets now provide consistent, programmatic yield that can sustainably support payout mechanisms at scale.

Distribution has also changed. Historically, premium bond-style savings products were constrained by local deposit bases and national banking systems. Today, stablecoins and USD balances held in fintech wallets function as a global, dollar-denominated liability layer. This allows a protocol like Ample to aggregate deposits and yield across partners and geographies, enabling payout pools and expected outcomes that no single institution could realistically offer on its own.

Transparency was another historical limitation. Prior attempts relied on opaque payout logic that was difficult for users, and often regulators, to verify. With smart contracts and verifiable randomness, payout rules can now be codified onchain. Users can see exactly how yield is accrued, how payouts are calculated, and how the payout budget is allocated. The system is auditable by design.

The underlying infrastructure has matured as well. The onchain stack today looks materially different than it did in previous cycles. Smart wallets abstract away key management and gas complexity. Layer 2 networks have reduced settlement costs. On and off ramps have expanded to the point where users can move between local currency and stablecoins with minimal friction. Taken together, this creates a UX environment where an onchain savings product can operate with the same, or better, usability as a traditional fintech application.

From a user behavior perspective, the appeal of this type of savings structure is well established. Humans consistently prefer variable outcomes over fixed yield, even when the expected return is identical. This preference has driven adoption of regulated savings products globally, including in the United States and the United Kingdom, where Premium Bonds alone represent approximately $150 billion in deposits. The mechanism works because it changes how yield is experienced, not how it is generated.

From an integrator perspective, this savings model offers a way to increase asset retention without increasing risk. Assets remain deposited longer because the experience is more engaging than static APY. Ample turns this structure into a reusable primitive. If successful, wallets, exchanges, and fintechs should be able to offer this savings model for idle assets such as USDC, BTC, ETH, SOL, and tokenized equities. Over time, a meaningful share of onchain yield could route through pooled savings structures rather than traditional yield products.

The beta release is focused on validating a small number of variables: initial asset selection, user behavior and retention, payout cadence, partner integration surfaces, and jurisdictional posture. Ample takes a small fee on yield before payouts are distributed. Ample is built entirely within Layer3, and any protocol revenue generated flows directly to the L3 treasury.

The beta is intentionally limited in scope. The objective is to test whether the structural assumptions outlined above translate into real usage and durable behavior. If they do, Ample becomes less of a consumer-facing application and more a financial primitive that others embed.

Follow along @AmpleHQ

English

ParaFi Capital retweetledi

With the cornerstone of finance shifting to stablecoins and cryptoassets, Lemon is tackling a generational opportunity to reimagine and modernize consumer financial services in LatAm.

Lemon Argentina@lemonapp_ar

Levantamos una Serie B de 20 millones de dólares para seguir acercando crypto a millones de personas en América Latina. Hoy somos la aplicación crypto con más usuarios activos en Argentina y en Perú.

English

ParaFi Capital retweetledi

@joshsolesbury, Investor at ParaFi Capital, explores how stablecoins drive fintech adoption, use cases, and value creation.

English

ParaFi Capital retweetledi

AgriFORCE Growing Systems (AGRI) announced today its plans to raise ~$550M to establish the first NASDAQ-listed company with a dedicated AVAX strategy. To bootstrap its AVAX accumulation strategy, AGRI will use a portion of the cash proceeds raised to purchase locked AVAX from the Avalanche Foundation. Purchased tokens are subject to a long-term lock-up schedule that permits staking and other uses.

The cash proceeds received by the Foundation will be strategically deployed to support ecosystem growth, including investments in RWAs, purchases of AVAX and AVAX DAT shares. The Avalanche Foundation remains committed to using its treasury to advance adoption and long-term sustainability.

English