Sabitlenmiş Tweet

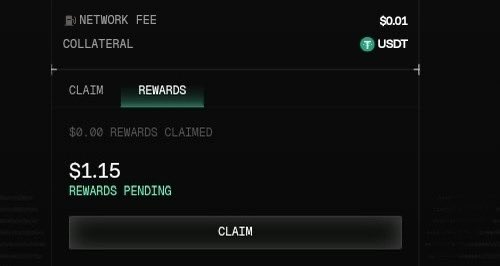

Wrapped up strong with @alturax Epoch 0 & 1 steady rewards, no stress.

Now Epoch 3 is LIVE 🚀

Same strategy, bigger upside. Consistency = higher potential earnings over time.

Don’t fade this one.

English

Proverbs Wisdom

383 posts

@PathofProverbs

Let Wisdom guide you One Proverb at a time

Where Does the Next $1T of Crypto Value Come From? As the market matures, the focus shifts to real-world adoption. Where will the next wave of value be created? Featuring: @GregoryLBell (@hashgraph) @renapshah (@StacksEndowment) @alturax (@AurelliusEth) @ivanmiskovic (@QuantumFDN) Moderated by David Micley (@wintermute_t) May 6 | The Bass, Miami Beach Secure your spot: innovate.thetie.io/tickets-miami

$1M TVL on @arbitrum. The programmable economy is expanding access to non-directional strategies on stablecoins. Altura keeps it transparent and secure 🦉

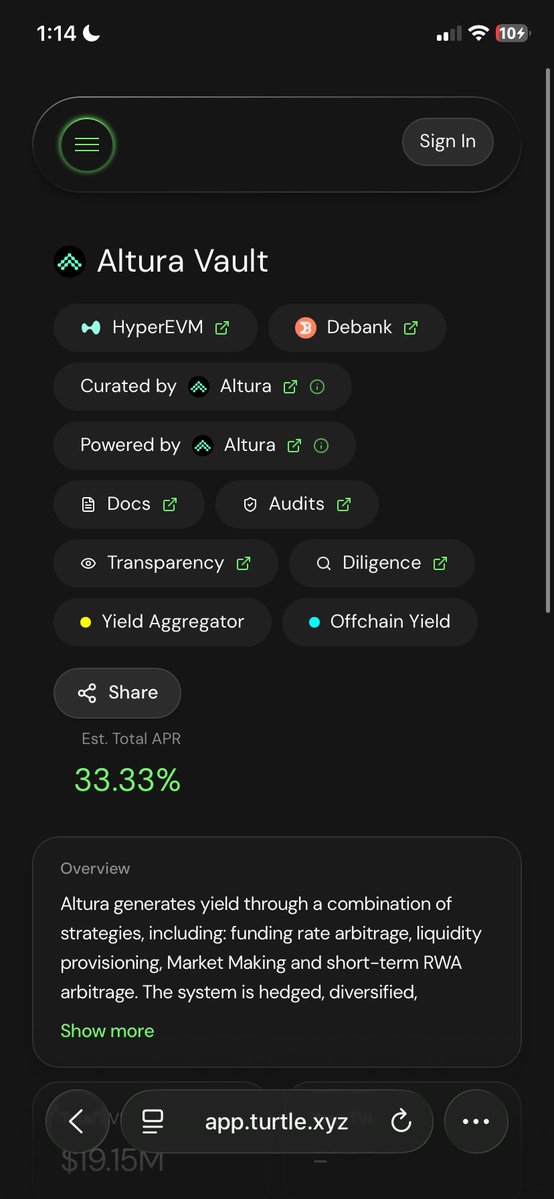

Introducing, Strategies by Altura 🦉 Track our vault's performance data and capital allocation across protocol reserves, institutional custody and yield-generating strategies. Experience transparency by design. Now live on app.altura.trade

The Altura Vault has crossed $15M AUM. Smart money is consolidating around verifiable yield backed by unbeatable incentives on a protocol where globally insured deposits and real-time security are the minimum standard. Money just works better here 🦉

As a precautionary step, we’re temporarily disabling multi-chain functionality until USDT0 OFT bridging is fully restored and deemed stable. USDT0 remains fully backed 1:1 by USDT. Altura has zero exposure to rsETH. we’re prioritizing system integrity by pausing cross-chain flows at the infrastructure layer.

We're rolling out another $500K in ALTU rewards on @merkl_xyz, starting on April 30. Simply hold AVLT to qualify. Rewards from ongoing opportunities roll over, and all current vault depositors will remain eligible with no further action required.

Recent events like the exploit involving Kelp DAO are another reminder of a hard truth in DeFi. Risk management needs to develop in lockstep with financial innovation. For a long time, this industry has operated on the assumption that smart contract risk is something users simply accept in exchange for yield. Repeated exploits have made it clear that this approach can't scale DeFi beyond a niche audience. Capital preservation needs to become a core design principle, not an afterthought. Removing risk entirely is not realistic. The real question is how well the industry can absorb shock events. One of the most practical ways to address this is through insurance. Whether built into protocols or offered as an optional layer, users should have the ability to protect their capital against smart contract failures, oracle issues, and counterparty risk. Insurance does come at a cost. But it is foundational, so that cost should be treated the same way traditional finance treats custody, compliance, and risk controls. It's also important for insurance providers to improve how they assess risk. Protocol ratings should play a much bigger role in underwriting. Not all DeFi protocols carry the same level of risk, but coverage today often fails to reflect that. A more transparent and risk-based pricing model would benefit both users and insurers through improved capital allocation across the ecosystem. Users deserve peace of mind when trusting protocols with their capital. As builders, we have a responsibility to provide commensurate levels of opportunity and protection. The fate of DeFi may very well hinge on yield mechanisms that build on stronger foundations. Insurance is one of them.

Recent events like the exploit involving Kelp DAO are another reminder of a hard truth in DeFi. Risk management needs to develop in lockstep with financial innovation. For a long time, this industry has operated on the assumption that smart contract risk is something users simply accept in exchange for yield. Repeated exploits have made it clear that this approach can't scale DeFi beyond a niche audience. Capital preservation needs to become a core design principle, not an afterthought. Removing risk entirely is not realistic. The real question is how well the industry can absorb shock events. One of the most practical ways to address this is through insurance. Whether built into protocols or offered as an optional layer, users should have the ability to protect their capital against smart contract failures, oracle issues, and counterparty risk. Insurance does come at a cost. But it is foundational, so that cost should be treated the same way traditional finance treats custody, compliance, and risk controls. It's also important for insurance providers to improve how they assess risk. Protocol ratings should play a much bigger role in underwriting. Not all DeFi protocols carry the same level of risk, but coverage today often fails to reflect that. A more transparent and risk-based pricing model would benefit both users and insurers through improved capital allocation across the ecosystem. Users deserve peace of mind when trusting protocols with their capital. As builders, we have a responsibility to provide commensurate levels of opportunity and protection. The fate of DeFi may very well hinge on yield mechanisms that build on stronger foundations. Insurance is one of them.

Real yield is back onchain. @alturax delivers returns through market-neutral strategies and RWA trading. → Deposit into the Altura vault. → Hold for 30 days. → Earn Altura's native APY + a share of a $9,000 bonus rewards pool. app.layer3.xyz/campaigns/disc…

As a precautionary measure, we have temporarily paused the USDT0 OFT bridging infrastructure while the rsETH incident is being investigated. We want to be clear that USDT0 has no exposure, and all USDT0 tokens remain fully backed 1:1 by USDT. We'll share updates as more information becomes available.