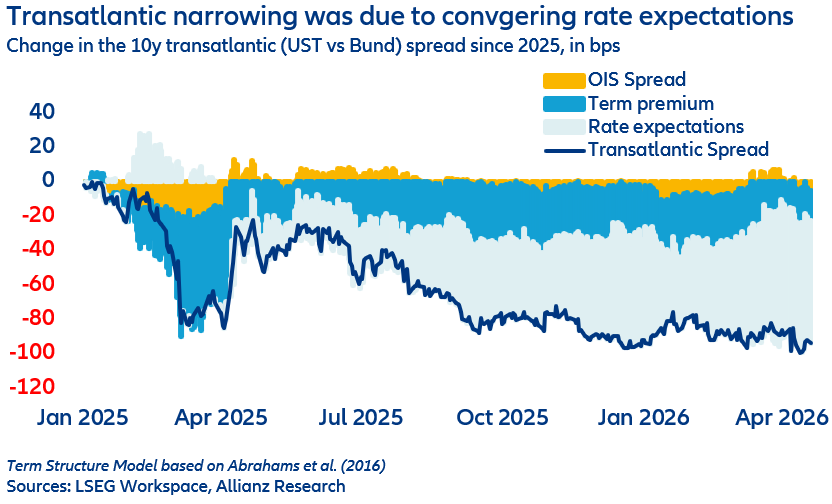

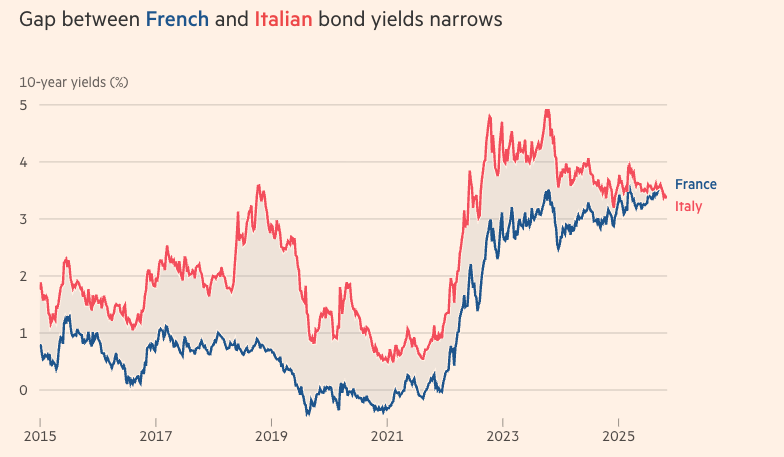

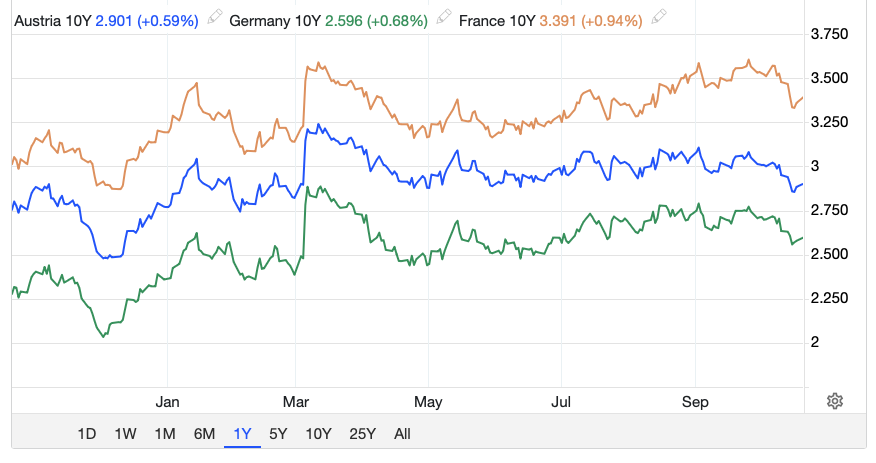

Recent #bond sell-off wasn't only about repricing of expected rates, it was also especially at the long end a repricing of risk (term premium). One forgotten driver of the term premium is the #duration reflux from run-off central bank #QE holdings. since 2022 the #ECB has lifted the 10y term premium by 80bps, the Fed by 35bps. Current #FED purchases are limited to Bills and di not extract duration, the run-off effects persist. For more: lnkd.in/dQKQd2-w

English