PSB

20.4K posts

@Lfc_samie It was Stoke City. Last game of the season when we unfortunately got battered 6-1

English

@AnfieldSector Bringing up Diogo’s death is the most spineless thing ever! Kobe Bryant a NBA & Lakers Legend passed away mid season in 2020 and LeBron & Anthony Davis and the whole team used that as motivation to go and win the championship for Kobe & his family!

English

[🟢] NEW: As things stand, FSG believe there is mitigation for performances: the death of Diogo Jota principle among that, given its effect on his team-mates at the start of the season. There has also been the fall-off in performance of the stars of the era, primarily last season’s top goalscorer Mohamed Salah.

While Slot is acknowledged to have made errors, the feeling is that he deserves four transfer windows before a judgment is made.

[@SamWallaceTel]

English

@EdFrosty500 Great job! Smashing it - next target for you is £15k followed by £20k

English

@HappyPunch @playbookboxing Hes bang on here John Fury. Either Shane McGuigan, Jonathan Banks (Emanuel’s real training protégé) or Dominic Ingle should be training Tyson. Don’t rate sugar hill at all. Tyson was done back in 2022. After Ngannou he should have called it or swerved Usyk. Big up John Fury

English

John Fury got emotional and said his relationship with Tyson Fury is completely destroyed 😳

“That’s hurt me like you wouldn’t believe. I don’t need you. I don’t need him and his millions. I need nothing off him.”

(via @playbookboxing)

English

@amitisinvesting Believe it or not weirdly i think and it feels like crypto has actually bottomed and is starting to slowly grind higher. I cant believe im actually saying that

English

Markets are in such a weird space currently right now.

Every single day there are two types of headlines: one that implies the war will end soon and oil prices should go down and then one that implies the exact opposite.

CPI was okay this week but if oil, which is now at $96, continues to stay here…inflation just isn’t going to get better.

Which means we aren’t going to easily get rate cuts. We now only have 1 cut projected for 2026.

The S&P is officially down 3% YTD and this week has lost that crucial $6700 level.

Individual sectors like Fintech and SaaS have just been completely left as narratives have ruined those names, whether it’s about AI or private credit.

However, individual growth stocks have meaningfully corrected from the highs. Some down 50%. Mag 7 multiples ex Tesla/Apple continue to be reasonable and every time they breakout…some headline brings them down, which is what we saw with $META.

I think this year so far has been characterized in 3 ways:

1. Finding a deeply important sector/theme and going heavy into that like drones/space/energy/etc, but timing is important as even those sectors have seen big pullbacks.

2. Accepting this year is consolidation (which is better than bearish) and just buying your favorite names at discounts every week to add to the portfolio.

3. Yielding volatility by running covered calls and playing ranges within stocks as many continue to be within a range which helps when running calls, something that has been one of my core strategies this year and is also what I thought might happen as we are in year 4 of the bull market and these names might just need to consolidate.

Going net short has not really worked unless you picked the right stocks, S&P down 3% isn’t really the best environment for shorting since everyone is so positioned for the crash that the premiums on puts/borrowing fees aren’t as attractive when everyone expects a major move down.

A hard market to navigate but still opportunity exists within it…

English

@TrendSpider @grok is this bullish or bearish for the stock and is this an indication that the bottom is in?

English

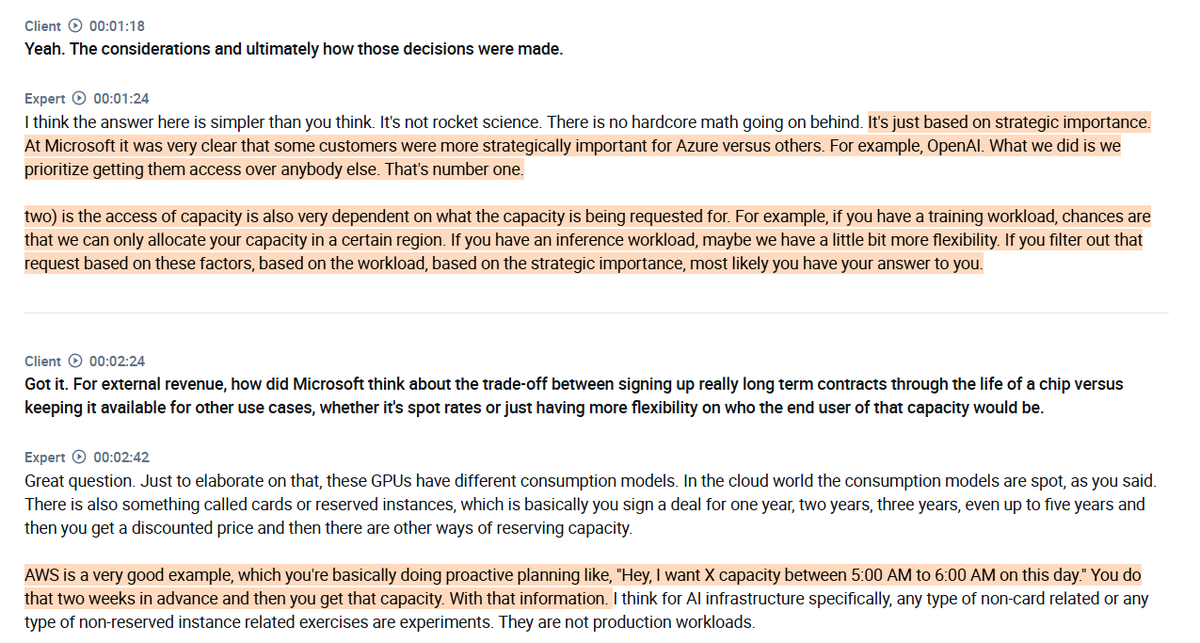

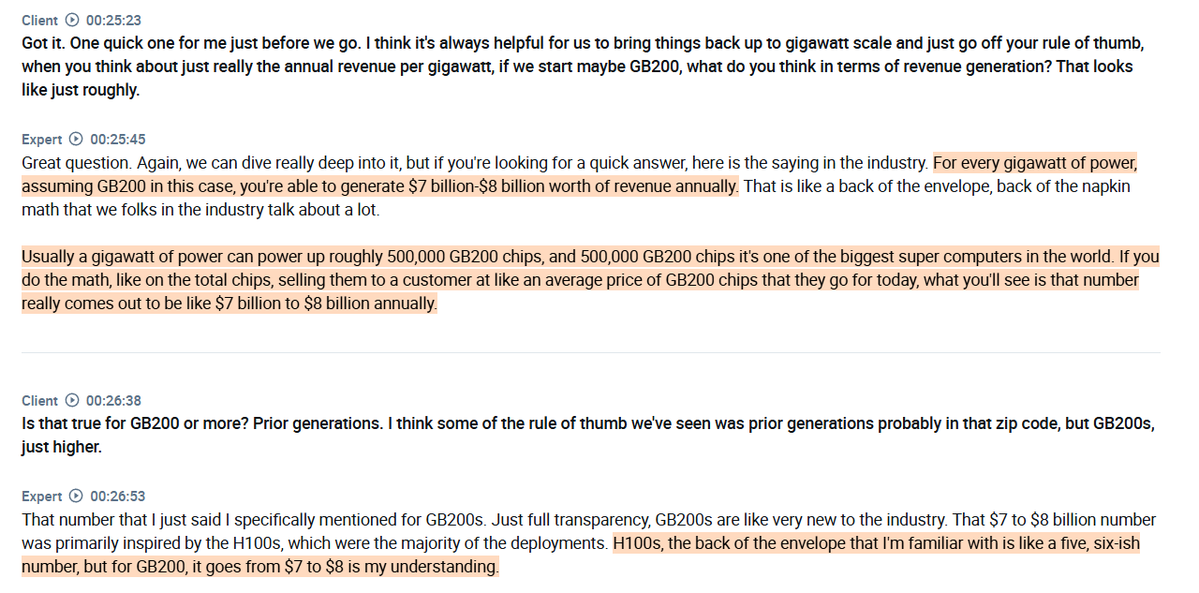

A very insightful conversation with a former $MSFT employee on cloud AI margins, GPU depreciation cycles, and the cloud economics in the AI era:

1. The expert highlights two key factors before discussing how $MSFT approaches ROIC targets in customer contracting conversations. First, GPU depreciation cycles have extended dramatically, from an initial estimate of 3 years all the way to 5, and later 8 or 9 years for certain chips. This means the original ROIC analysis has become significantly more favorable over time because the asset is lasting much longer than originally planned.

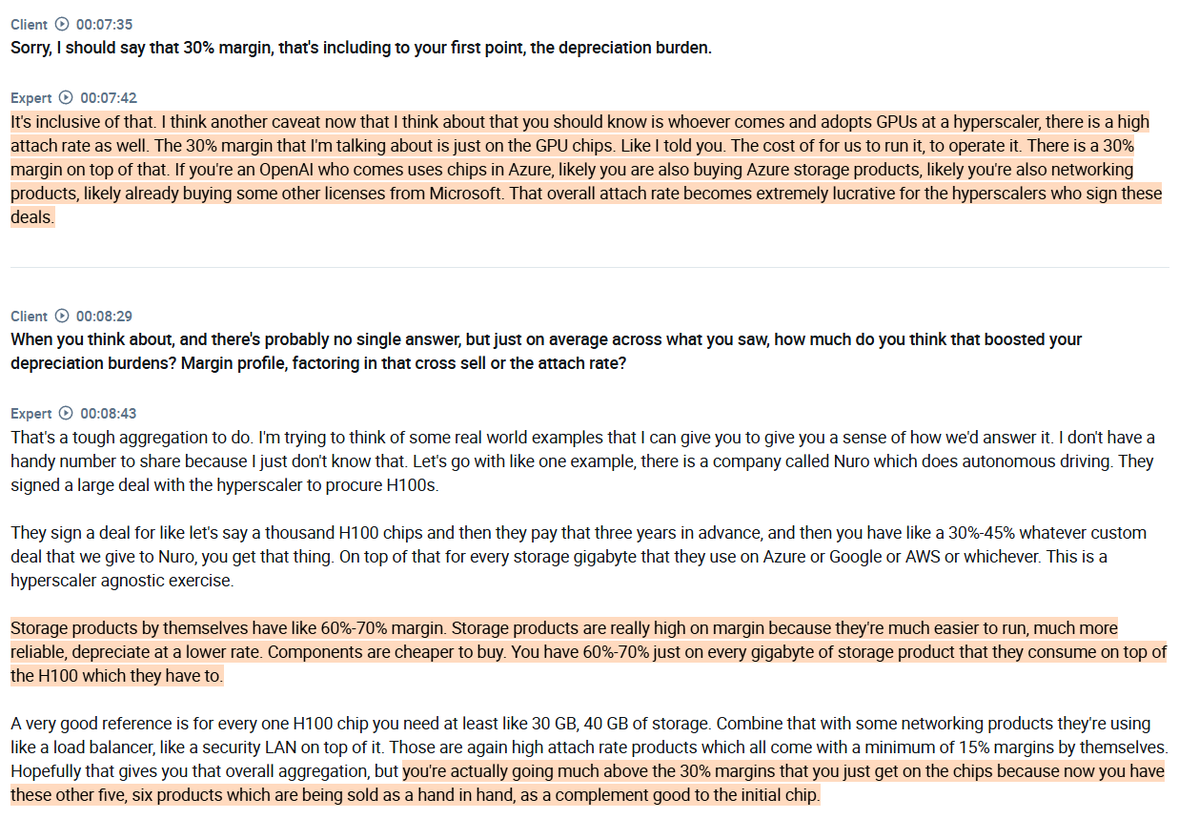

2. Second, strategic customers all operate on custom pricing deals, with those decisions made at the very top of the organization. The baseline approach is to use OpEx as the floor, with a minimum 30% margin built on top. He explains that this essentially covers the cost of capital on the original GPU investment, including depreciation.

3. The expert emphasizes that the V100 is the best real-world example of how depreciation cycles actually play out. That chip is nearly a decade old and still running at full utilization across many hyperscaler environments today, despite originally being depreciated over three years. Hyperscalers simply paid $NVDA to extend the warranty and kept generating margins from hardware that was already fully depreciated on paper.

4. Newer chips like the H100 and GB200 are a different story entirely, running at sustained high utilization around the clock, thermally constrained, and essentially impossible to repair, making replacement the only option when something fails. $NVDA has extended warranty terms for hyperscalers on H100-class systems, effectively taking on reliability risk and covering replacement costs.

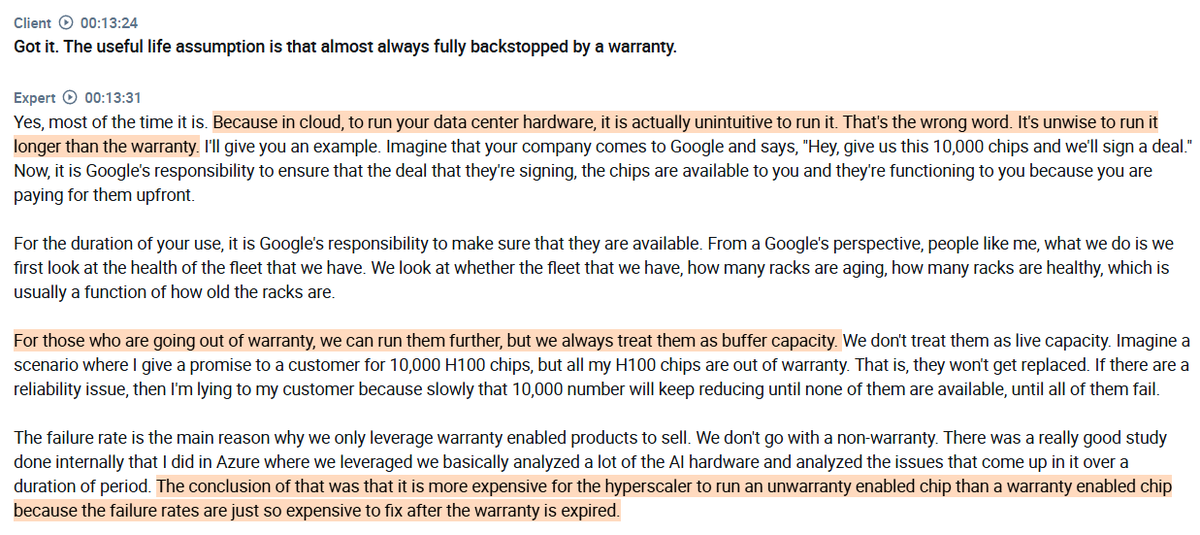

5. He is clear that running chips beyond their warranty is actually more expensive than staying within it, since failure rates without replacement coverage slowly erode customer commitments, which is why out-of-warranty chips are treated as buffer capacity rather than live capacity.

6. On the CapEx side, he estimates it costs roughly $30 to $35 billion dollars to stand up a gigawatt scale data center from scratch. Of that, around 80% goes toward IT infrastructure, primarily GPUs, CPUs, and memory, with the remaining 20% covering the physical shell and power setup. To put the GPU cost in perspective, each GB200 node costs around $60,000, with ten nodes stacked to form one rack at $600,000, and some hyperscalers go even higher. Given that everything in the supply chain remains constrained, he expects that overall CapEx figure to climb by another 5% or so from current levels.

found on @AlphaSenseInc

English

@StockMKTNewz @grok which us listed energy or utility company will benefit from this?

English

These companies will reportedly commit to building, buying, or bringing their own power supply for new AI data centers

Amazon $AMZN

Google $GOOGL

Meta Platforms $META

Microsoft $MSFT

xAI

Oracle $ORCL

OpenAI

WOLF@WOLF_Financial

BREAKING: Amazon, Google, Meta, Microsoft, xAI, Oracle, and OpenAI will head to the White House on March 4 to sign Trump's "Rate Payer Protection Pledge," as per Fox News. The companies will commit to building, buying, or bringing their own power supply for new AI data centers, ensuring American electricity bills don't rise with demand.

English

I bought a new stock today that’s been on my watchlist since September last year.

• Crucial in the AI data center buildout

• Revenue growth >115%

• FCF positive

• $1B net cash

• Stock is down 50% from its 52 week high

Any guesses which one it could be?

English

@wealthmatica And guess what? After all of this there shares outstanding will increase by 0.1% after 5 Years. You will just be diluted

English

At $200/share...

Amazon is so attractive in my opinion:

- Expanding AWS margins

- Accelerating AWS revenues

- AWS CEO said: "Supply sold out"

- Robotic arsenal under development

- Leo Constellation internet launch in 2026

- Trainium AI chips are a +10B business growing at 150% QoQ...

How are you bearish on a company like this long term?

$AMZN

Qualtrim@qualtrim

Amazon was the most accumulated Super Investor stock of last quarter, Q4 2025. Now at it's cheapest EV/EBITDA in 10 years. $AMZN

English

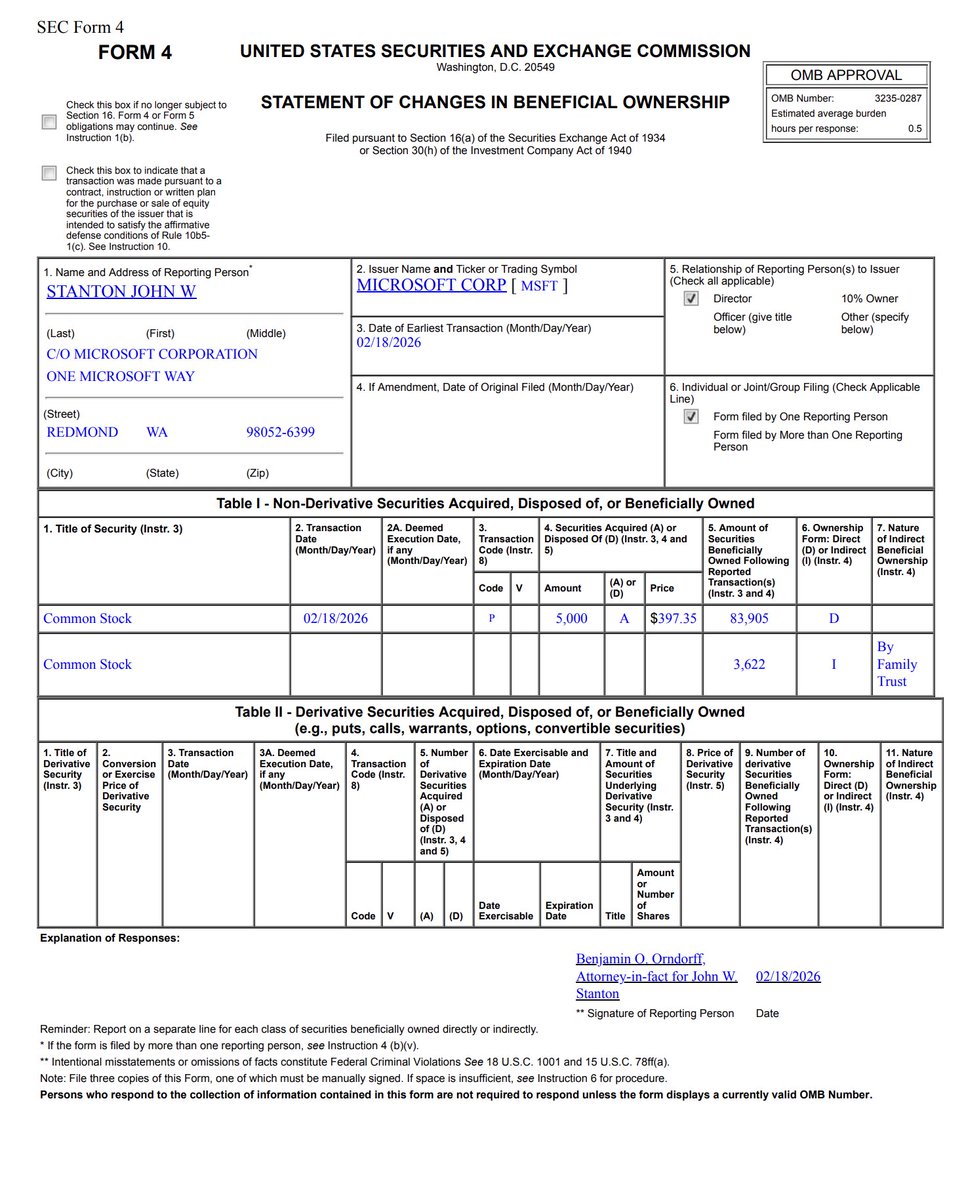

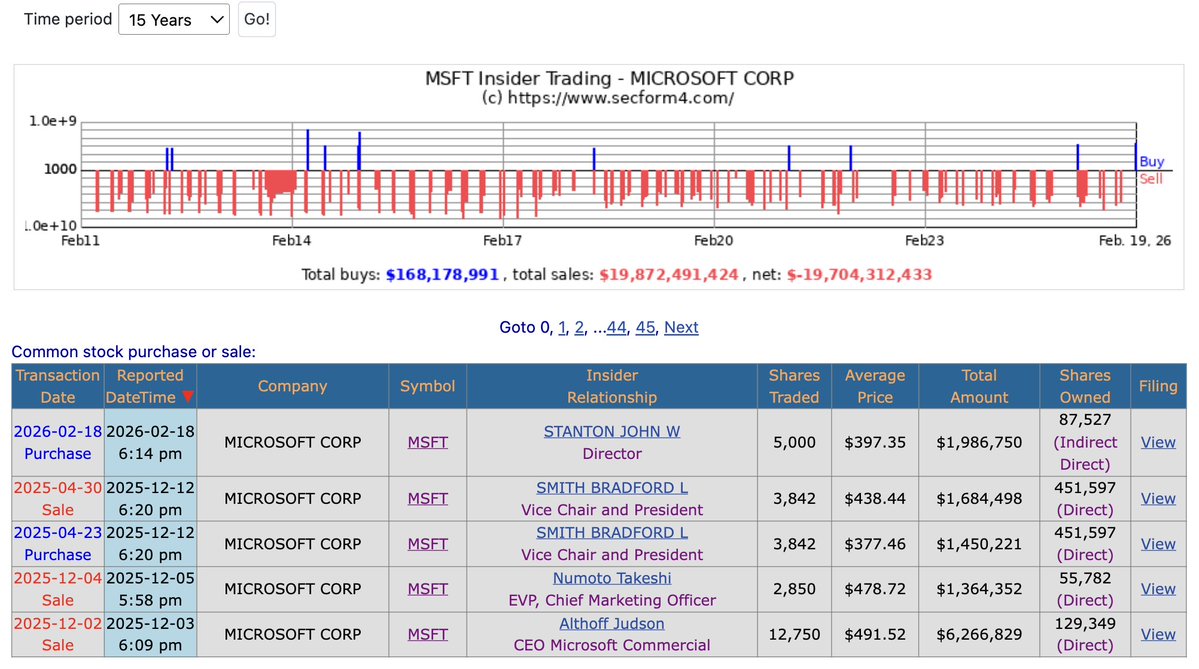

$MSFT Director John Stanton buys $1.98 million of shares, marking the largest insider buy in 11 years.

Microsoft is down by 15% YTD.

English

@LiebermanAustin There shares outstanding will increase by 0.1% in that time. You will be diluted

English

Prediction:

$AMZN is going to go on a generational run from 2026 - 2030 as the market realizes it’s one of the most defensible businesses in the world.

Price right now $200.

Check back in 4 years.

English

@amitisinvesting There’s only one stock that actually works in this environment and that is Visa. They materially benefit from AI and AI benefits its moat it doesn’t erode it.

English

last thursday, we had a similar decline to what we are seeing today...but it was for really no reason

then we recovered massively on friday

one week later, today, we are once again seeing new lows from last week for what it feels like is no major headline

amazing companies getting sold off on great earnings

utilities, defensives, industrials leading the way

$VZ is up 20% this year, last time it did that? 2006

choppiness isn't even the word...this market is moody, emotional, thinks AI is dead one day then thinks AI will destroy every industry the next...just a hard environment to navigate but the winners of the past few years are simply getting destroyed regardless of good earnings

the major reason I can point to, i think, is capex spend is so large that big tech will see negative FCF and that is leading to a rotation out of not only big tech but also high-beta growth, many sectors (space, quantum, nuclear) all now down YTD compared to January

ugly environment

English

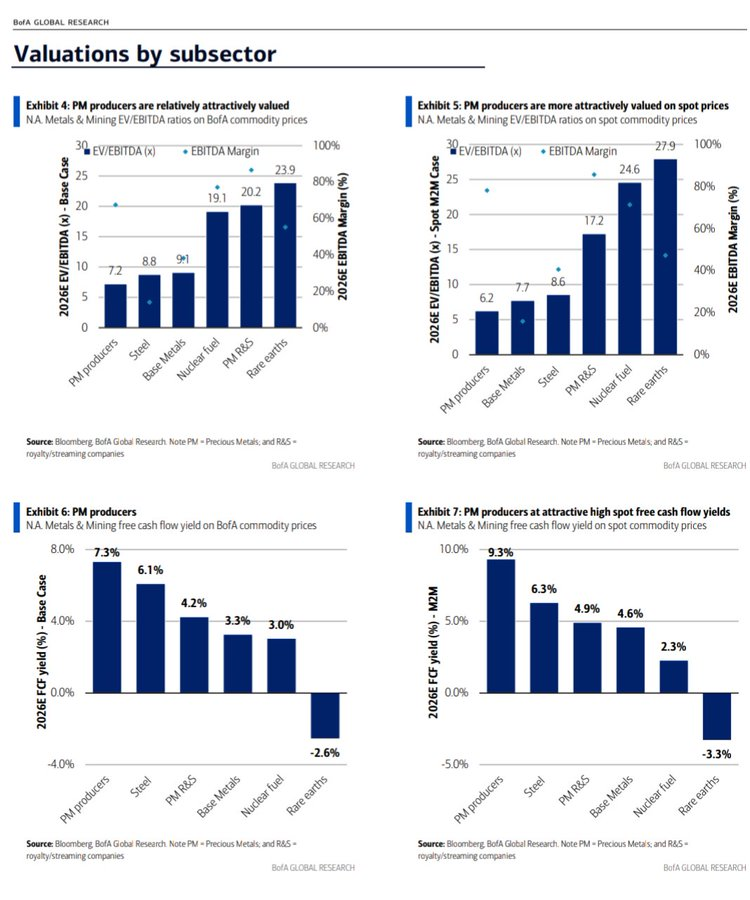

Bank of America: PM miners are the cheapest commodity sector

- Lowest EV/EBITDA

- Highest FCF yield

Despite higher metal prices, valuations have not rerated.

At current prices, precious metal miners are printing cash.

That disconnect sets the stage for earnings surprises.

English

@SteadyCompound @mastersinvest @grok what are the stocks in his portfolio that match his description?

English

Sir Chris Hohn:

- 18% over 2 decades

- Holds ~15 stocks

- Top 10 positions between 8% to 13%

- Focuses on: competitive forces, multiple layered barriers to entry, long time horizon, businesses with pricing power

Good piece by @mastersinvest

MastersInvest.com@mastersinvest

“Ultimately, the quality of the business trumps everything.” - Chris Hohn mastersinvest.com/newblog/2026/1…

English

PSB retweetledi

The Muslim Council of Britain has stated that certain findings from our rape gang inquiry are Islamophobic.

This may have worked before to shut down debate. It will not work now.

We are going to continue our inquiry, and we are going to continue telling the truth.

English