Phillip Lauterbach

94 posts

Phillip Lauterbach

@PhilLaut

CPA. Details matter. Transactionally focused helping families, small companies & real estate owners/operators. 3 kids 1 wife

Katılım Nisan 2021

529 Takip Edilen42 Takipçiler

I like to post about things that you'd never learn unless some one showed you, or taught you, lots of things in real estate are not google-able, or you didn't even even know you should be thinking about it.

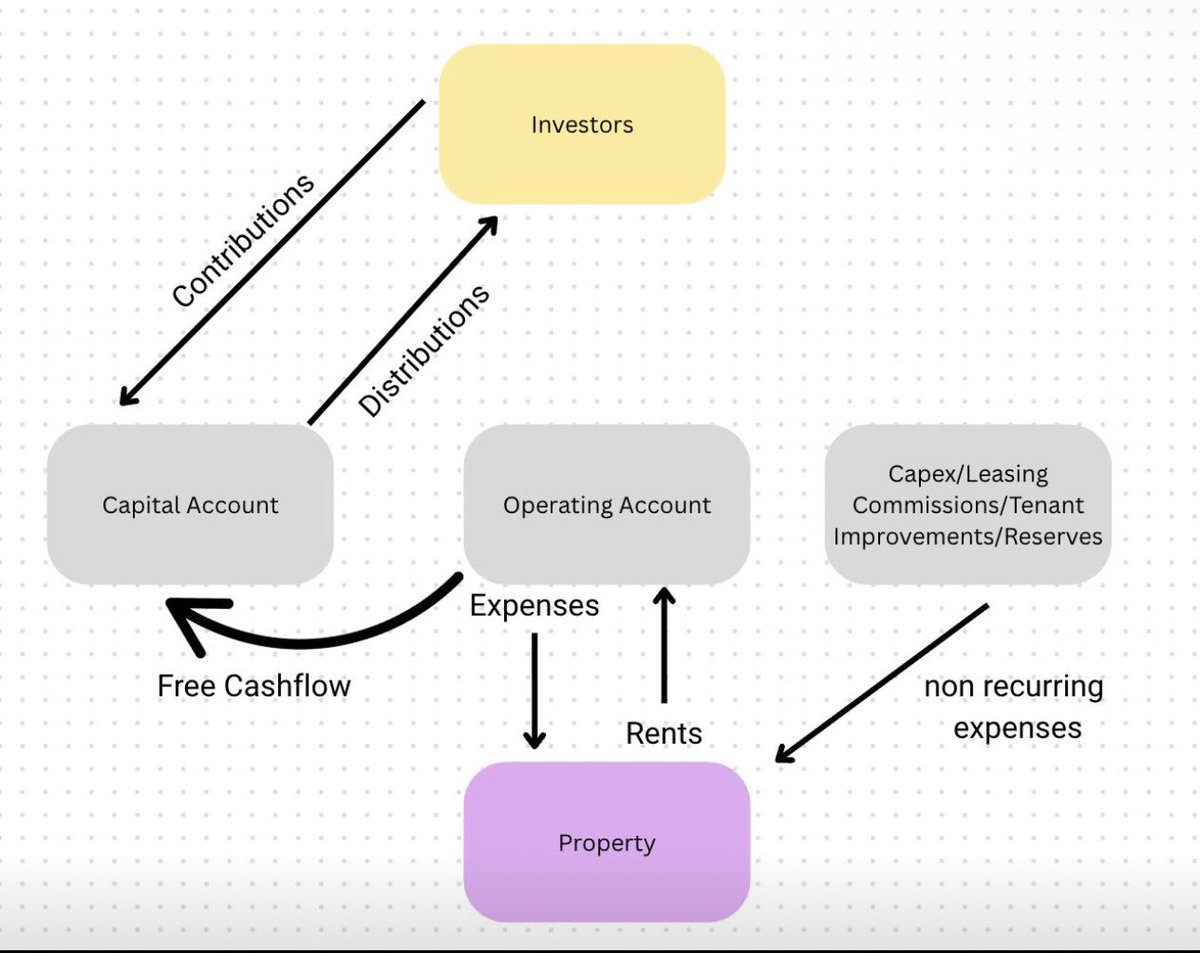

I could certainly be wrong here, but this is how I set up bank accounts. Probably lots of ways to do it, but this way makes sense to me. I'm not an accountant so don't think I am one, and don't get mad at me if anything below is wrong.

When I buy a deal, I set up three different accounts:

1. Capital Account: LPs invest money here and get distributions here. It makes it dramatically easier to calculate returns when all you have are contributions and distributions here.

2. Capex/LC/TI Account: Anything non recurring goes here, construction, leasing commissions, tenant improvements. This is also where I keep capitalized reserves.

3. Operating account: I keep this account pretty low, because the property manager has access to this account, and if they try to rob me, I want it to be a relatively small amount. I have debt service come out of this account, but you could also have a separate account for loans

English

@iononrecourse Gables had a little ring to it for a little while

English

The only company I know of that was able to create a brand in multifamily: Post Properties.

One of the great development companies, they built garden apartments in nice pockets of the sunbelt.

The differentiator was simple - a preposterous amount of landscaping with tulips as the feature.

All the property names carried the Post preface. There was a perceived consistency and quality that got them premium rents.

They had a great run until straying from the original premise into high-density urban properties. Hit a rocky patch and the genius founder John Williams got squeezed out in a Tom Wolfe-worthy coup.

Surprised no one else has pulled it off.

English

@rledbetterCPA Thank u! So theres a diff class of LP that owns more of the partnership bc they own none of the s corp? Quite the calc to truly get it pro-rata all said & done. Only one type of shholder finna scorp…. Good thing partnerships are so damn flexible… toes to nose shit right thur.

English

@PhilLaut Bingo. Or if the partner is ineligible to be a S-Corp partner, you work it out in the economics of the partnership. It'd be ordinary income to them out of the S-Corp anyway.

English

Real estate tax 101 is not putting the property in a S-Corp

It messes up basis and flexibility of owners

But there's an exception - buying land and subdividing

The reason is that this is more like a "business" than a "rental"

Which means you'll be taxed at (1) ordinary tax rates, and (2) self-employment tax rates

Not to mention you may be eligible for a qualified business income deduction

The common play here is "land banking"

Buying the land in a partnership with investors, capturing a majority of the appreciation

Then using a S-Corp to "purchase" the lots from the partnership to do work to ready them for sale

This keeps the "investor" intent in the partnership - key for long term capital gains rates

And keeps the ordinary income tax inside a S-Corp

Big developers will do this in what's called a Bramblett transaction - selling the appreciated land to the S-Corp developer on a note, deferring income further while protecting capital gains

English

When you sell a property, the IRS wants a breakdown of the sales price

How much was for

> Building

> Improvements

> Land

Most tax preparers assign the sales price "pro-rata" based on original cost

But this creates more recapture gain (ordinary rate, not capital gain) than is realistic

The furniture (subject to recapture) did not increase in value as much as the land or building

And the IRS requires a "respective fair value" approach

For example, if the property has been held for 10+ years, having ordinary income tax on recapture from original landscaping doesn't make sense

This has literally saved my clients millions in taxes on exits

Always double check Form 4797 in those sales years

English

@baldridgecpa It might actually be easier to just do a really high income taxpayers tax planning bc u know they at max tax rate well over all cliffs no nothin none of this stuff

English

Some guy turned down a $10,000 raise because it would push him from the 12% bracket to the 22% bracket.

Twitter laughed at him.

"That's not how marginal rates work!"

They're right. He's wrong. What an idiot, right?

But a client called me two weeks ago freaking out.

She was about to lose $12,400 because she's projecting $5,000 too much income.

Here's what happened:

She's 58. Husband is 56. They run a consulting business together.

They buy health insurance on the ACA marketplace.

Last year they made ~$85,000. Paid $9,100 for coverage.

This year they're projecting $90,000+.

She got her 2026 premium quote.

$21,500.

That extra $5,000 in projected income was going to cost her $12,400.

That's a 248% marginal tax rate.

The ACA subsidy cliff came back.

Enhanced subsidies expired December 31, 2025 and Congress didn't extend them.

If your household income exceeds 400% of the Federal Poverty Level, you lose ALL premium tax credits.

For a couple, that cliff is $84,600.

She was about to blow right past it.

We ran the numbers.

A $10,000 retirement contribution drops her projected income to $80,000.

Well under the cliff.

She keeps her subsidies. Saves $12,400 in premiums. Saves another $2,400 in federal tax.

$14,800 in total savings on a $10,000 contribution.

That's a 148% return before her money even grows.

Problem solved.

We had until December to sort this out, but a ton of people will fall off this cliff and never know.

This is one cliff. There are more.

QBI Deduction

Accountants. Lawyers. Consultants. Doctors.

You get a 20% deduction on qualified business income.

$400K profit? That's $80K off your taxable income.

Worth $30K in tax savings.

Phase-out starts at $201,775 single / $403,500 married.

Every dollar above that threshold eats into your deduction until it's gone.

Net Investment Income Tax

3.8% surtax on investment income.

Kicks in at $200K single / $250K married.

These thresholds haven't moved since 2013.

One dollar over and every dollar of dividends, interest, and capital gains gets hit.

Capital Gains and Dividends

0% tax on qualified dividends and long-term capital gains up to $94,050 married / $47,025 single.

One dollar over? 15%.

This isn't a phase-out. It's a cliff.

Social Security Taxation

Combined income over $25K single / $32K married?

50% of your Social Security becomes taxable.

Over $34K / $44K? 85% taxable.

These phase outs haven't changed since 1993.

A Roth conversion can flip a switch and make your entire Social Security check taxable.

SALT Deduction

The cap went up to $40,400 in 2026. Good news.

Bad news? It phases out above $505,000.

High earners in New York, California, New Jersey?

You might be back to the old $10,000 cap.

Senior Deduction

New for 2026. Extra $6,000 if you're 65+.

Phases out at $75,000 single / $150,000 married.

That threshold is LOW.

A lot of retirees will lose part or all of it.

Here's the point.

Your AGI says you're in the 24% bracket.

But your REAL marginal rate might be 50%. 100%. Sometimes 248%.

How much more tax will that incremental dollars of income cost you?

Most people don't find out until it's too late.

Here's what to do.

Know your cliffs.

Model your numbers BEFORE year end.

Build in a margin of safety.

You don't want a surprise 1099 in January to blow you off a cliff you thought you cleared.

Sometimes a retirement contribution pulls you back under.

That's exactly what we did for my client.

Sometimes you defer income to next year.

Sometimes you just pay it.

But don't stumble over a cliff because someone told you "marginal rates don't matter."

They don't. Until they do.

Run your numbers. Or call someone who will.

H/T to @money_cruncher for the inspiration. Definitely give him a follow.

English

@Metalsandman999 The phase outs are mostly tight enough they can be planned around

Maybe cliff isn’t the best word. But when you get to the end and realize you could have planned for it but just didn’t what’s a better term for it?

Landmine?

English

> Mom, how did we get so poor?

> Your dad owned a very successful illiquid startup but loved sunsets on the Santa Monica pier a little too much

English

@rledbetterCPA if the business is an llc taxed as an s corp does anything change?

English

100% bonus depreciation is back

And a lot of business owners will expand, take bonus, and save a ton in tax

But if you own your business real estate in a separate LLC, the self-rental rules can trip you up

1.469-4(d)(1)(C) is an election you should know about to free up those losses

Example -

Taxpayer and his partner own a business 60/40 that made $500,000 in profit in 2025

They also own the building the business works in 60/40, and pay rent to themselves

In 2025, they did a $700,000 expansion to the building and want to take that as bonus depreciation to offset business income

After the bonus, the real estate LLC will generate a loss of $600,000

Without the above election, the self-rental rules will classify the $600,000 real estate LLC loss as passive

Meaning, it won't offset the active business income

But the 1.469-4(d)(1)(C) election allows a rental and business to offset with same proportionate ownership

It's just not automatic

It makes sense too - otherwise it's a penalty for liability protection

Enjoy that bonus depreciation - but double check your elections to not lose the benefit!

English

@bhallcpa @patrickdichter Not that hard to get clients why wouldn’t these enterprising PE firms recruit 3 great CPAs pay them a big salary to get clients hire staff as they go and help them build a firm with $2M ebitda over 4 or 5 years. Rather than pay $20M for a firm doing $2M ebitda. Wtf is that

English

I get a lot of calls from traditional searchers trying to buy accounting firms. “Yeah I’ve been looking for 9, 12, 15 months and can’t find anything.”

Not surprised because they’re trying to buy $1-2M EBITDA accounting firms and can’t go smaller due to traditional search model. Those don’t come up for sale often, and usually get bought be big firms or big PE first for 5-8x multiples.

I tell all of them to look smaller or consider a self funded search because you can start smaller and grow organically and/or do additional acquisitions. But I think most don’t like my advice.

English

@CPATaxTeam @pwrhtr777 @maxpashman Ain’t the gift/sale to trust estate tax savings where as roth is income tax savings?

English

@pwrhtr777 @maxpashman Gift/sale of partnership interests to a trust. Saved over $20mm, about 30% of value in taxes.

Charitable LLC for gifting

English

The reality on Back Door Roth: Most advisors will point to the lifetime growth in a taxable account and then include a 20% capital gains tax on that to show why a Roth is so much better than a taxable investment account.

Reality: the client rarely taps into the Roth in retirement and leaves it to the kids. The taxable account is stepped up and has no capital gains meaning the tax difference is nominal (under 1% tax effect). Almost every one of our tax clients ends up rarely using the Roth not realizing a taxable account would have the same effect, but also allows the beneficiary to hold that account instead of having to liquidate it within 10 years.

Don't fall for the analysis that the taxable account is all taxed in retirement. Most never even touch half of their retirement accounts or taxable accounts and they end up passing them on to heirs at stepped up basis. #taxes #rothIRA

English

@Dirtdog When you get a construction loan towards end of this window, are you able to value the land (for sake of the size of the construction loan) at an amount greater than you finna close at?

English

Typical Deal Timeline for My Offers

My standard timeline from contract to closing is 240–330 total days, structured as follows:

• 90-day Inspection

• 120–210 day Govt Approvals + 2 - 30 day extensions

• 30-day Closing

This timeline is what allows me to help you pay the prime rate you want for your land. Without this unfortunately your land is not worth that price to me.

INSPECTION PERIOD (First 90 Days)

Immediately after going under contract, we order the following due diligence items:

• Phase I Environmental Report

• ALTA Survey with Topography

• Title Report and Abstract (once available)

• Geotechnical / Soils Report

• Site Investigation Report (SIR) – details all fees, departments, connections, impact fees, utilities, and requirements for development

GOV’T APPROVALS PERIOD (120–210 Days + Extensions)

During this phase, we pursue the key entitlements:

• Conditional Use Permit (CUP) – 3–6 months on average

• Site Plan Approval – pursued simultaneously with the CUP when allowed (sometimes sequential)

• Building Permit – lower risk while working with the building department vs the public meeting processes for the site plan and CUP but it still takes time to get through

• Construction Loan (if needed) – secured toward the end of this period once approvals are in place

CLOSING PERIOD (30 Days)

I have never regretted giving myself a full 30 days to close once all approvals and financing are lined up. However, I have regretted every single time I’ve had less than 30 days.

If something can go wrong at closing, it inevitably does on the deals with a rushed timeline. The extra 30 days provides critical breathing room for any last-minute issues with the city, lender, or capital deployment.

This structure protects both the seller and buyer and ensures we can deliver the premium value the land deserves. Once I have closed I will have the retailer I am working with asking me every 5 minutes if we are tracking on time for our delivery to them and can I shave a few days off. It is critical all of the homework is done up front.

What else do you look for on your land timing for development projects? Comment below or share this for reach.

English

@DallasAptGP What happens if you only deploy some of the money you put in your QOF?

English

Most people don't realize a capital gains tax bill is actually a Golden Ticket.

Here is the 2026 reality: You have a gain. You are paying the IRS in April 2027. That is happening no matter what.

But that tax bill is your entry fee. Only those with realized gains can enter a Qualified Opportunity Fund (QOF).

Think of it like funding a Roth IRA.

You use after-tax money. No deduction today. But if you hold for 10+ years? Everything that grows comes out Tax-Free.

With a QOF, you are paying taxes on the seed, not the tree.

The 2026 deadline isn't "invest before the benefit disappears." It's "invest before you lose access."

You are already paying the cover charge. Why wouldn't you go to the party?

English

@Eli_Albrecht What industry have you found this to be most common in

English

Very few days go by that I do not hear about a founder seller selling to Private Equity, buying back their business for pennies on the dollar, and reselling to PE a few years later.

English

@bhallcpa @CPATaxTeam What is a very large portfolio? 15 commercial properties with 45+ tenants? Or very large like publicly traded reit large?

English

@CPATaxTeam Appfolio or buildium. Yardi for very large portfolios (but only after outgrowing appfolio)

English

For those real estate accountants out there...what is the best management software program now? Yardi Breeze?

English

@BigJohn043 @paulswaney3 I wonder how many "families" would come out ahead with a "boglehead" approach with maybe just VT in it.

Part of me thinks it's more ego investing than disciplinary investing, at least until you have enough $ to buy an MLS team.

English

The big issue with family offices is they generally don't have a well defined buy box. Or it changes all of the time.

Can't tell you how many friends worked at one of these and did a bunch of work on a deal only for the family to decide at the last minute they didn't like it.

The other side is the family member comes to you with the VC idea that their golf buddy has and all of a sudden you are a VC....

Boring_Business@BoringBiz_

The most underrated job in finance is the family office route > no pressure from LPs, since there are none > evergreen fund structure, don’t have to worry about exiting investments within a certain period of time. You can hold on to winners for as long as you like > less timing pressure to get deals done since there isn’t as much pressure to deploy dollars right away > teams are typically smaller, so you get direct access to seniors and management for learning ramp Comp and work life balance can vary pretty highly across different family offices. But if you find the right fit for you, those are jobs that you never want to leave

English

2026 Predictions

1) Bitcoin, currently at $90k, will end the year higher.

2) The 10-year U.S. Treasury yield, currently 4.15%, will end the year +/- 25bps.

3) Nov CPI was 2.7%, it will end the year higher.

4) The Fed Funds Rate will end the year lower than 3%.

5) The stock market, as measured by the S&P 500, will end higher.

6) Multifamily Rent growth in DFW is currently -2.9% YoY, it will end the year below 0%.

English

@rledbetterCPA @aussieflya LPs with a $0 capital account who are not guaranteeing the debt but are allocated their portion of qualified non recourse debt can’t take losses?

English

For sure.

Year 1 cost seg - all LPs have positive capital accounts. Bonus depreciation flows first to capital accounts, so LPs would get the losses (likely still suspended for passive)

Year 3 cost seg - all LPs have received refinance return of capital distribution, taking their capital to $0. Future losses now flow to recourse debt holders - including bonus depreciation. GPs holding the guarantee would get the losses and offset it with other real estate income

English

A cost segregation study in Year 1 isn't always the answer.

Yesterday during a year-end session with a client we talked about impacts of capital accounts with recourse debt and cost segs.

Delaying some of the cost segs will save them hundreds of thousands in tax in Year 3+.

English

@investing_law I would appreciate the full thing. Thank you for sharing with us !

English

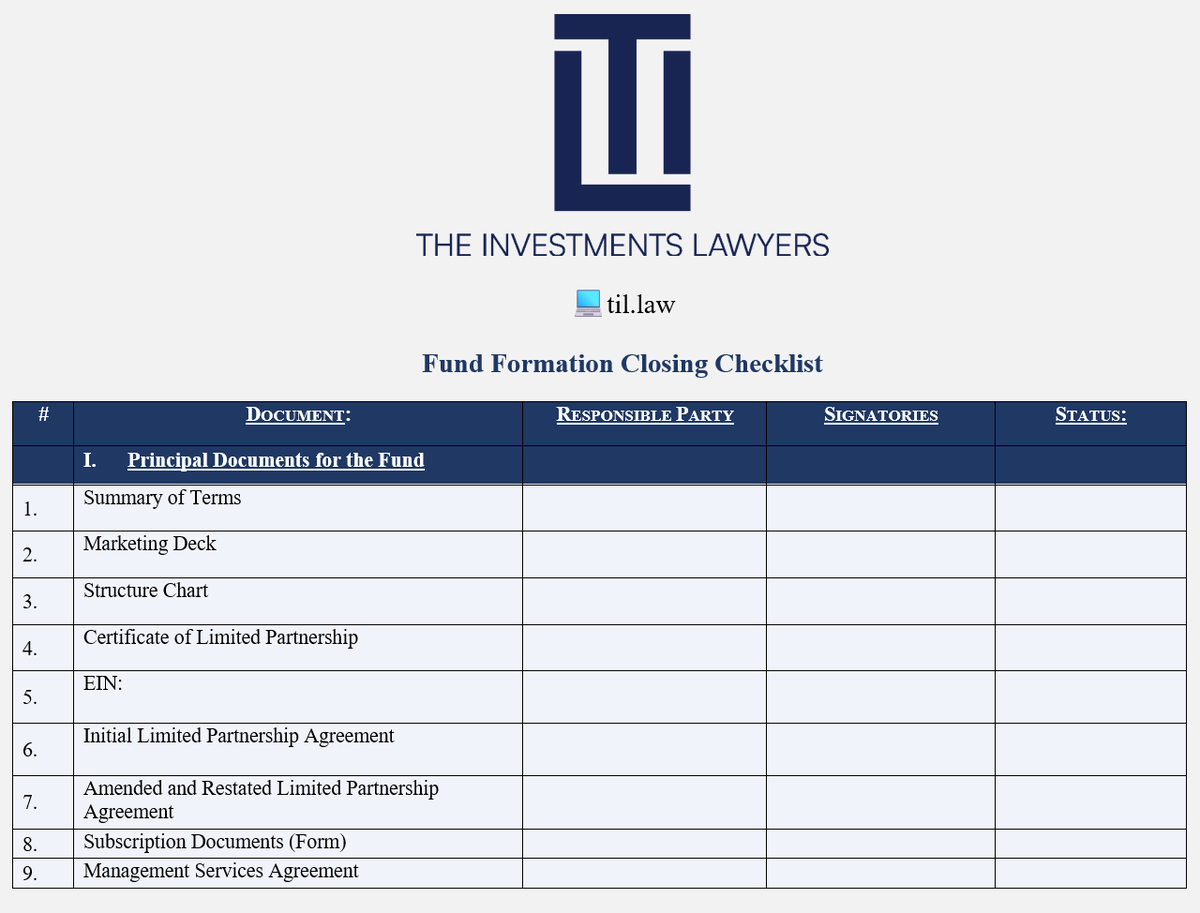

Here’s the first page of our investment fund formation checklist (works for SPVs too).

If you want a Word version of the full thing, comment below!

Every fund formation will have its own unique requirements, but some general categories of “to-dos” include:

🔹Entity Formation

🔹Marketing Deck / PPM

🔹Summary of Terms

🔹Initial LLC/LPAs (short-form)

🔹A&R LLC/LPAs (long-form)

🔹Subscription Document Preparation and Review

🔹Intercompany Management Agreements

🔹Ancillary Agreements (e.g., Closing Resolutions)

🔹Side Letters

🔹Securities Act Filings (Form D / Blue Sky)

🔹Advisers Act Registrations (ERA / RIA)

What questions do you have?

(Note that this checklist is not legal advice! Every fund is different. Work with your lawyer.)

English