Sabitlenmiş Tweet

Altcoin-Season // NOT like 2017 and 2021!

I have the desire to get rid of this. It's about the so-called "altcoin season" that everyone is talking about, and it's a 100% thing that altcoins will explode. People's reasoning? "But, they existed in every cycle, so they will now be there again, and it will go up again."

We need to start by looking at the Bullrun cycles differentiated with all the corresponding factors, and not as one unit.

So…

2017:

Let's start with 2017, which can be done very quickly.

The Bullrun 2017, the total market capitalization was not even $20 billion dollars, so there was no/barely any liquidity necessary to pump the market massively, is probably logical, where no/little capital is available, it also needs little to grow massively.

At the same time, there were only a few hundred-maybe 1-2 thousand projects on the market, the market was so incredibly small that the capital was divided into a small number of projects. Because in the end, each project takes something of the cake, in the end also means, the more projects, the less potentially remains for each individual project.

Capital is diversified.

2021:

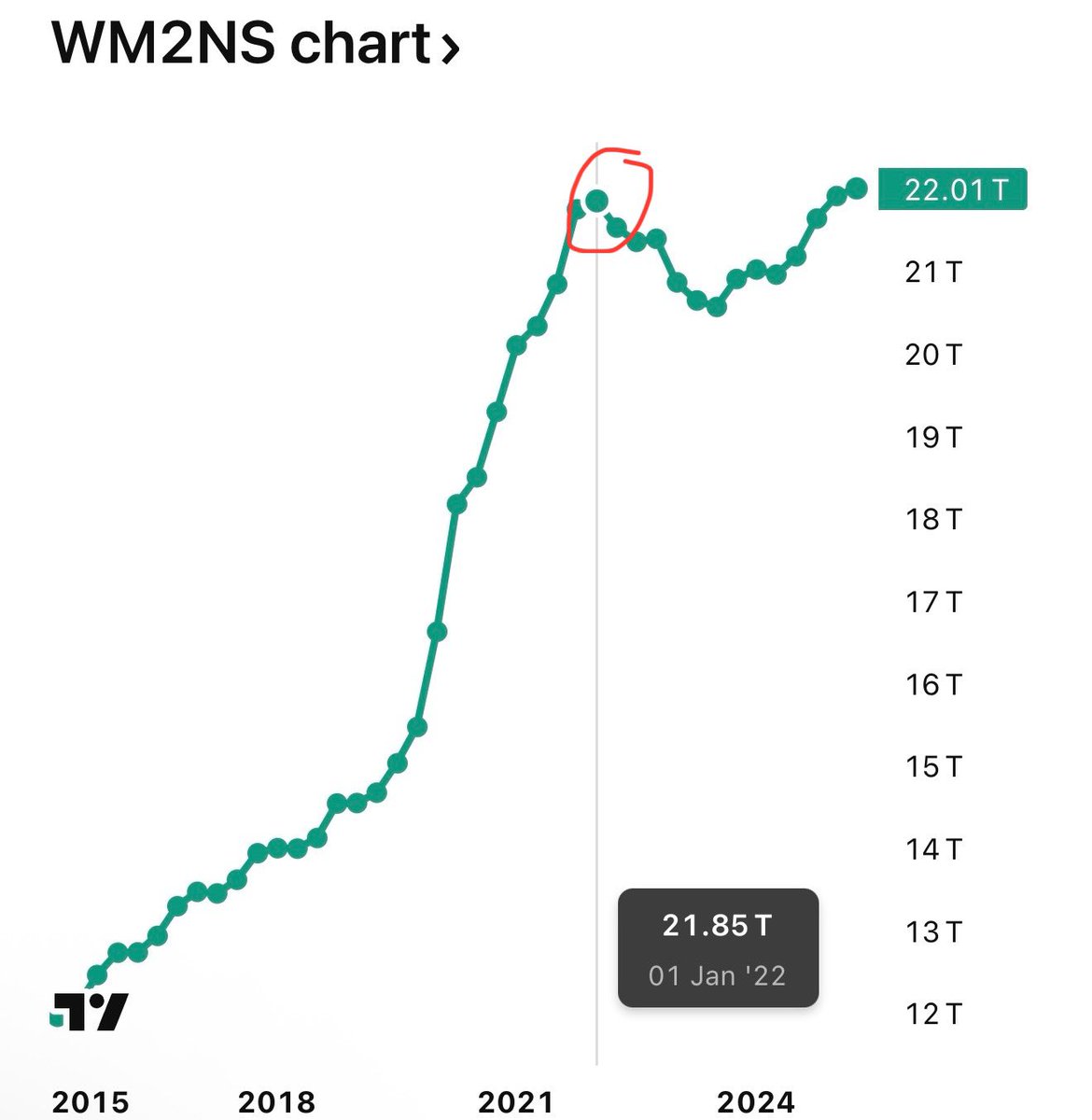

2021 was also a cycle that was quite different, this cycle was at a time when we were in a state of emergency. It was the Corona time. The M2 has risen by 1/3 in this short time alone. The M2 has thus increased by 1/3, i.e. by about 40%, within 2 years.

The money supply M2 rose from $15.47T to $21.85T...that's the +40%.

At the same time, there were MASSIVE QE + state transfers, and interest rates were close to 0%, and that until the beginning of 2022.

In the time, it was a record QE... QE increased from $4.2T to approx $9T, it rose by over 110%!!!

This was a time when MASSIVE MASSIVE MASSIVE liquidity was released and created!!!

We do not have these parameters in this cycle. Quite the contrary.

In this cycle we have higher inflation, higher interest rates, no QE, but QT, significantly more crypto projects like in 2021, which will all get something out of the liquidity, and not like 2017 or 2021, where the selection was by far much smaller.

Again, the new capital that comes into the market is also even more widely diversified among all the projects.

And if we take the low of the M2 in the summer of 2023 with the current status, we have come from $20.57T to only $22.01T. That's only 7%.

That's why I'm making it clear that statements like: "but there's always been an altcoin season, and massive pumps have always happened there." are irrelevant.

Because we have a COMPLETELY NEW environment, with absolutely different factors!

These are the hard data/facts... and no "would/could/if" statements.

The origin is always liquidity, high liquidity ensures correspondingly high capital inflows! However, if this is only "relatively" given, and NOT like 2021, it will of course also be a completely different overall picture, and thus become a much more marginal pump.

People just want to hear/read ultra-bullish statements, and every contribution that goes more into realism, and thus also means that the X-potentials will definitely not be as gigantic as many think, will be defamed, and titled as ignorant.

But the truth remains the truth. And the data shows exactly what I'm describing here.

In the end, it is not my job to convince someone, do what you want with the information.

M2 Chart:

tradingview.com/symbols/FRED-W…

Recent balance sheet trends:

federalreserve.gov/monetarypolicy…

1/2…⬇️⬇️⬇️

#Crypto #cryptocurrency #Bitcoin #Ethereum #Blockchain

English