MarketWatts

4.2K posts

MarketWatts

@RootSwego

20+ Years on the Buy side, Energy, Materials , EM & Commodities

Katılım Mart 2009

5.8K Takip Edilen635 Takipçiler

MarketWatts retweetledi

THE WAR WITH IRAN IS EXISTENTIAL! IRAN COULD BOMB A U.S. CITY! AMERICANS MUST IMPOVERISH THEMSELVES TO STOP IRAN FROM GETTING A NUKE! A CIVILIZATION WILL DIE TONIGHT!!!

Man in charge of war: "Excuse me - I need to fly to a small Kentucky county to campaign against a Republican House member."

Dr. Simon@goddek

🚨LMFAO. The Secretary of War flew to Kentucky to campaign against THOMAS MASSIE, the one Republican who actually votes against your kids dying in another forever war. And he seriously opens with this: HEGSETH: "I have to say up front for the lawyers that I'm here in my personal capacity. As a private citizen." Bro! You are the SECRETARY OF WAR. You did not wake up this morning and become Dave from accounting. The regime is sending a cabinet official to take out the most anti-war and pro America guy in Congress and we are supposed to pretend it's a personal hobby?! Massie lives rent free in their entire Epstein apparatus for a reason.

English

MarketWatts retweetledi

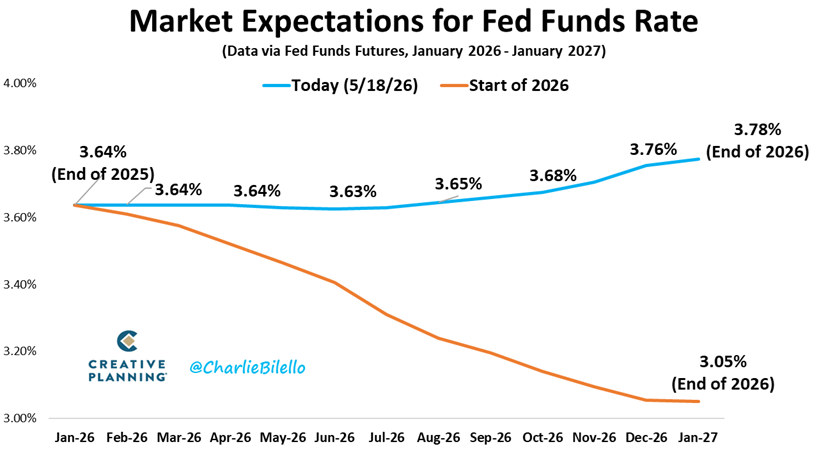

Jan 1: market pricing in 2 Fed rate cuts in 2026.

Today: higher odds of a hike than a cut.

If Kevin Warsh argues the Fed should recommence with rate cuts in June despite all evidence pointing to rising inflationary pressures, his independence will immediately be questioned.

English

MarketWatts retweetledi

BREAKING: Iran is reportedly preparing for a rapid, high-intensity war scenario that could involve launching hundreds of missiles daily at Gulf energy infrastructure, refineries, and ports, according to analysis cited by The New York Times.

The report also warns the Houthis could move to disrupt or shut down the Bab el-Mandeb Strait, potentially opening a second major maritime front alongside the Strait of Hormuz.

English

MarketWatts retweetledi

60 days ago, 🇺🇸Trump : We postponed our attack on Iran by 1 day, very close to making a deal.

40 days ago, 🇺🇸Trump : We postponed our attack on Iran by 2 days, very close to making a deal.

20 days ago, 🇺🇸Trump : We postponed our attack on Iran by 7 days, very close to making a deal.

5 minutes ago, 🇺🇸Trump : We postponed our attack on Iran by 2-3 days, very close to making a deal. 🤣

Elect a clown expect a circus.

English

MarketWatts retweetledi

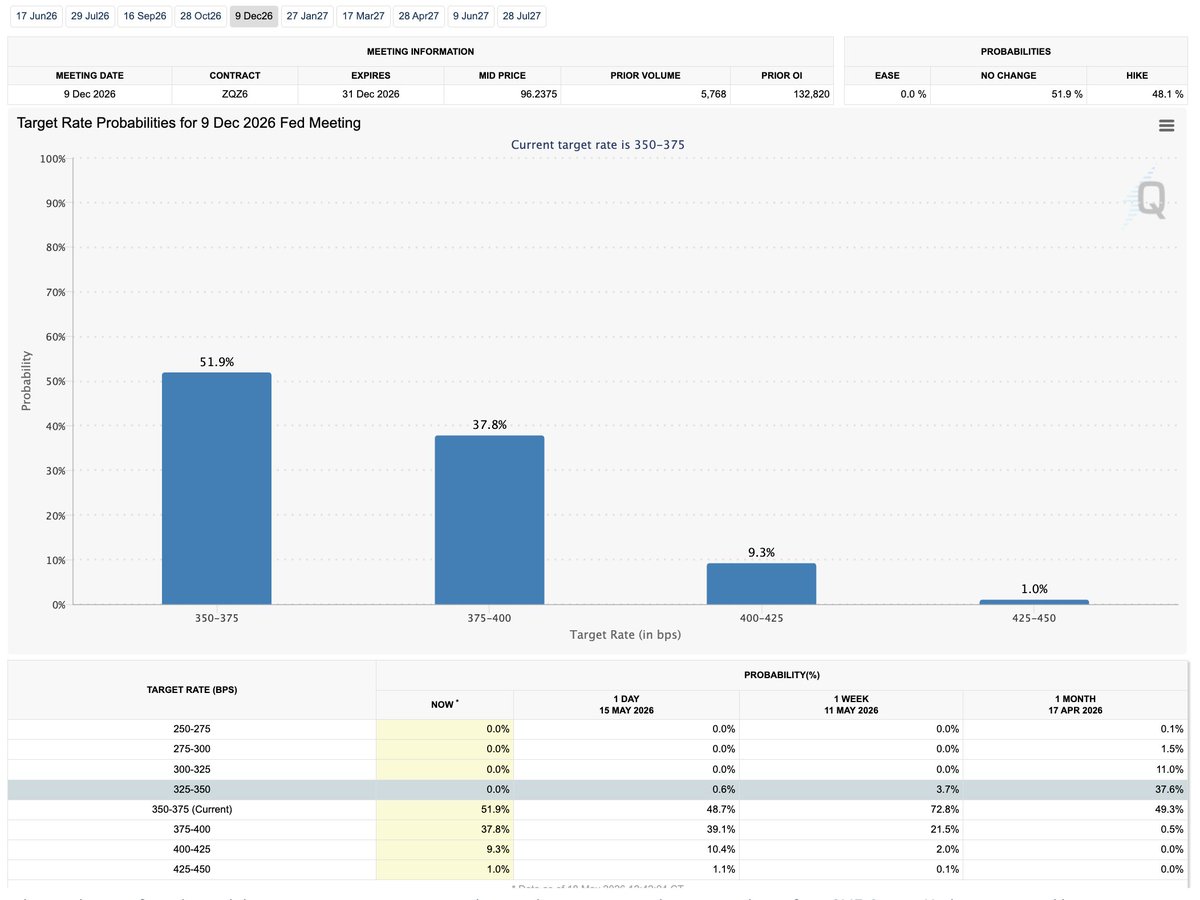

0% chance of a rate cut this year, down from 37.6% a month ago

English

How COVID QE Differed from QE 1, 2, and 3

The impact of QE on the real economy during the Global Financial Crisis (QE1, QE2, and QE3 from 2008 to 2014) was drastically different from the COVID-19 era.

1. The Regulatory Environment: Tightening vs. Loosening

QE 1, 2, & 3: In the wake of the 2008 crash, regulators were actively tightening rules on banks. The implementation of Dodd-Frank, Basel III, and the introduction of the Liquidity Coverage Ratio (LCR) and the SLR forced banks to aggressively rebuild their capital buffers.

COVID QE: The banking system was already well-capitalized. Instead of tightening rules, the Fed loosened them (zero reserves, SLR exemptions) so banks could act as conduits for economic relief.

2. Where the Money Got Trapped

QE 1, 2, & 3: The Fed bought trillions of dollars of assets from the banking system, creating a massive amount of "base money" (bank reserves). However, because banks were trying to repair their balance sheets and comply with new, strict regulations, they hoarded these reserves. They did not aggressively lend them out. As a result, the "money multiplier" collapsed. Base money exploded, but M2 grew at a very normal, sluggish pace. The liquidity was trapped inside the financial sector.

COVID QE: Because of SLR relief and zero reserve requirements—combined with the Treasury directly handing out cash—the money didn't stay trapped at the Fed. It was pushed entirely out into the real economy.

3. The Fiscal Policy Partnership

QE 1, 2, & 3: Monetary policy was largely acting alone. The fiscal response to the 2008 crisis was relatively modest compared to the size of the output gap. QE mostly served to lower long-term interest rates and recapitalize banks.

COVID QE: Monetary policy and fiscal policy merged. The Fed monetized the debt, the regulatory rule changes allowed the banks to process it, and the Treasury delivered it to the public.

English

MarketWatts retweetledi

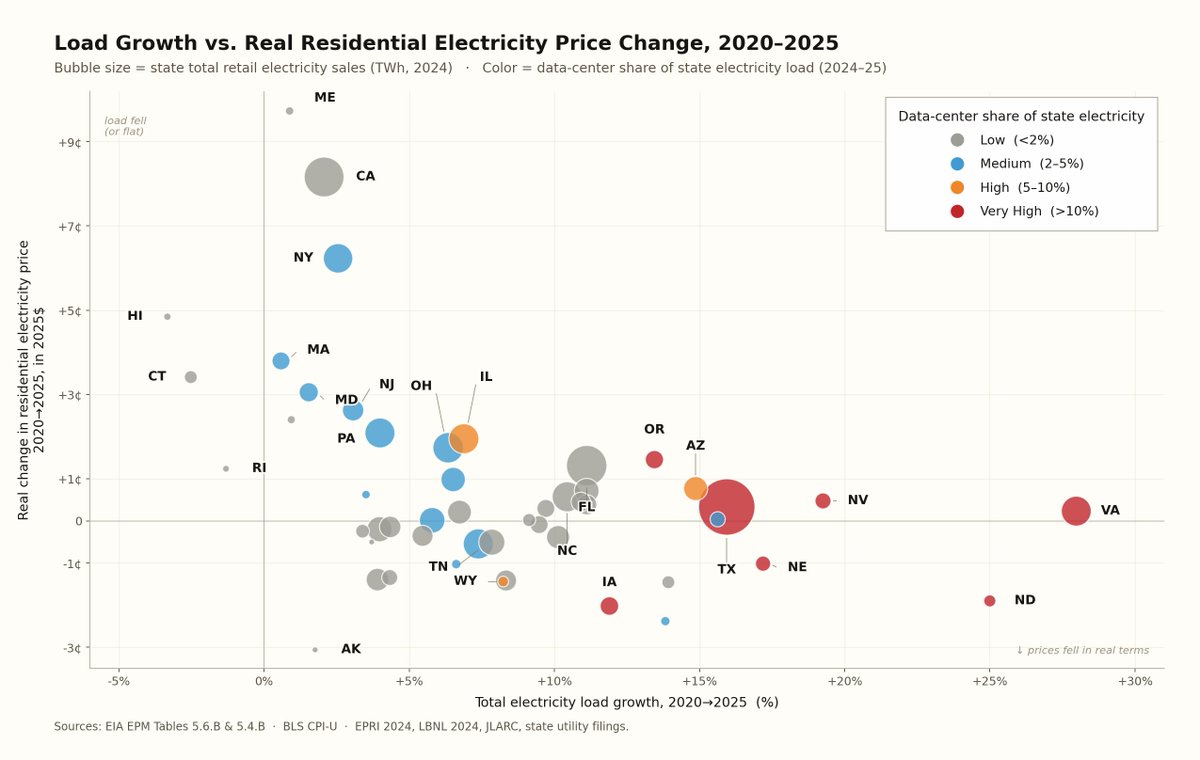

This is the single most important chart.

If AI were driving prices, you'd see a cluster top-right. You don't.

States with huge load growth (VA, TX, NV, ND, IA) sit at ~0c change in 5y. States with massive price hikes (CA, NY, MA, CT) have basically NO load growth.

English

MarketWatts retweetledi

The most absurd number in CPI? According to the US Government, the cost of health insurance has declined 20% over the last 5 years...

English

MarketWatts retweetledi

US electricity prices are surging well ahead of inflation:

Electricity prices jumped +6.1% YoY in April, the highest reading since January.

This marks the 8th monthly increase above +5.0% over the last 10 months.

At the same time, overall US CPI rose +3.8% YoY, the biggest increase since May 2023.

This means electricity prices are rising ~61% faster than the broader inflation rate.

This comes as surging power demand from data centers is straining US energy grids, pushing wholesale electricity costs sharply higher.

Since January 2020, average US electricity prices have soared +44%, to an all-time high.

Over the same period, the CPI has risen +28%, also to its highest level on record.

US electricity price growth is accelerating.

English

MarketWatts retweetledi

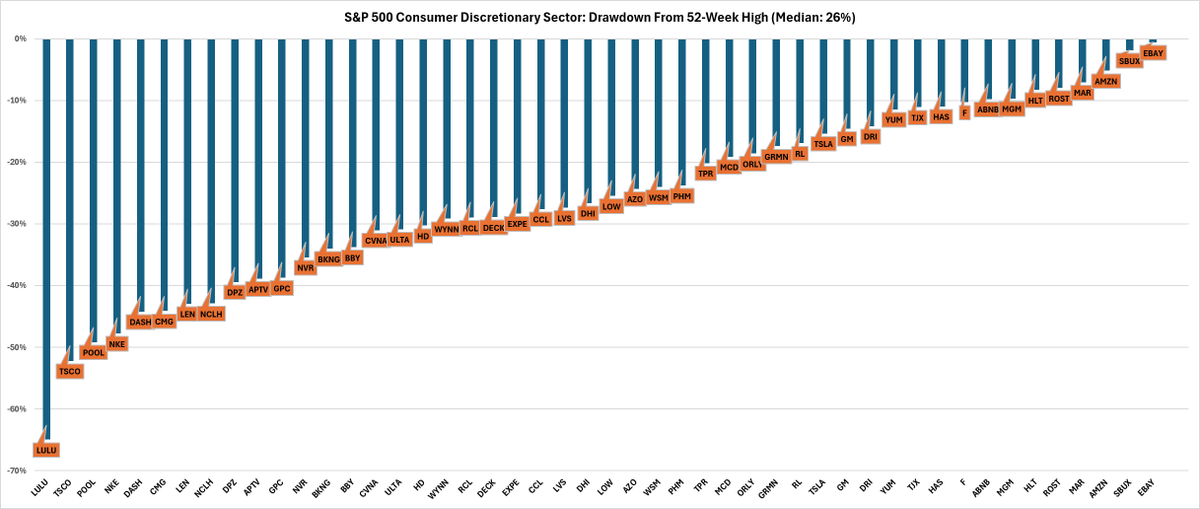

S&P 500 Consumer Discretionary sector median component drawdown from 52wk high?

26%

Worst: $LULU -65%

Best $EBAY -0.6%

English

MarketWatts retweetledi

MarketWatts retweetledi

MarketWatts retweetledi

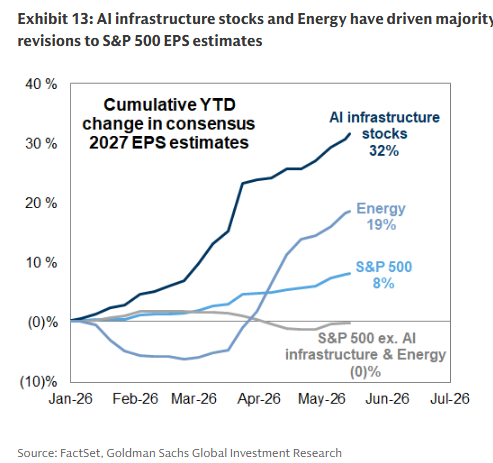

Ex-AI & Energy, S&P 500 EPS revisions are dead flat YTD

English

MarketWatts retweetledi

“My investors what to know what returns are at strip.”

-PE guy walking away from generational buying opportunity during COVID lows

HFI Research@HFI_Research

oIl fUtuReS cuRve PrEdiCts lOwEr pRIces

English

MarketWatts retweetledi

Japanese actor Hiroyuki Sanada spoke about the contradictions of human nature:

“Some people dream of having a swimming pool at home, while those who have one hardly ever use it. Those who have lost a loved one feel a profound sense of loss, while others often complain about their living relatives. Those without a partner long for one, while those who have one often don't appreciate it. The hungry would give anything for a meal, while the satiated complain about the taste of their food. Those without a car dream of owning one, while those who have a car are always looking for a better one.”

The key to happiness is gratitude: truly seeing and appreciating what we already have, and understanding that somewhere, someone would give anything for what we take for granted.

English

MarketWatts retweetledi

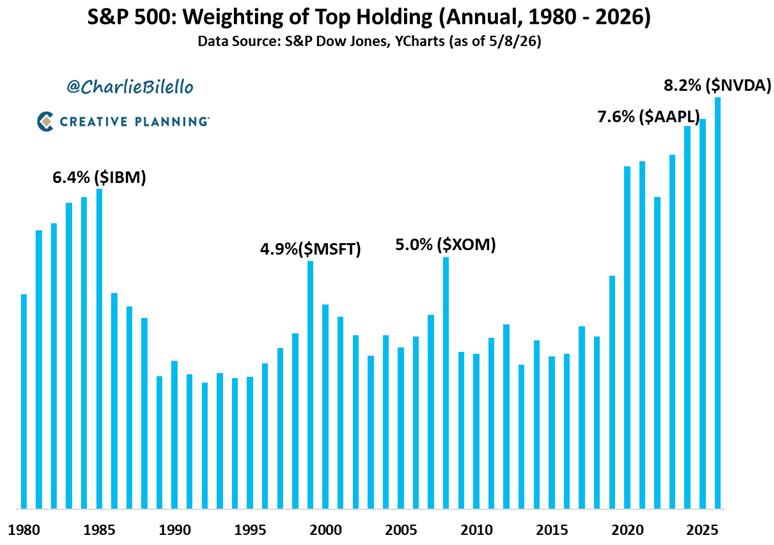

The S&P 500 has never been more concentrated in a single stock than it is today with Nvidia representing over 8% of the index.

English

MarketWatts retweetledi

G7 bond yields hitting 20-year highs isn't a blip—it's structural.

• Energy-driven inflation 🔥

• Endless government deficit spending 💸

• Fed QT shrinking liquidity 🏦

• Deglobalization raising term premiums 🌐

Torsten at Apollo

English

MarketWatts retweetledi

In Iran, they are publishing the five conditions set by Trump for a deal:

1- The U.S. will not pay any compensation for the damages to Iran

2- Transfer of the enriched uranium to the U.S.

3- Only one nuclear facility will remain operational inside Iran

4- Less than a quarter of Iran’s frozen assets will be released

5- The cessation of war on all fronts is conditional on holding negotiations

In contrast to the five "confidence conditions" set by the Iranians for holding negotiations:

1- Ending the war on all fronts

2- Lifting of sanctions

3- Release of the frozen funds

4- Compensation for war damages

5- Recognition of Iran’s sovereignty over the Strait of Hormuz

English