I wasn’t planning to share this, but it’s such a high-quality explanation of CPO that I have to.

Just watch it. You’ll regret it if you don’t.

youtu.be/wiH6d4m9o4o?si…

Morgan Stanley recently published a bottom-up model on hyperscaler datacenter CAPEX spending.

A 1GW NVDA Vera Rubin datacenter costs $41bn. A 1GW Trainium3 cluster costs $15bn.

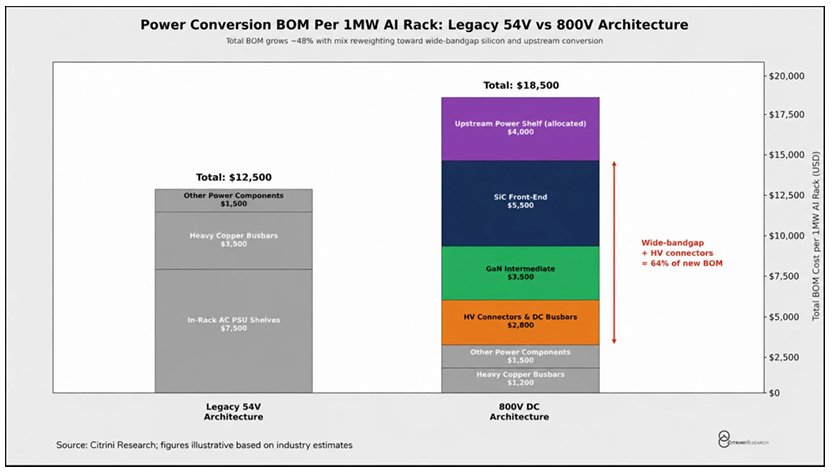

The Powered Shell sits at 6-14% of every build.

That is $2-6bn per GW.

This is the power semis opportunity.

Here is a list of stocks that benefit the most in each generation:

Current Gen - Silicon Power Delivery

$MPWR – The rack power incumbent. Monolithic has accumulated design wins across the Blackwell generation for DC-DC conversion. Higher switching frequencies mean less copper, less heat, more density. 800V datacenter samples already out, but the bigger revenue ramp lands in 2027.

$VICR – Factorized Power Architecture pure-play. Products are concentrated in the datacenter and hyperscaler segments for power delivery on server motherboards and inside racks. Working toward delivery of a next-gen high-density VPD system for a lead AI customer. Underowned relative to how architecturally embedded it actually is.

$POWI – The GaN entry point. PowiGaN technology is being developed directly with NVIDIA for the 800 VDC architecture transition. Industry-first 1250V GaN switches achieve greater than 98% efficiency, outperforming both stacked 650V GaN and 1200V SiC alternatives.

Confirmed NVIDIA collaboration.

Next gen - Wide Bandgap Semiconductors (2026 to 2028)

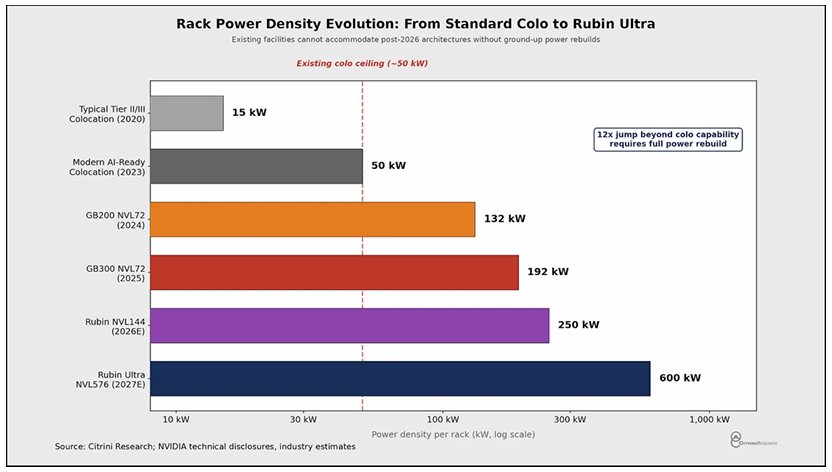

When rack power hits 100kW and beyond, silicon hits its switching wall. GaN and SiC move in.

$NVTS – The GaN pure-play. Confirmed NVIDIA collaboration on 800V HVDC architecture for Kyber rack-scale systems powering Rubin Ultra. GaNFast and GeneSiC platforms cover both AC-DC and DC-DC conversion layers. Strongest confirmed design win of the group.

$AOSL – The GaN challenger. Also collaborating directly with NVIDIA on 800 VDC architecture, covering SiC for high-voltage conversion and GaN FETs for high-density DC-DC conversion inside the rack. Smaller cap, higher beta to design win acceleration.

$WOLF – Post-bankruptcy optionality. Emerged from Chapter 11 in September 2025 with debt cut 70% and interest expense cut 60%. Now targeting AI datacenters alongside EVs and aerospace as the next growth vector. Highest beta to SiC datacenter adoption if the thesis plays out, but revenue confirmation is still ahead.

Test infrastructure

$AEHR – Wafer-level burn-in leader for SiC, GaN, and silicon photonics. The only name that sits on both the power and photonics layers. Expanding into AI processors and GaN production orders with improved visibility into H2 fiscal 2026. Scales with every new wide bandgap production ramp regardless of who wins the platform battle.

Disclosure: I own $NVTS $AEHR on this layer.

Bullish Power Semis

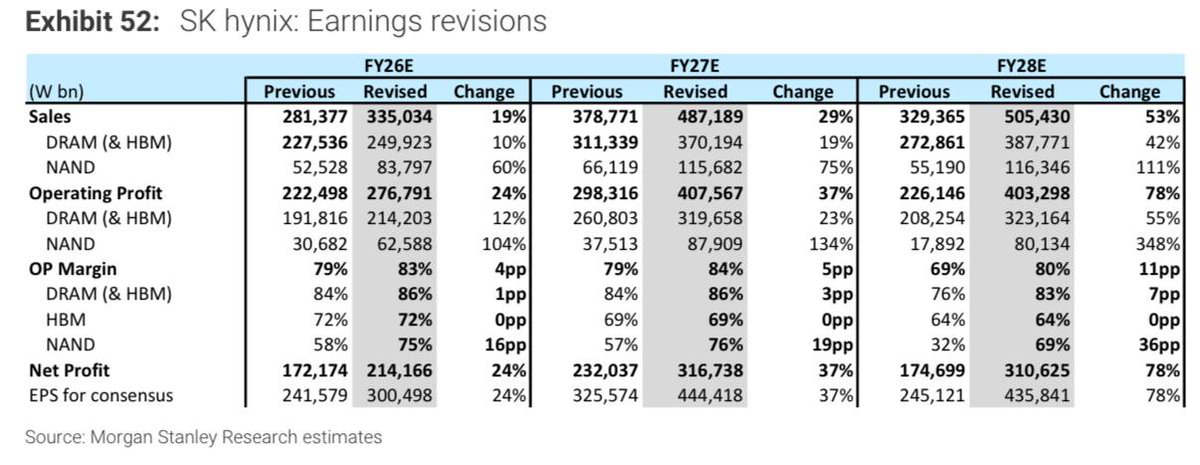

Thread: Korea’s Memory Exports, May 1–20

1. DRAM

DRAM, including modules: export value of $11,527mn, +498% Y/Y, +27% M/M

The DRAM export unit price, including modules, reached $60,319/kg, up 5% from April 20, 2026, and up 432% Y/Y.

New TIL: I figured out how to use my LLM CLI tool in a shebang line, which means you can write executable scripts in English, or hook up more complex scripts with a snippet of YAML template

Jukan's Truth Time:

Many people have been asking:

"Samsung has its own DRAM division — so why isn't it aggressively pursuing mobile device market share expansion during a memory shortage like this?"

Today, I'll give you the answer.

First, let me clear up a common misconception.

Samsung's MX (Galaxy division) and Samsung's DS division (semiconductor division) only share the Samsung name — they do not share a single, unified interest. Each puts its own profits first.

This became clear in what happened before Samsung MX launched the Galaxy S25.

At the time, Samsung MX concluded that the LPDDR5X built on Samsung's 1b node lagged behind the offerings from SK Hynix and Micron in both performance and thermals. Yet Samsung DS was trying to sell this underperforming LPDDR5X to Samsung MX at a higher price than SK Hynix's and Micron's LPDDR5X.

This led to an unprecedented outcome: Micron — not Samsung — became the first vendor for the mobile DRAM in Samsung's flagship S-series smartphones. (TM Roh, head of Samsung MX, later denied this. But for at least the initial-to-mid production volumes, Micron has been confirmed as the first vendor.)

Now, however, the situation is reversed. As the term "Memorypocalypse" floating around the market suggests, memory is currently in extreme short supply.

So — after going through what happened in 2025, would Samsung DS really turn around and supply LPDDR5X to MX at a discount?

Another interesting point: one of the reasons MX cannot source DRAM cheaply from DS is that DS has to be mindful of its external customers.

Specifically, if Samsung supplies DRAM to its internal divisions at a discount, its external customers — who are already paying steep prices for DRAM — would be deeply unhappy. Trust between Samsung and its customers would break down, and customers would hold a grudge against Samsung.

Samsung DS reportedly has no appetite for taking on that kind of risk.

As a result, Samsung MX, having already incurred massive costs in Q1 due to difficulty securing memory and a sharp rise in its procurement prices, is expected to spend even more in Q2 to meet its volume requirements as the world's largest mobile device manufacturer.

This aligns with reports that TM Roh, head of Samsung MX, has briefed management that MX could swing to a loss this year.

In conclusion, the reason Samsung MX cannot aggressively pursue a market share expansion strategy during this memory shortage is not simply that "Samsung has a DRAM division but can't make use of it."

The core reasons are threefold:

First, MX and DS sit under the same Samsung roof, but their interests diverge. Second, DS has no choice but to prioritize its own profitability and its external customer relationships over internal supply. Third, in the current memory shortage environment, MX — like any external customer — is structurally forced to bear elevated memory costs.

That's all for today's Jukan's Truth Time. Thank you.

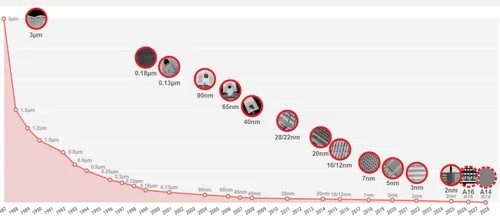

At 2nm, transistors are 10 atoms wide. You can't shrink further.

Yet NVIDIA went from 3,958 TFLOPS (H100) to 50,000 TFLOPS (Rubin) in 4 years.

I wrote about the 5 engineering tricks that replaced Moore's Law:

• Multi-die tiling (1→2→4 chiplets)

• FP8→FP4 precision (free 2× FLOPS)

• NVL72 (72 GPUs as one computer)

• Superchips (CPU+GPU fused at 1.8 TB/s)

• HBM4 (22 TB/s bandwidth for the rack)

This discussion will help you what Jensen Huang was trying to explain during Dwarkesh's the latest podcast.

This approach is also recipe for how Chinese companies like Huawei are trying to catch up, and they will do well even if they are forever stuck at 7nm.

polymath707.substack.com/p/moores-law-i…

@TaxAct efiled my taxes a few days ago. I need to amend my return, how can I retrieve a copy of my 1040? I made some changes and the PDF reflects those. I need the original.