SaxoMuse

90 posts

Michael Burry loaded up on Lululemon $LULU in 2025… and it’s been a brutal ride since.

Started buying around the $300+ range

Doubled down into weakness

Stock now: $128.98

That’s a 55–60% drawdown from his initial entry!

Timeline:

Q2 2025 (initial buy) Bought 50,000 shares

Estimated price range: $290–$320

Position value: roughly $15M

Q3 2025 (added / doubled down)Increased to 100,000 shares total

Likely added in the $260–$300 range

Position value: $17–18M at the time

Q4 2025 – Latest filing Held steady (100K shares)

No major trim reported

Classic Burry:

Early

Aggressive

Deep in the red lol

The question is Lulu dead money… or another one of those trades where he looks crazy before he looks right?

English

C'est sur mon site que je produirai en exclusivité mes analyses Phases 3 🇺🇸 et recoveries. Également mes stratégies Options correspondront mieux sous ce nouveau format car très technique.

Le compte X continuera bien évidemment comme auparavant mais toujours sous format X.

Français

Je suis un "petit compte" en terme d'abonnés. Mais en revanche j'ai un Taux d'adhésion hors norme sur X. Ça signifie que les personnes qui me suivent sont très engagés.

Et c'est excellent. Je produit des analyses de secteurs stratégiques et de sociétés qui sont très suivis.

Français

@SaxoDel95616 @0xKasper_ C'est les Ephad qui vont manger tout ton héritage, 4000euros par mois, il faut vendre la maison

Français

@SmithyAlan45201 @0xKasper_ L’extrapolation sur l’exproriation des parents est ridicule

Français

@SaxoDel95616 @0xKasper_ Nos parents ne sont pas encore morts, et la gen Z arrive a l'âge adulte maintenant, ils ont besoin du capital en ce moment, pas dans 10-15 ans. et même, on va pas exproprier nos parents si ? En plus ça a encore le temps de dévaluer, et ça sera taxé par l'état une fois encore.

Français

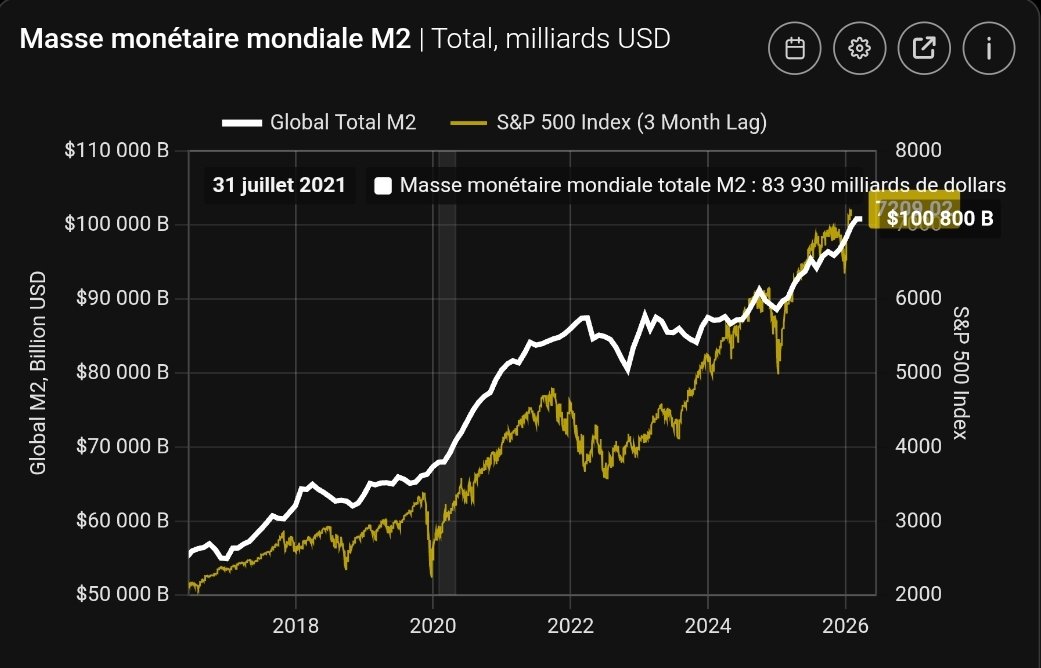

Quel est le principal risque pour les Marchés financiers ?

Comme la M2 n'est pas principalement de la liquidité provenant d'actifs nets sans dettes en contrepartie mais, au contraire, principalement de la liquidité reposant sur la Dette, le risque est le Deleveraging.

Français

This is maybe my favourite trade idea yet?

$EMN up 7% in less than 4 days following my thesis.

And outperforming peers like $DOW.

"Only 7%?!" I hear you say...

Imo, that's pretty damn good since chemicals companies are notoriously slow movers.

Trade TLDR:

- Strait of Hormuz closed = shortages of naptha in Japan (feedstock used to make semis)

= Non-Japanese producers gain utilization + accelerated qualification pipelines.

Then I mapped that $EMN would be the best Non-Japanese company:

- their PGMEA is specially made for semis.

- get easier requalification by Samsung/SK hynix since they have patents on sustainable PGMEA.

I didn't end up taking a position in the end since I was already fully allocated.

But congrats to anyone who did - I do see $EMN being a longer-term Non-Chinese/Korean beneficiary in the AI/Semis supercycle.

Paradis Labs@ParadisLabs

Potential trade idea: News TLDR: - Strait of Hormuz closed = shortages of naptha (key feedstock used to make semis) - Japanese suppliers (e.g. Shin-Etsu, Fujifilm, Nissan Chemical) rely on Middle East for 40% of its naptha - Has led to Japanese photoresist suppliers (>90% market share) warning Samsung/SK hynix about supply disruptions All of this essentially means: - Japanese photoresist makers face near-term margin compression + volume rationing (negative). - Non-Japanese producers gain utilization, pricing power and accelerated qualification pipelines. What names could actually benefit from this? 1. $DOW - largest global PGME/PGMEA market share (~22%). - full backward integration shields them from Hormuz shock. - TX capacity expansions (debottlenecking) were already online heading into 2026 - gives them spare output just in time for when Japanese lines ration. - CEO said that the war is creating “positive margin inflection” and surging order books. - the risk is kinda obvious? If Hormuz reopens fast, some uplift reverses...but $DOW's cost edge would still remain structural imo. In long-run: $DOW could see multi-yr qualification waves due to CHIPS Act-driven US fab buildout + permanent Japan-risk aversion by Samsung/SK hynix/ $TSM. 2. $EMN - their PGMEA is specially made for semis. - expanded their purification unit in TX in late 2025 - timed perfectly for the shortage. - holds patents on sustainable PGMEA - should ease any requalification by Samsung/SK hynix. - since they're a pure specialty-chemicals player, their output is already qualified / easier to qualify at customers that need Japanese alternatives. - imo, they support a premium valuation as a semiconductor materials pure-play. - $EMN benefit from any capacity-utilization or qualification-win commentary on upcoming earnings calls. In long-run: $EMN have an edge due to specialty focus + recent TX purification investments. Smaller scale allows faster customer-specific tailoring vs. $DOW's volume play. ----- I don't have any room in my portfolio rn for a steady compounder, but I'd probably favour $EMN since they're more pure-play + smaller MC at $8.23B vs. $DOW at $27.82B. And yes, I wouldn't expect any sort of parabolic runs up though. But they could be a nice addition to a portfolio if looking for diversification in the AI supply chain. (I don't advocate for diversification personally, but ofc some ppl are more risk averse than I am). People might say - "why isn't $DD on the list?" - their recent guidance show no semiconductor-materials commentary. Their focus is on water infra, meaning there's no real Hormuz-related tailwinds imo. Also, aware that Chipmakers hold buffer stocks. So fab output isn't collapsing today - but allocation is tightening + prices are already moving (global PGMEA electronic-grade prices up 40-50%). There are more Chinese/Korean companies that could benefit, but many can't/won't trade those markets.

English

@aleabitoreddit Honestly most of your posts are public, being a subscriber doesn’t really make us ahead. Sometimes you post publicly minutes after you post to subscribers. So I see that $1 as a tip rather thant paying a right to know your ideas before the rest

English

I’m convinced that the people who charge $200 or $2000 just to see their stock picks.

Do so just because their ideas aren’t good enough.

Otherwise they would just go long on them with their own capital and retire.

This is why they get mad when they see others sharing better ideas for free.

English

@aleabitoreddit How many of them have not been discovered yet ?

English

SaxoMuse retweetledi

⚠️ L'obligation de déclaration des portefeuilles auto-hébergés ne sera pas mise en oeuvre.

Après plusieurs mois d’échanges, la commission mixte paritaire (dernière étape parlementaire) du projet de loi contre les fraudes fiscales et sociales a supprimé l’article 3 quater. Cet article visait à créer une obligation déclarative annuelle pour les portefeuilles crypto auto-hébergés.

Depuis novembre, l’Adan s’est mobilisée pour porter une position auprès des administrations, des cabinets et des parlementaires : renforcer la lutte contre la fraude, oui ; créer une obligation inopérante et risquée pour les contribuables, non.

Nous remercions les membres de la CMP et les rapporteurs du texte pour leur écoute et leur lucidité, l’ensemble des interlocuteurs institutionnels avec lesquels ce travail a été mené, ainsi que les acteurs du secteur qui ont renforcé la mobilisation.

Français

@PetitRentier Donc faut voir ce que tu peux enlever. Mais aussi voir ce qu’il y a pas et que tu pourrais rajouter

En fait tout dépend de ta stratégie. Mais personnellement je peine à trouver l’idée de ton pf actuel. Tu saurais m’expliquer ? 😃

Français

@PetitRentier Je sais pas. Enlever les redondances. C’est comme si tu faisais des mini ETF par secteur au lieu d’avoir 1 ou 2 entreprises par secteur, tu moyennises ta perf. Ces multiples secteurs sont finalement peu diversifiés et dépendants du même cycle économique et des US. C’est mon avis

Français

Mon portefeuille d’actions - PEA et CTO confondus (~50K€)

🇺🇸 NVIDIA : 4 016 €

🇺🇸 Alphabet : 3 931 €

🇳🇱 Adyen : 3 816 €

🇳🇱 ASML : 3 515 €

🇳🇱 Prosus : 3 218 €

🇺🇸 Amazon : 2 953 €

🇩🇪 Nemetschek : 2 181 €

🇨🇦 Constellation Software : 2 016 €

🇺🇸 Microsoft : 1 985 €

🇺🇸 Mastercard : 1 922 €

🇫🇷 Air Liquide : 1 816 €

🇺🇸 Booking Holdings : 1 790 €

🇺🇸 MSCI : 1 540 €

🇺🇸 Fortinet : 1 509 €

🇧🇷 Nu Holdings : 1 424 €

🇳🇱 Nebius : 1 392 €

🇺🇸 Uber : 1 250 €

🇸🇪 EQT : 1 194 €

🇫🇷 L’Oréal : 1 121 €

🇫🇷 EssilorLuxottica : 1 096 €

🇺🇸 Meta : 1 091 €

🇫🇷 LVMH : 910 €

🇺🇸 Salesforce : 895 €

🇸🇪 Camurus : 870 €

🇩🇰 Novo Nordisk : 823 €

🇫🇷 Equasens : 797 €

🇨🇳 Alibaba : 566 €

🇺🇸 Duolingo : 365 €

🇸🇬 Sea Limited : 343 €

🇺🇸 Netflix : 341 €

Je me rends compte que ce type de présentation permet d’avoir une vue globale et une vraie réflexion sur le nombre de lignes à détenir.

📌 Je précise que :

• 💰 J’ai 3 250 € de cash à investir sur PEA

• 🔒 Je ne peux plus faire de dépôts sur mon PEA Jeune jusqu’à mes 25 ans (seuil de 20k€ atteint)

• 🎯 J’aimerais concentrer le portefeuille en vendant notamment les plus petites lignes

💬 Des avis ? Vous validez l’allocation ? 🤔👀

Română

@elpistollero_ Oui je comprends totalement. C’est un investissement quality

Français

@SaxoDel95616 Il faut en avoir conscience de sont utilité en portefeuille on fera pas x5 en 6 mois c’est pas le but

Français

🔔voici l’écosystème brookfield en image $BN $BIPC

Français

C’est le meilleur moment , c’est la branche la plus récente

Capital déployé (2008 → 2026)

≈ 100 à 120 milliards $ investis cumulés

Dont :

~60–70 milliards $ en acquisitions

~30–40 milliards $ en capex / développement

📊 Rythme

2008–2015 : ~3–5 Md$ / an

2016–2020 : ~5–10 Md$ / an

2021–2026 : ~5–15 Md$ / an (accélération, surtout data & énergie)

Français

@elpistollero_ Le prix est encore bon pour acheter ? J’irai regarder si ca vaut la peine

Français

qui est dans mon cœur de portefeuille pour m’exposer aux infra mondiale, comme je l’explique depuis quelques jours . En bref c’est mon pilier infrastructure pour les décennies à venir

Français

I actually don’t need to get rich quick (I mean, it would be nice).

But instead the first priority is just trying to get less stressed slowly.

Slowing down is the real goal for me personally. Anyone else?!

English

@MRadarCrypto La santé et l’énergie effondrées ? Quand je vois etf energie us ou encore des cours ceux de johnson et johnson ou eli lily je suis pas sur quon puisse dire les secteurs defensifs s’effondrent

Français

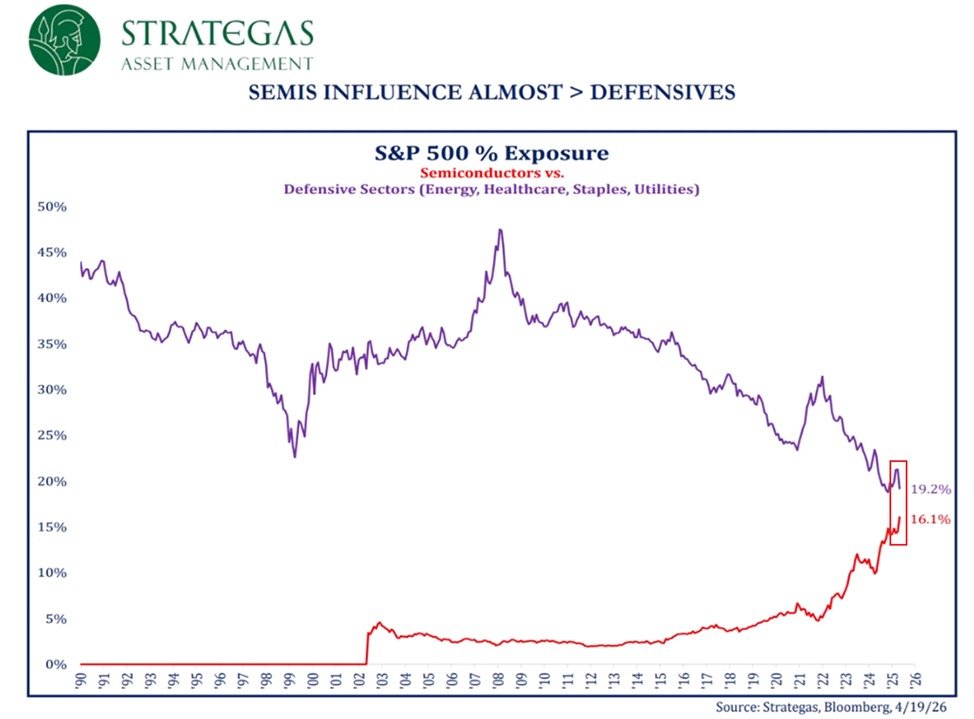

🚨Le S&P 500 n'est plus un indice diversifié. C'est un ETF "Semi-conducteurs" déguisé.

Les puces pèsent désormais 16,1 % de l'indice. C'est 11 points au-dessus du pic de la bulle Internet de 2000.

Pendant ce temps, les secteurs "défensifs" (santé, énergie, conso) pourtant le veritable essieu de l'indice depuis des décennies s'effondrent à leur plus bas historique : 19,2 %. 📉

On a triplé la mise depuis le bear market de 2022. Le marché ne parie plus sur l'économie, il parie sur une seule architecture : l'IA.

Si Nvidia trébuchent, c'est tout le marché qui panique, on l'a déjà vu, et c'est encore plus le cas aujourd'hui à 5260 milliards de valorisation.

Français