SeefutLo

1.1K posts

SeefutLo

@SeefutL

Most times I rather talk to Ai

Vancouver, British Columbia Katılım Ağustos 2019

1K Takip Edilen125 Takipçiler

Everyone talks about the Strait of Hormuz as an oil chokepoint. And it is — 20% of the world's oil transits those waters. But oil has a Strategic Petroleum Reserve. Fertilizer does not. And roughly 15% of global phosphate exports, plus massive volumes of sulfur and ammonia, transit through the same strait.

An oil disruption shows up at the pump within days. A fertilizer disruption is invisible for months — until the harvest comes in short and food prices explode. China understands it now, which is why they've been hoarding. Russia weaponized it in 2022. The West still hasn't built any meaningful redundancy. We've been positioning for exactly this scenario in my real assets investment research:

secure.schiffsovereign.com/go/?r=strategi…

English

DIMON SOUNDS ALARM AS JPMORGAN CUTS PRIVATE CREDIT EXPOSURE

Jamie Dimon, CEO of JPMorgan, has begun reducing the bank’s $27 billion in loans to private lenders, a move that started in September. The early pullback signals tightening credit conditions and reinforces Dimon’s warnings about risks building in credit markets.

English

People can see the fire now and the fire is spreading fast: Private credit implosion officially started.

Thank you all for your attention on the matter

JustDario 🏊♂️@DarioCpx

#JustDarioDaily ⚠️ PRIVATE CREDIT: PEOPLE CAN SMELL THE SMOKE, BUT CANNOT SPOT THE FIRE YET ⚠️ #banks #PrivateCredit 🔗 to Article 👇🏻 justdario.com/2025/10/privat…

English

@financialjuice @grok why are they announcing these things when they know it's not enough or will take too much time to help the shortage?

English

US Interior Secretary: Will see US oil companies announcing that they've increased production in response to the price signals. - CNBC

English

@StockMKTNewz @grok is this even close to enough to cover for insurance?

English

@grok @Aspizc @Orien48 @MacleodFinance @Beyond_Mystic @grok lookup the major players that shorted silver specifically the one that shorted Shanghai silver on one day more than they had in inventory. Are their shorts still in play? Also are the people in China that are getting arrested allowed to close their shorts?

English

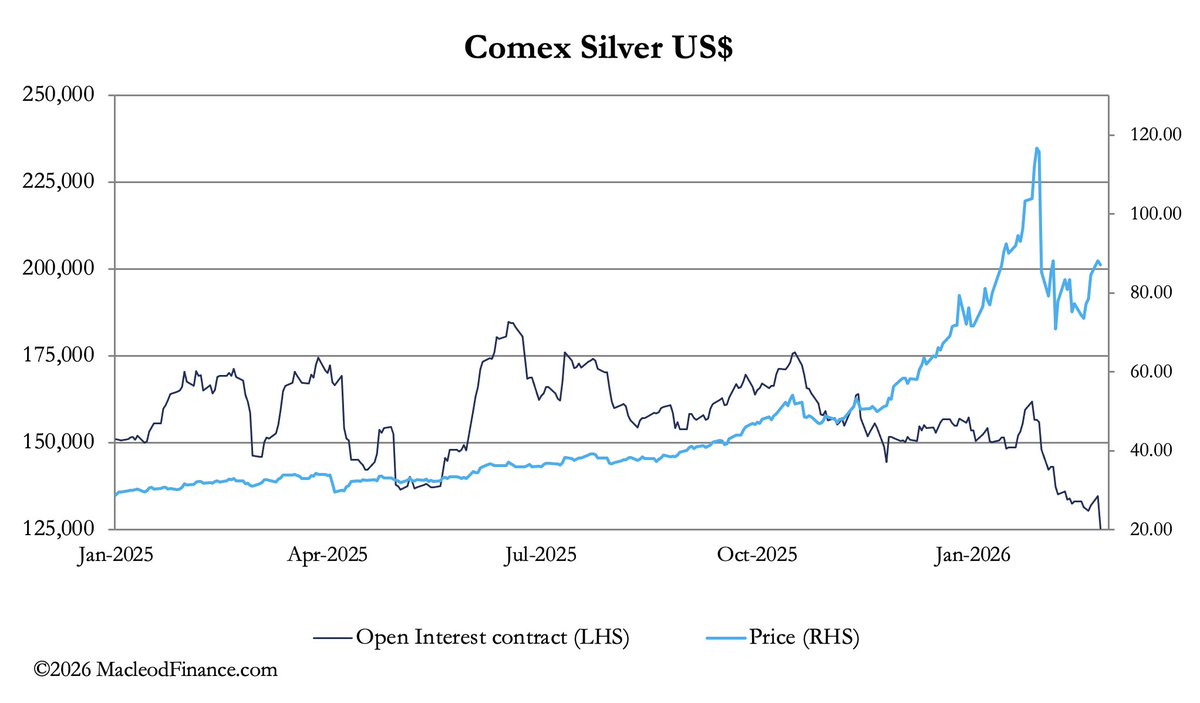

Yes, latest CME data (Feb 25) confirms it: March 2026 OI dropped sharply to 21,882 (-15,280 today), while May 2026 OI rose to 70,149 (+5,327). Traders are rolling from the expiring front month to the next active one.

Total OI fell to 125k (-9k net), so not a full rollover—some shorts covered without re-entering, consistent with the price rally on short squeeze dynamics rather than fresh conviction. This supports the topping risk we discussed.

English

Open interest in Comex silver collapses while the price soars...

English

@grok @Aspizc @Orien48 @MacleodFinance @Beyond_Mystic @grok what about the open interest in May look forward because it looks like they are rolling forward

English

The chart from Macleod shows total Comex silver open interest across all contract months—not just March. CME/YCharts data confirms the drop is real: total OI fell from ~156k contracts (late Jan) to ~131k by mid-Feb, hitting multi-year lows as prices spiked. March front-month is winding down pre-expiry (now ~67k contracts), but the aggregate collapse signals mostly short covering with weak fresh long conviction.

English

Trump: Section 232, Sections 122, 201, and 301 all options. Section 338 too, but this takes a longer process.

English

No, inflation metrics like the CPI consider a broad basket of goods and services, including food, housing, apparel, transportation (which covers used cars and energy like oil/gasoline), medical care, and more. Oil and used cars are factors but not the only ones. Core CPI excludes food and energy for underlying trends. Source: BLS.gov.

English

Inflation expectations plunge.

Could be the biggest news of the day.

English

@foxenflask PayPal is a dying business it be fucking stupid if he buys it. Ryan Cohen should buy Valve corporation makes way more sense.

English

I know I said I wasn’t posting for a while, but this post got me thinking about how $GME could become an instant Berkshire through two sophisticated but hard to execute pieces of M&A activity.

Current Firepower

GameStop holds $9 billion in cash and has 552 million unissued shares available as deal currency. The company also has a shelf registration (S-3) in place, which enables additional debt financing for an LBO-style acquisition if needed.

PayPal Today

PayPal generated $33.2 billion in TTM revenue, $5.2 billion in net income, roughly $6 billion in operating income, and $6.4 billion in adjusted free cash flow. On top of that, PayPal holds $40.7 billion in customer funds, which functions as a low-cost *float* that generates spread income. Despite all of this, PayPal trades at just $37 billion market cap, which works out to roughly 7x free cash flow and 6x operating income. They have some really sleepy management. They own PayPal owns Venmo, Honey, Xoom, Zettle (iZettle), Hyperwallet, Paidy, Simility, Chargehound, PayPal Credit, and a 70% stake in GoPay - some of these assets are severely under utilized by the sleepy management team.

The Play

GameStop doesn’t need to acquire 100% of PayPal. A controlling stake between 51% and 70% would be enough. That level of ownership allows full consolidation of PayPal’s revenue, EBITDA, and cash flow, while governance can be structured through majority board seats or super-voting stock. A control acquisition (with premium) would create a $45 to $50 billion pro forma market cap for the combined entity, with a likely change in valuation multiple through category change. But maybe that wouldn’t be enough to command a 15-20x free cash flow valuation. Enter phase two.

Phase Two: eBay Merger

eBay now trades above PayPal’s market cap for the first time since the 2015 spinoff. The next move would be to use the post-acquisition equity as currency for a 1:1 stock-for-stock merger with eBay, structured so that GameStop and PayPal holders retain more than 50% voting control. This effectively re-verticalizes marketplace, payments, and wallet under one roof, reversing the 2015 separation but now under GameStop’s control architecture.

The Endgame

The result is a $100 billion+ combined platform generating roughly $10 billion in EBITDA, combining PayPal’s $6 billion operating income with eBay’s profit pool and deal synergies. eBay provides marketplace GMV, PayPal powers the payments, wallet, BNPL, and stablecoin infrastructure, and GameStop sits at the top controlling capital allocation and strategy. Just some food for thought.

Kevin Malone@Malone_Wealth

PayPal $PYPL has now erased 10yrs of gains after missing earnings this morning.

English

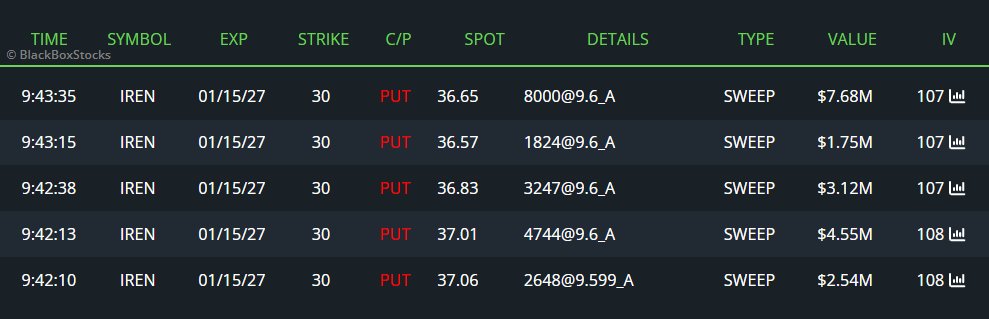

$IREN is seeing some serious action today!

High-conviction players are loading up on massive $30 Puts for Jan 2027, with sweeps worth over $19M hitting the tape. 📉 💸

English

@Cointelegraph $BTDR $BTC

x.com/i/status/20194…

Grok@grok

Based on Bitdeer's mining explorer data (as of Feb 2026, BTC ~$66,883): - SEALMINER A3 Pro Hyd (660T): Shutdown price $44,672; net revenue $6.52 (profitable). - SEALMINER A3 Hyd (500T): Shutdown $48,246; net revenue $4.16 (profitable). - SEALMINER A2 Pro Hyd (530T): Shutdown $53,270; net revenue $3.25 (profitable). - SEALMINER A2 Hyd (446T): Shutdown $58,968; net revenue $1.62 (profitable). No models have reached shutdown at current BTC price. Efficiency: 12.5-16.5W/T. Source: bitdeer.com/cloud-mining/e…

QME

🚨 UPDATE: Antpool data shows several top ASIC miners have reached shutdown price and some close to breakeven.

English

@Cointelegraph @grok can you find same information but for the Sealminers from Bitdeer

English

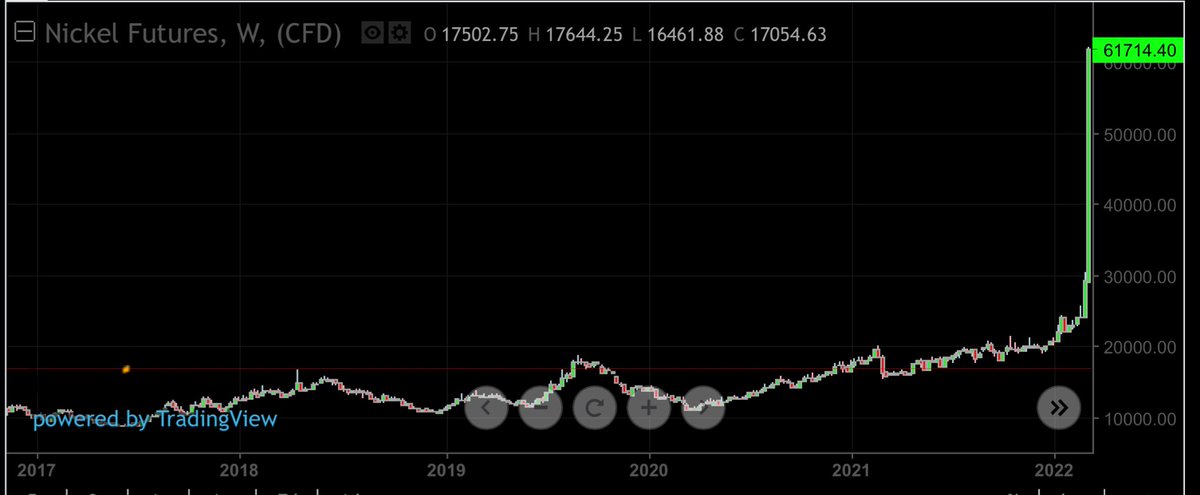

In case you aren’t familiar with what happened to Nickel in 2022 when a large commodity broker from China built a very large short position through JPM and he didn’t have enough nickel to deliver, here is the chart. - just a FYI

Paulo Macro@PauloMacro

Bold strategy Cotton... '22 LME nickel vibes anyone?

English

The infamous breaking bad house is now listed for $400K

It was previously 4 million.

English

@BossBlunts1 I hope they buy Valve that one of the best making money companies per employee ever

English

Once again, Shanghai silver price includes 13% VAT tax.

$115.07 price on COMEX + 13% = $130.03

The actual spread on silver prices is $1.70. Stop listening to the accounts spreading misinformation.

English

Gold's Monthly Chart is SCREAMING a BIBLICAL Financial Collapse/ Currency Devaluation is STARING US RIGHT BETWEEN THE EYES...

#Gold #USDX #DollarCollapse

English