David López Mateos

179 posts

David López Mateos

@SenorScience

Founder and CTO: @ComputeDesk. Exited Pace Revenue to FLYR. Formerly VP of Research at Winton, particle physics researcher at Harvard and CERN

London, England Katılım Temmuz 2018

74 Takip Edilen1.1K Takipçiler

for the sceptics: the dik-dik is a real antelope. about 30cm tall. we didn’t make it up.

English

David López Mateos retweetledi

me: i made a list of names we should probably block

ceo: read them out

me: judicious-booby, moist-mongoose, tiny-dik-dik

ceo: keep them all

Compute Desk@ComputeDesk

Today we're launching gpuspec.io. Buying or selling GPU capacity means describing the same cluster over and over: model, count, region, fabric, term, price. It's slow to write, easy to garble, and impossible to track once it's been forwarded a few times.

English

We launched a tool for writing down and sharing what's in a cluster. Sounds simple, and it is, but you can't price or trade capacity until everyone describes it the same way. Bigger stuff on top of it shortly. Have fun with it!

Compute Desk@ComputeDesk

Today we're launching gpuspec.io. Buying or selling GPU capacity means describing the same cluster over and over: model, count, region, fabric, term, price. It's slow to write, easy to garble, and impossible to track once it's been forwarded a few times.

English

Takes seconds to make one, try it out.

gpuspec.io/humble-pogona

English

Today we're launching gpuspec.io.

Buying or selling GPU capacity means describing the same cluster over and over: model, count, region, fabric, term, price. It's slow to write, easy to garble, and impossible to track once it's been forwarded a few times.

English

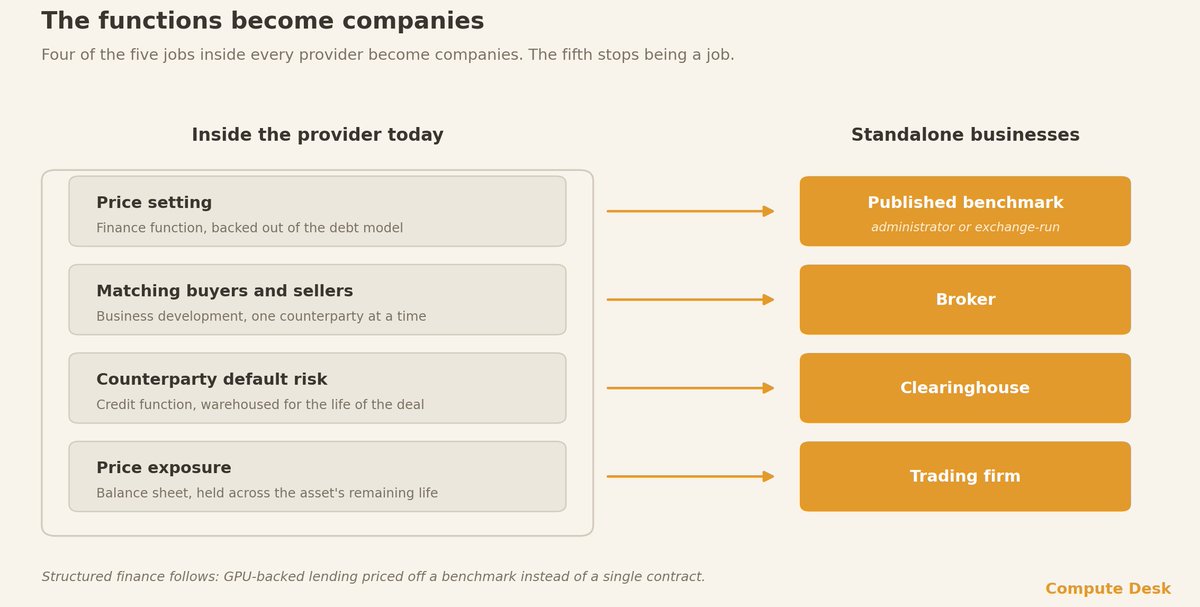

Every neocloud today is its own broker, its own insurer, its own clearinghouse.

Not by strategy, by default: it sets its own price, eats counterparty risk, and holds price exposure for the life of the asset, because the financial layer that takes those jobs off its books is only now being built.

When it arrives, those jobs become companies.

computedesk.substack.com/p/financial-ma…

English

Fair, and both our indices, Hopper and Blackwell, are moving up. The difference is pace: Blackwell is climbing faster. This is coming primarily from H100 stabilizing while higher memory chips like H200 keep climbing up. HBM is the scarce piece, and it's the part showing up in the rents.

English

GPU rental rates are up 5-10% so far in July (led by the newer gens).

English

So excited for this announcement. Long time in the making, but so much more still left to unveil…

Compute Desk@ComputeDesk

Today we announce Compute Connect with our partners @Architect_Fi, and built on our Compute Clear infrastructure. Compute Connect is an Exchange-for-Physical market. Neoclouds, AI companies, enterprises exposed to compute procurement and pricing risk will have a bridge between the physically-settled compute deals they are familiar with, and the cash-settled derivatives market familiar to financial institutions. We will announce launch partners soon, and invite neoclouds, compute brokers, market-makers and traders to inquire at info [at] compute-index [dot] com.

English

This is the missing piece sitting at the intersection of Compute and Finance. So proud to be partnering with @BrettHarrison to make this a reality.

Brett Harrison@BrettHarrison

Announcing ComputeConnect, the financial industry’s first exchange-for-physical (EFP) network for compute, coming soon from Architect and @ComputeDesk. ComputeConnect links US exchange-traded compute futures to compute capacity delivery. Exchange-listed cash-settled compute futures are entering US markets to correct course on the current AI economy, reorienting debt to long-term growth: • Creating price discovery and transparency independent of any single capacity provider. • Establishing a forward curve for measuring deprecation and forecasting supply and demand. • Providing financial hedges for compute consumers and producers. • Enabling hedge funds, ETF companies, and traders to gain long and short financial exposure to compute. US cash-settled compute futures lack a physical delivery mechanism, and ComputeConnect fills this gap. Existing physically settled futures such as energy and agriculturals require their clearing house (DCO) to set a uniform standard for the grade and delivery method for the underlying commodity. Compute, by contrast, is highly fragmented, heterogeneous, and rapidly evolving, making it infeasible for any single DCO to define and enforce comparable standards. ComputeConnect establishes a network of compute capacity providers and links the network with Architect’s US futures products using exchange-for-physicals (EFPs), OTC contracts in which futures positions are exchanged for the assets the futures track. EFPs allow counterparties to negotiate the grade, timing, location, and other characteristics of the commodity along with a basis tied to the futures settlement price. ComputeConnect will • Build a network of capacity providers and capacity marketplaces. • Establish an open protocol for members of the network to receive delivery requests and advertise available GPUs. • Publish standard basis tables for different SKUs, memory configurations, and locations for GPUs. • Book the futures legs of the transactions to Architect’s DCM, the American Innovation Exchange. • Facilitate and guarantee delivery of capacity using Compute Desk’s ComputeClear platform. The advancement of US AI is constrained at every link in the supply chain: materials, power, chips, capital… The American Innovation Exchange, ComputeConnect, and our industry partners aim to secure compute’s dominance as an American asset class.

English

Two providers sell the same bare-metal GPU contract at the same rate.

One owns the substation, the building, and the chips. The other resells capacity it rents from someone else.

Same product page. Very different balance sheets.

Why "neocloud" is a hyperscaler-era word: open.substack.com/pub/computedes…

English

@BrettHarrison is doing a great service to the compute industry. Proper risk allocation is necessary to reduce systemic risk in this build-out, and the pieces he's putting out are critical for the necessary adoption.

Brett Harrison@BrettHarrison

Compute options will be as transformative to the US AI industry as compute futures. Sellers and buyers of compute won't only use options for insurance, they'll write options and get paid. Covered calls and cash-secured puts: Compute sellers: covered calls Compute sellers such as neoclouds are long inventory: racks of accelerators that will be rented out over the coming years. Against the capacity they already own, they can write covered calls on GPU-hour prices above today's market and collect the premium as income. If prices stay flat or drift lower, they keep the premium as yield on top of their rental revenue. If prices rise above the strike price at expiration, they rent out capacity at the strike price while still keeping the premium. The upside beyond the strike is capped, but in return the seller converts a portion of future GPU price volatility into present cash. At each expiry, the seller can keep writing calls against inventory, harvesting premium from a depreciating asset. Compute buyers: cash-secured puts Compute buyers such as frontier model companies and AI labs are short inventory, looking to acquire rental time on GPUs. Buying futures locks in their effective price, and buying calls insures against rising prices. But there's another important derivatives trading strategy for compute buyers: writing cash-secured puts. If there's a price below the prevailing GPU rental rate that a buyer would be happy to pay, they can sell a put at that strike and immediately collect the premium as income. If prices rise, they keep the premium when the put expires out of the money. If prices fall to the strike or below, they effectively buy compute at the lower price, partially subsidized by the premium they collected. Both strategies, executed with discipline and proper risk management, generate income while the worst-case exercise scenarios align with the natural hedge. In summary: • Futures: lock in the forward price of compute. • Buying options: insure against adverse moves in GPU prices. • Selling covered calls or cash-secured puts: generate income where exercise aligns with the natural hedging outcome. These strategies are hallmarks of mature US derivative markets facilitated by CFTC oversight. The American Innovation Exchange and our industry partners are ready to support compute as a US-developed asset class from the beginning.

English

The basis-risk objection is a stall. It tells everyone who can't move this risk today to wait for a perfect instrument that's never coming. But 0.7 correlation already halves your variance, and a hedge doesn't need to do more than that. You don't wait for perfect, you hedge when it kills enough risk to be worth the cost. Compute buyers have nothing right now, so the real bar is "better than nothing," and this clears it easily.

Brett Harrison@BrettHarrison

US Compute Futures As Hedges Compute futures face the argument that if a future doesn’t track the exact costs hedgers incur, it will carry too much basis risk to form a viable market. This fundamentally misrepresents how hedges actually function in many major US markets. A hedge does not need to be perfect in order to be useful, let alone transformative, to its underlying commodity market. To be viable as a multi-billion dollar market, a hedging instrument needs to remove enough risk at scale to be worth its initial cost. If the correlation between a hedging instrument and the portfolio is ρ and the optimal hedge ratio is used, the fraction of variance eliminated by the hedge is ρ². A correlation of only 0.7 cuts variance in half. Cross-hedges built on loose relationships predominate in the real US economy. Airlines hedge jet fuel with crude. Bond desks hedge rate risk in credit with treasuries. Long-short equity portfolios hedge market beta with S&P 500 futures. At my former firms Jane Street and Citadel Securities, every trading desk was required to hedge portfolio factors with related instruments intraday and overnight to isolate alpha. Commodity markets are typically heterogeneous. Compute is not a unique underlying in this respect. An “H100 hour” could represent many different goods: SXM or PCIe, spot or reserved, hyperscaler or neocloud, US or Asia. Weigh this “problem” against the “solution” that compute buyers and sellers have today: nothing. Asset-backed loans on GPUs carry 40-50% haircuts because lenders can’t transfer the associated risks. The institutions financing the >$1T datacenter-linked debt sector regularly transact in other heterogeneous commodity markets. The success of US compute futures/options markets primarily depends on CFTC-regulated exchanges’ agility and competency at collaborating with index providers native to chip configurations, neocloud procurement, and timeseries interpolation on a continuous basis. Designing a futures contract that minimizes basis risk and maximizes liquidity formation is an antecedent requirement. Fulfilling the US government mandate to “accelerate the maturation of a healthy financial market for compute” is the main goal.

English

Funny detail in here: the oldest chip, the one with the biggest install base, had the biggest rental jump this year. So much for old silicon being the depreciating trade. People miss it because there's no public price for any of this, rental or resale. You only catch it by tracking where it actually clears. Daily.

Compute Desk@ComputeDesk

Daily GPU compute rates live from @Architect_Fi, ahead of imminent Compute Futures on AI Exchange. Tickers powered by @ComputeDesk. Reach out for hypergranular intraday feeds.

English

Worth 99 seconds of anyone's time. Compute futures stopped being a thought experiment and turned into a live product faster than almost anyone expected. Good to see it explained plainly.

Jacob Robinson@JacobRobinsonJD

Compute futures are the most novel product I've heard of in the past month. What is a "compute future"? @BrettHarrison explains exactly how it works in 99 seconds (he and his team at @Architect_Fi pioneered them).

English

Resale and yield run on different clocks. Resale tracks the secondary market for the chip. Yield tracks the rental market for the hour it produces, and that one is climbing on scarcity: spot discounts on H100 have been narrowing as providers reprice reclaim risk. A chip can be worth less while the compute it produces rents for more. There's a trade in the gap between the two.

English

GPU depreciation is about resale value, GPU yield is a different story. H100 rental prices are up 19% in 90 days and H200 up 17%. Older silicon may fetch less on the secondary market over time, but the compute the chips produce is renting for more. Not the same trade.

English

Edge inference is here. The market for it isn't.

Comcast, Charter, Akamai, Cloudflare, Nscale: real GPUs in real metro DCs. But the pricing layer to clear them doesn't exist.

What programmatic ads solved, edge compute hasn't:

computedesk.substack.com/p/edge-inferen…

English

The demand side is not the question: it is there. Whether these take off comes down to the settlement index: does it track the price an operator actually pays. Too broad and the hedge carries basis risk against an average nobody touches. Too narrow and it is too thin to settle. The index is the hard part, and it is the part we just built.

English

I’d like to see a prediction market on how much volume compute futures will have at the end of next year. This is one of the most interesting sub-stories to me right now. And I’ve heard compelling arguments in both directions on whether they’ll take off or not.

English

David López Mateos retweetledi

"The suitability of the Hedge depends on the index."

@Architect_Fi compute futures powered by @ComputeDesk indexes.

Brett Harrison@BrettHarrison

The typical neocloud operator we speak to says some version of: “I’ve sold out 12 months of capacity on my H200 cluster, but I don’t know what compute prices will be in months 13-24.” Futures solve this, but the suitability of the hedge depends on the index. More below ↓

English

The months 13-24 line is exactly the gap. Why the index decides suitability: too broad and the hedge carries basis risk against an average the operator never touches, too narrow and it is too thin to settle against. Capturing private cloud clears without losing the specific cluster is the whole problem. That index is the part we built.

English

The typical neocloud operator we speak to says some version of: “I’ve sold out 12 months of capacity on my H200 cluster, but I don’t know what compute prices will be in months 13-24.” Futures solve this, but the suitability of the hedge depends on the index. More below ↓

Architect@Architect_Fi

Compute futures indexes need to be broad enough to capture private cloud transactions but narrow enough to minimize basis risk for datacenter hedging. Architect’s Nvidia H100, H200, B200, and B300 futures will offer the best of both worlds on the American Innovation Exchange.

English

A month ago I wrote that two layers were missing under the procurement paradigm: a way to hedge forward compute price without buying more capacity, and a benchmark worth settling it against. Today the first one ships. Architect is listing H100 through B300 futures, settled to our index. The contract was the easy part. The index is the work: broad enough to catch where compute actually clears in private deals, narrow enough that the hedge tracks your cluster and not a market average. Now there is a price to trade around.

Architect@Architect_Fi

Compute futures indexes need to be broad enough to capture private cloud transactions but narrow enough to minimize basis risk for datacenter hedging. Architect’s Nvidia H100, H200, B200, and B300 futures will offer the best of both worlds on the American Innovation Exchange.

English