@miclyn411359 Its just not as simple as we all think. All lawsuits need to be done with. Powell needs to be gone. Its gotta be done right.

English

Serge Motrin

58 posts

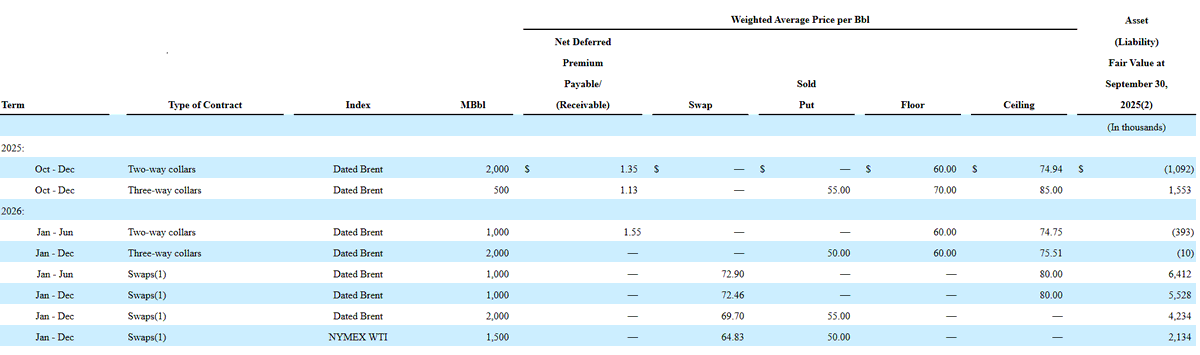

Kosmos Energy - $KOS (monthly) One of my favourites oil/gas play Let's check potential share valuation at $150 oil (not taking into account their gas revenue) Shares Outstanding: 481 M Current Market Cap: 481 M × $2.90 ≈ $1.39 B Net Debt: ~$3 B EV ≈ $4.39 B $150 oil Production: 65k boe/day (~2.37 M boe/year) Revenue = 2.37 M boe × $150 ≈ $355.5 M Costs: $25/boe → $59 M/year EBITDA ≈ $296.5 M I'm gonna use the same implied EV/EBITDA multiple from current market pricing: - Current EBITDA at $100 oil (no gas) ≈ $178 M - Current EV ≈ $4.39 B Implied current EV/EBITDA multiple ≈ 4.39 B / 178 M ≈ 24.6× (this reflects market optimism) At $150 oil → EBITDA ≈ $296.5 M EV = 296.5 × 24.6 ≈ $7.29 B Equity = EV – Net Debt ≈ $7.29 B – $3 B ≈ $4.29 B 💡$4.29 B ÷ 481 M shares ≈ $8.92/share