Sabitlenmiş Tweet

PTA

477 posts

PTA

@Serta_Capital

Professional Investor (Private Credit) | OG SpaceMob | $ASTS enthusiast | Sharing DD on launches, partnerships & risks | NFA

Chicago, IL Katılım Ocak 2014

443 Takip Edilen383 Takipçiler

@elonmusk The nearest star is light years away, what are you talking about.

English

It’s a start. Vastly more will be needed to extend consciousness to the stars.

The Rabbit Hole@TheRabbitHole

SpaceX has launched more then every other company combined

English

Chinese or not, doesn't matter. But I can clearly tell you let your stock control you which should be the other way around!

Dr. Sp🅰️ceman@drunkonrumraisn

@Money_or_Life_X Terrible take but no surprise it's Chinese.

English

@Kaynouky Yes, if they got stuck in the SECO 1 orbit they are toast, but we don't know that; second upper stage burn may have happened partially and boosted them up, or may not have happened at all. Need to wait for data.

English

Best estimate for the SECO-1 orbit given the slow observed decrease in altitude in the webcast is somewhere in the range of 164 x 380 km to 116 x 420km, depending on flight path angle at cutoff which was somewhere in the 0 to -1 degree range.

Still waiting for SECO-2 data.

English

English

I’m down hundred of thousands over the past 2 days… management, please throw me a bone.

@AbelAvellan

@scottwisniews

@AST_SpaceMobile

$ASTS

English

@commonsenseplay seems like AI firms mostly do that in house (for example, forward deployed engineer at PLTR)

English

AI NEEDS MANAGEMENT CONSULTANTS AFTER ALL

I hope you listened - huge opportunity for swing trades in Consulting giants to spread artificial intelligence through the business world.

- Accenture $ACN: down nearly 50% from 2025 high

- Booz Allen Hamilton $BAH: down 55% from 2024 high

- FTI Consulting $FCN: down 20% from 2024 high

- Gartner $IT: down 30%

- Capgemini $CAP.PA: down 40% from ATH

Common Sense Investor (CSI)@commonsenseplay

IS CONSULTING A DEAD-END INVESTMENT? I don’t think so. The market is pricing it like it is. From their all-time highs, major public consulting firms have been heavily repriced on AI fears: Accenture $ACN: down nearly -50% from 2025 high Booz Allen Hamilton $BAH: down 55% from 2024 high FTI Consulting $FCN: down 20% from 2024 high Gartner $IT: down 30% Capgemini $CAP.PA: down 40% from ATH The narrative: AI replaces consultants. I think that’s massively overblown.What the market is missing: 1) AI ≠ infinite acceleration The “just add more compute” story is starting to show limits - cost, diminishing returns, and real-world friction. AI will keep improving, but not in a straight line the market is pricing. 2) Consultants are the ones who monetize AI These firms aren’t getting disrupted - they’re positioned to win through: - Leaner teams means expanding margins. Selling AI strategy, integration, and deployment Helping enterprises actually implement “agentic” systems - Everyone wants AI. Almost no one knows how to deploy it at scale. 3) Enterprise transformation takes YEARS - Most large organizations are running on decades-old infrastructure (even mainframe architectures are still widely in use) - AI adoption means:ripping out legacy systems integrating across fragmented stacks navigating compliance and risk That’s not a product - that’s a multi-year consulting engagement. The reality: - Consulting isn’t dying, it’s becoming more critical! - AI increases complexity, not simplicity. And complexity drives demand for advisory. I’ve started buying Accenture and am watching the others closely. If sentiment shifts, a 50–70% rebound in high-quality names like ACN over the next 12–18 months is very realistic. This looks like a classic overreaction and there is money to be made!

English

@CatSE___ApeX___ why is this related to asts? is it possible this is for starlink?

English

$ASTS

Grain Management wants to use 800 MHz for satellite D2D fierce-network.com/wireless/grain…

The B🅰️reskin Bear@Dmaj7add6overC7

$ASTS The Grain management 800 MHz of T-Mobile spectrum situation continues. When paired with the FCC ITU filing on behalf of AST for T-mobile frequencies, and other recent filings, it seems increasingly plausible T-Mobile is positioning to join w/ AST. x.com/CatSE___ApeX__…

English

@Euunul @BaldingsWorld lol your industries are decimated because of chinese dumping

English

Well, if Europe would apply the same standard we would have to declare war on USA. Cyber security? US is using tech platforms to spy on and influence the European population. Economic? US has been sabotaging the European economy for years if not decades (GFC for example, tariffs, hostile takeover of Alstom, Nord Stream etc). Neither China nor Iran threatened to invade us, USA did.

English

I hate to hit on this but Europe and the US do not come close to agreeing on security at a big picture level or on the details and you cannot have a security alliance lacking even some agreement on what constitutes security. Let me give you an example.

1. The US assumes a much larger definition of security. Cyber. Economic. China. Iran. On and on. Europe utilizes a very narrow definition of security: has a sovereign state physically attacked an EU/NATO member state? If the answer is no, then it does not apply to me and we are not interested. At the most fundamental level, Europe and the United States do not agree on the concept of security.

2. Europe and the United States do not agree on how or when to act. Take Iran as a simple example. Arguably the reason the Trump administration acted was to prevent Iran from reaching a point where the US would be unable to prevent Iran fro obtaining nuclear weapons. Europe does not believe in acting until they have been physically attacked. Two different approaches to security.

3. Europe and the United States treat proximity very different. Europe is only interested in direct physical proximity threats (i.e. Russia). The United States sees threats globally.

4. The United States has for decades, though pushed farther under Trump, expected allies to engage in burden sharing. Europe due in no small part to sections 1-3 treats security and protecting burden sharing as one way to defend Europe.

There is no reason to get angry but the idea that a security alliance can exist when partners in alliance do not share the most basic shared definitions make continuing an alliance difficult at best.

English

If you've had your eyes on any items from the $ASTS merch store, everything in the store is 30% off today fyi.

ast-spacemobile.myspreadshop.com

Maybe they are trying to clear out inventory for new designs (new launch patches, etc...)?

English

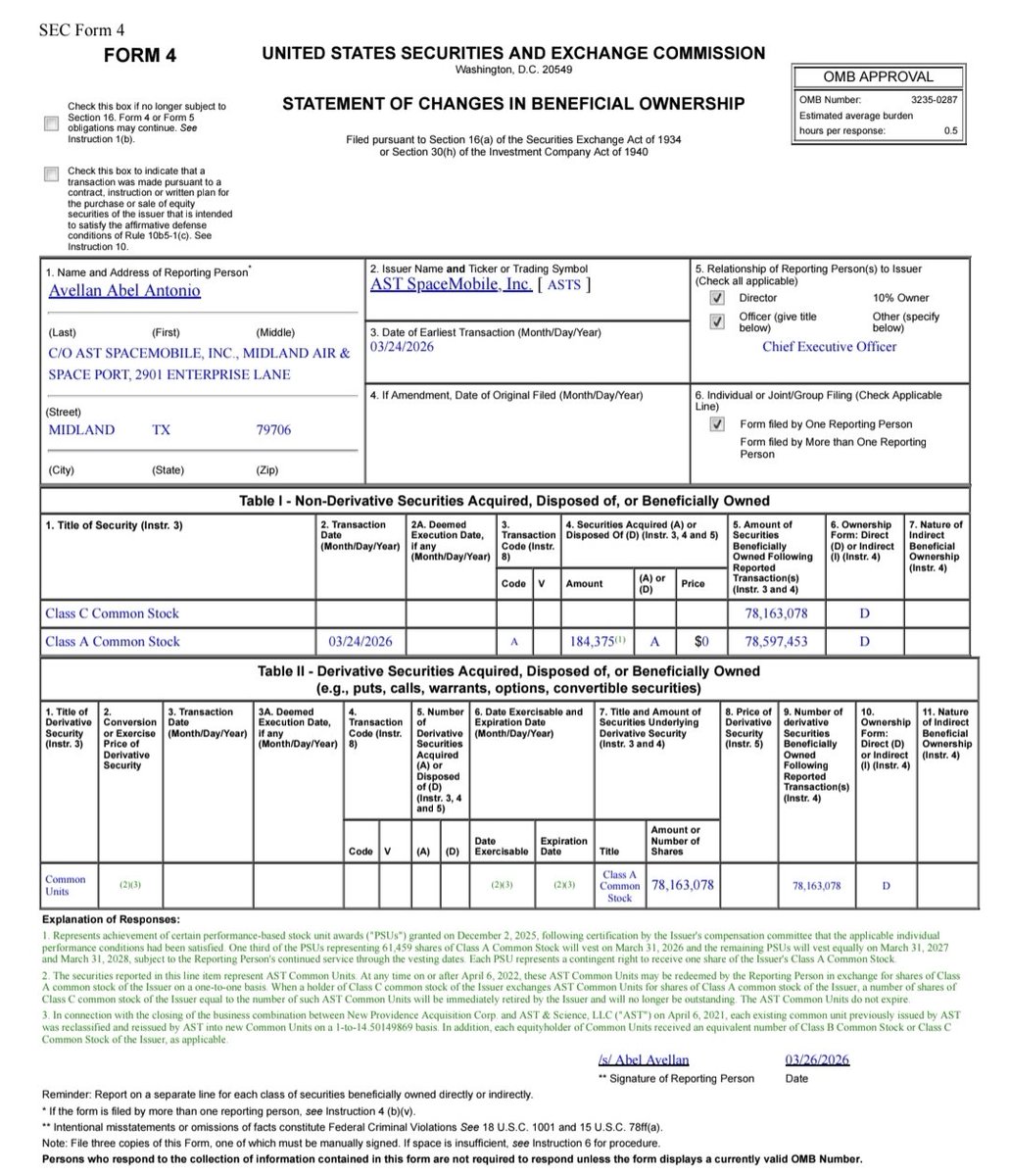

ABEL AVELLAN RECEIVES 184,375 SHARE AWARD

The shares relate to meeting performance achievements that have been deemed to have been met.

The last time this happened we got news in the next couple of weeks so hopefully this means a big milestone has been achieved!

$ASTS

English

$ASTS AST SPACEMOBILE REFINES BLUEBIRD: EXECUTION STORY, NOT THEORY

The latest conference update on @AST_SpaceMobile is not introducing a new vision. It is tightening the execution path. The market is starting to transition from “is this possible?” to “how fast can this scale?”

1) BLUEBIRD IS MOVING FROM PROTOTYPE TO PRODUCTION

The company used the Satellite Conference to refine how its BlueBird constellation rolls out, reinforcing that this is now a deployment story, not an R&D experiment. The emphasis is on cadence, coverage, and scaling capacity across markets.

Important because the technical risk phase has largely been addressed with successful deployments like BlueBird 6, which already demonstrated the core architecture at full scale.

2) DIRECT-TO-DEVICE IS BEING POSITIONED AS GLOBAL INFRASTRUCTURE

This is no longer being framed as a niche connectivity solution. The messaging is clearly shifting toward global broadband infrastructure delivered directly to standard smartphones.

That implies:

•No hardware dependency at the user level

•Immediate TAM via existing mobile subscribers

•Integration through MNO partnerships rather than retail customer acquisition

This is structurally different from traditional satellite models and explains why valuation debates are intensifying.

3) THE REAL STORY IS CAPACITY AND COVERAGE DENSITY

Refining the BlueBird rollout is effectively about one thing: how quickly AST can achieve continuous, not intermittent, service.

Investors should focus on:

•Satellite production rate

•Launch cadence

•Regional coverage stacking

•Throughput per satellite

Because once continuous coverage is achieved in major markets, the revenue model transitions from speculative to recurring at scale.

4) VALUATION DEBATE IS SHIFTING FROM “IF” TO “WHEN”

The article highlights ongoing valuation debate, but the underlying shift is clear. The question is no longer whether direct-to-device broadband works. It is how large the revenue base becomes once deployed globally.

This is where traditional satellite comps break down:

•This is not a capacity-constrained niche network

•This is a shared infrastructure layer across billions of devices

That creates a fundamentally different ceiling.

CONCLUSION

This update is incremental on the surface but significant in implication. AST SpaceMobile is tightening execution, aligning rollout expectations, and signaling that the bottleneck is now deployment speed, not technology.

The market is still treating this as a speculative space story. The company is increasingly presenting it as terrestrial telecom infrastructure delivered from orbit.

That disconnect is where the opportunity sits.

finance.yahoo.com/markets/stocks…

English

Blue Origin’s launch support vessels left Port Canaveral this afternoon - likely practice for the upcoming AST Bluebird 7 launch! Tug Harvey Stone led the parade with Jacklyn (LPV-1) in tow. Daughter Craft joined for a bit with her new boarding access equipment. Off Patrick now.

English

Can someone explain how this remotely justifies $RKLB’s price?

Space Investor@SpaceInvestor_D

$RKLB Revenue per year (consensus): 2021: $59M 2022: $207M 2023: $248M 2024: $434M 2025: $599M 2026 (p): $876M 2027 (p): $1.21B 2028 (p): $1.57B 2029 (p): $1.91B

English

@tottaway22 Unlikely. Artemis operates on fixed NASA timelines while New Glenn's schedule keeps slipping. Pick one mission or risk missing both.

English

Will the timing work that people attending the Blue Origin New Glenn 3 Launch for $ASTS BlueBird 7 will also get to watch Artemis on 3/6?

Please. Would be great timing!

English

@RatboyMilnor @navymig @SydSteyerhart japan will carry it’s weight. europe and canada are just deadweight 🤷🏻♂️

English

@navymig @SydSteyerhart Europe & Canada have been allies with the US for a much longer time and that relationship has been smashed to bits in about 3 months time by the orange clown, so I don’t see why you think Japan-US relations are bulletproof

English

The right-wing in Japan has a large enough supermajority that they can amend the Constitution that was forced on them at gunpoint by American liberals in 1945.

For the first time in nearly a century, the Soul of the Japan can be reclaimed.

由仁アリン Arin Yuni@Arin_Yumi

BREAKING NEWS: THE LDP HAS SECURED A SUPERMAJORITY OF 310 SEATS

English

@LostFundamental Why would you use satellite operators comp when this is a high growth high margin business? This is like using OEM comps to value Tesla.

English

This is in-line with where mature satellite operators trade and not at their randomly assumed 18.5x EV/EBITDA for $ASTS. 5/N

English

$ASTS AST Space Mobile – why this is likely a $20 stock longer term. Just a point view, not financial advice, please keep it civil the thread is just meant to present an alternative view. We will see who is right soon enough! BTW, anybody remembers CSR (more later). 1/N

English

@steve2bacon So much cope in chat lol. Poverty is limiting their imaginations.

English

Jesus, I see what you’ve done for ASTS investors, and I want that for me 🙏😔

English

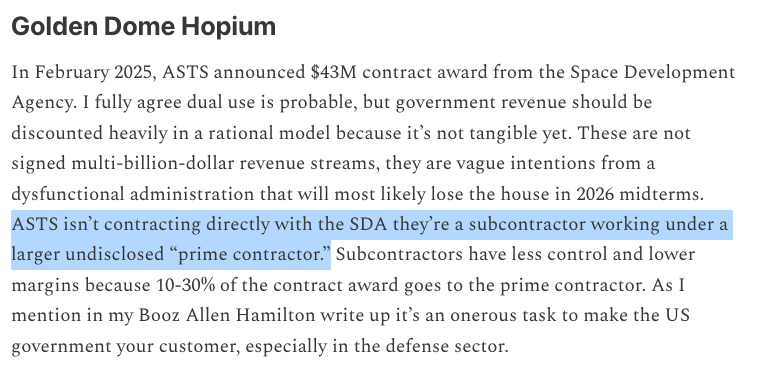

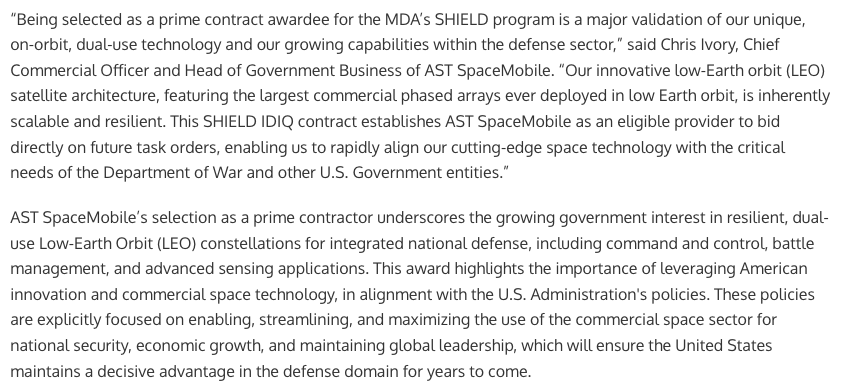

Mr. Valuations on Jan 9: $ASTS isn't contracting directly with the SDA they're a subcontractor. Subcontractors have less control and lower margins. Golden Dome is hopium.

*One week later*

“Being selected as a prime contract awardee for the MDA’s SHIELD program (part of the broader Golden Dome strategy) is a major validation of our unique, on-orbit, dual-use technology and our growing capabilities within the defense sector.”

English

@peterlindmark Thank fucking god it didn't happen for ASTS lol. One of my fears and I get diversifying launch partners are good but SpaceX definitely gets you the peace of mind.

English

PSLV-C62 / EOS-N1 Mission | Lost control over its orientation during 3rd stage action.

English